In the world of personal finance, your credit score is often treated like a secret “grade” that determines your worthiness for a home, a car, or a loan. Because it’s so important, it’s also surrounded by myths and old wives’ tales that can actually end up hurting your financial progress.

At LendingMoney.ca, our goal is Credit Rehabilitation. We want to pull back the curtain on how credit really works so you can stop worrying and start building. Here are seven of the most common credit score myths debunked.

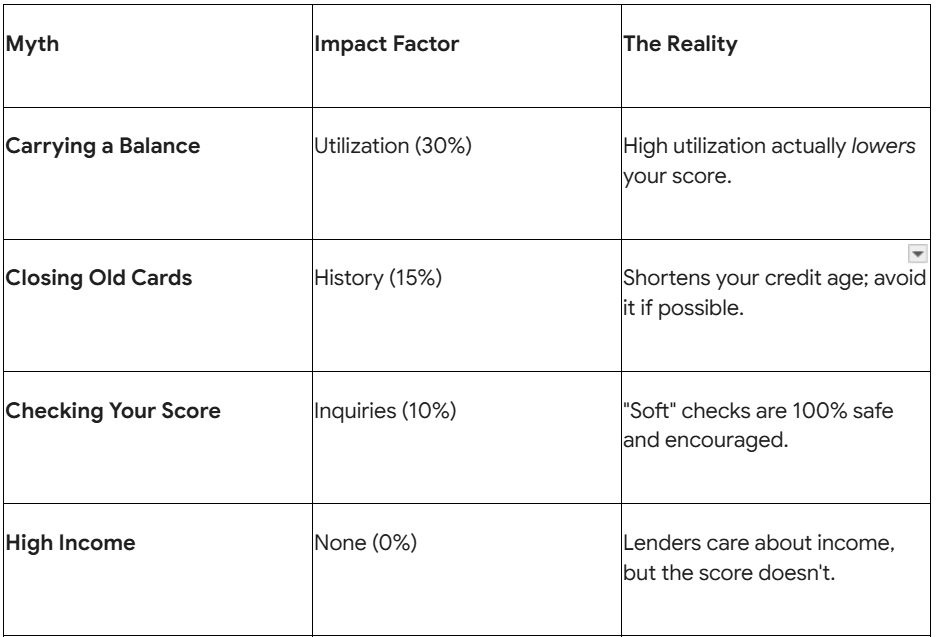

Myth #1: Checking my own credit score will lower it.

The Fact: Checking your own credit score is considered a Soft Inquiry (or a soft hit), and it has zero impact on your score.

In fact, we encourage you to check it regularly! Monitoring your score through services like Equifax, TransUnion, or third-party apps helps you spot errors or signs of identity theft early. The only checks that lower your score are “Hard Inquiries,” which happen when a lender pulls your report to approve you for a new credit card or loan.

Myth #2: Carrying a balance on my credit card helps my score.

The Fact: This is one of the most expensive myths out there. You do not need to pay interest to have a good credit score.

Lenders want to see that you use your credit and pay it off. Carrying a balance month-to-month doesn’t help your score; it just costs you money in high interest. The best strategy for your score is to pay your balance in full every month. This keeps your Credit Utilization Ratio low, which accounts for about 30% of your total score.

Myth #3: If I have a high income, I’ll have a high credit score.

The Fact: Your salary is not part of your credit score calculation.

You could earn $200,000 a year and have a poor credit score if you miss payments or max out your cards. Conversely, someone with a modest income can have a perfect 850 score by managing their debts responsibly. While your income is very important to lenders when they calculate your “Debt-to-Income” ratio for a mortgage, it doesn’t move the needle on your three-digit credit score.

Myth #4: I should close old credit cards I don’t use anymore.

The Fact: Closing an old account can actually lower your score.

There are two reasons for this:

- Length of History: 15% of your score is based on the age of your accounts. Closing your oldest card makes your credit history look shorter (and “younger”) than it actually is.

- Available Credit: Closing a card reduces your total available credit limit. If you have a balance on other cards, your utilization percentage will suddenly spike, which looks risky to lenders.

Myth #5: Paying off a debt removes it from my credit report.

The Fact: Negative information (like a late payment or a collection) usually stays on your report for 6 to 7 years.

Paying off a collection account is great – it changes the status to “Paid,” which looks much better to a human lender – but it doesn’t make the history of that collection disappear instantly. The key to “Credit Rehabilitation” is to start making on-time payments now so that the positive recent history outweighs the old mistakes.

Myth #6: Debit cards help build my credit score.

The Fact: Using a debit card has no impact on your credit.

When you use a debit card, you are spending your own money from a chequing account. Credit scores only track how you manage borrowed money. If you are trying to build credit from scratch or rebuild after a tough period, you need a “tradeline” like a secured credit card or a small installment loan that reports to the bureaus.

Myth #7: A divorce automatically separates our credit scores.

The Fact: Credit scores are always individual, but joint accounts stay joint until they are closed.

A divorce decree might say your ex-spouse is responsible for the joint car loan, but the bank doesn’t care. If your name is still on that loan and your ex-spouse misses a payment, your credit score will take the hit. When separating finances, it is crucial to pay off, close, or refinance joint accounts into single names.

Why Understanding the Truth Matters

At LendingMoney.ca, we see these myths every day. Clients often wait to apply for help because they are afraid of a “hit” to their score, not realizing that the high-interest debt they are carrying is doing far more damage every single month.

Our Credit Rehabilitation approach is about more than just money – it’s about education. When you understand the rules of the game, you can win.

Ready to stop guessing and start growing? [Apply with Ease] and let our Financial Heroes help you build a plan based on facts, not myths.

Read Blog – The Truth Behind the Curtain: Myths vs. Realities of Private Lending