When the CRA freezes your account, they aren’t just taking the money you have; they are capturing every dollar that enters that account-including your upcoming salary, GST rebates, and even child benefit payments. Here is what you need to do in the next 24 hours.

1. Don’t Panic, But Don’t Wait

A bank freeze doesn’t “go away” on its own. Your bank is legally obligated to comply with the CRA’s order. They cannot help you, and they cannot “give you a little bit back” for groceries.

- The Action: Call the CRA Collections Officer assigned to your file immediately. You can find the general collections line at 1-888-863-8657.

- The Goal: You need to find out the Total Amount Subject to the Requirement to Pay. Often, the CRA freezes more than you actually owe just to ensure they capture the full balance plus interest.

2. The Hero Pivot: Open a New Account (Carefully)

While your current account is frozen, you still need to live.

- The Move: Open a new bank account at a different financial institution-one where you have no existing debt or credit cards.

- Why this works: It takes the CRA time to “find” new accounts. Redirect your payroll or direct deposits to this new account immediately. This is not “hiding” money (which we don’t recommend), but it is ensuring you have the cash flow to pay for essentials like food and rent while you negotiate.

3. Negotiate a Partial Release

The CRA wants their money, but they generally don’t want you to become homeless or lose your job.

- The Negotiation: Offer a lump-sum good faith payment in exchange for an immediate partial release of the freeze.

- The 2026 Requirement: To unfreeze the account completely without paying the full balance, the CRA will usually demand a Full Financial Disclosure. This means you’ll have to show them exactly what you earn, what you own, and what you spend.

4. Use Home Equity to Kill the Debt

If you owe $50,000 and the CRA has frozen your $5,000 savings account, you are still $45,000 in the hole and your credit is being destroyed every day.

- The LendingMoney.ca Solution: If you have equity in your home, we can often secure an Emergency Equity Loan in as little as 48–72 hours.

- The Result: We pay the CRA in full. The CRA then issues a Statutory Discharge to your bank. Your accounts are unfrozen, your “Super Lien” risk is gone, and you move from a high-stress government debt to a manageable mortgage payment.

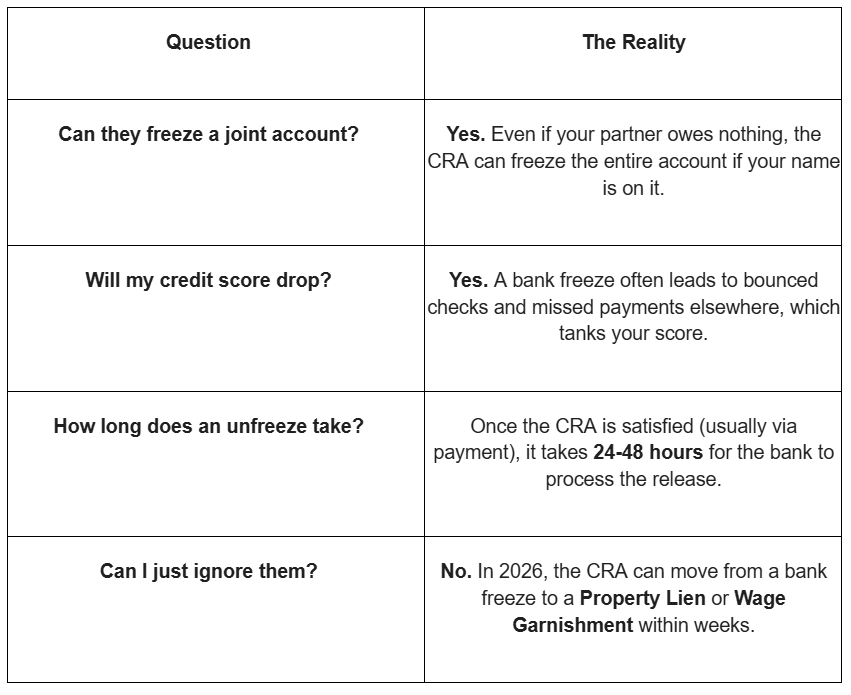

Frozen Account FAQ (2026)

| Question | The Reality |

| Can they freeze a joint account? | Yes. Even if your partner owes nothing, the CRA can freeze the entire account if your name is on it. |

| Will my credit score drop? | Yes. A bank freeze often leads to bounced checks and missed payments elsewhere, which tanks your score. |

| How long does an unfreeze take? | Once the CRA is satisfied (usually via payment), it takes 24–48 hours for the bank to process the release. |

| Can I just ignore them? | No. In 2026, the CRA can move from a bank freeze to a Property Lien or Wage Garnishment within weeks. |

We Pull the Emergency Brake

At LendingMoney.ca, we see a frozen account as a symptom of a larger problem. We don’t just want to unfreeze your money; we want to fix your financial structure so this never happens again. Our Credit Rehabilitation programs start by clearing your government debt so you can breathe again.

Are you staring at a $0.00 balance because of the CRA? [Connect with an Arrears Specialist] at LendingMoney.ca right now. We’ll look at your equity and find the path to unfreezing your life.