A private mortgage is often described as a “bridge.” But a bridge is only useful if it leads somewhere. If you are in a private mortgage in 2026, your primary goal is to use this 12-month window to rehabilitate your credit so you can “graduate” to a lower-interest bank or B-lender.

At LendingMoney.ca, we don’t want you to stay in a private loan forever. We want to help you fix the issues that put you there in the first place. Here is your month-by-month guide to Credit Rehabilitation while using a private mortgage.

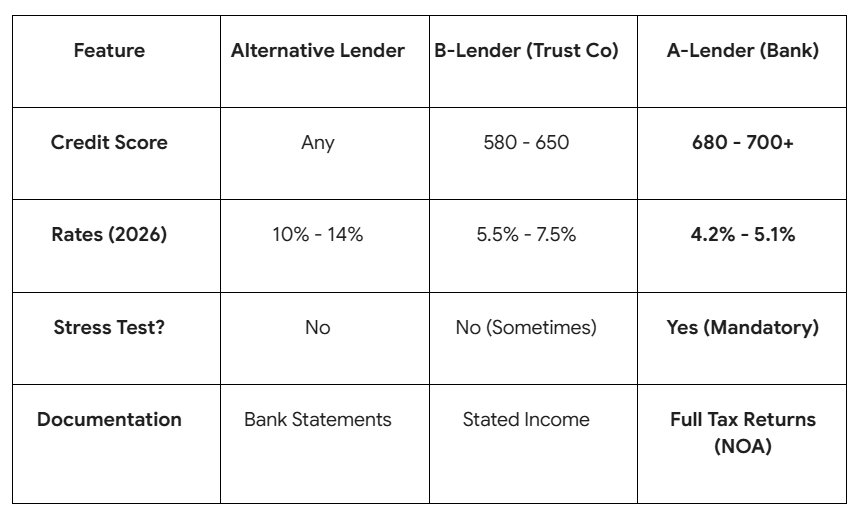

1. The Private Mortgage Reporting Reality

In 2026, most individual private lenders do not report to Equifax or TransUnion.

- The Problem: Even if you make every payment on time for a year, your credit score might not go up because the bureaus don’t see the “good behavior.”

- The Hero Move: You must focus on your other tradelines. Since the mortgage isn’t helping your score, your credit cards, car loans, and phone bills have to do the heavy lifting.

- The Catch: While private lenders don’t report the “good,” they will certainly report the “bad” if they have to take legal action (Power of Sale). On-time payments are mandatory to protect your equity.

2. Eliminate “R9” and “R7” Ghost Debts

If you took a private mortgage to consolidate debt, you likely have old collections (R9) or settled accounts (R7) on your report.

- The Strategy: Use a small portion of your mortgage “holdback” or savings to pay off any remaining small collections.

- The 2026 Rule: A “Paid Collection” is significantly better than an “Active Collection” when applying for a B-Lender. It shows the underwriter that you have cleared the wreckage of the past.

3. The 10% Utilization Rule

The fastest way to jump your score while in a private mortgage is to change how you use your credit cards.

- The Math: If you have a $5,000 limit, never let the balance exceed $500 (10%) on the day the statement is produced.

- The Hero Move: In 2026, many apps allow “Real-Time Reporting.” Pay your credit card balance every time you get paid (bi-weekly) rather than once a month. This keeps your “average utilization” extremely low, which is the #1 “Point Booster” in the Equifax algorithm.

4. Add Two “Fresh” Tradelines

To get back to a traditional bank, you usually need a “2-2-2” profile: 2 years of history on 2 lines of credit with at least $2,000 limits.

- The Strategy: If your old cards were closed during a Consumer Proposal or bankruptcy, open two new Secured Credit Cards immediately.

- The Timeline: By the time your 12-month private mortgage is up, these cards will have 12 months of perfect history, making you an ideal candidate for a B-Lender (Trust Company).

5. Diversify with a “Credit Builder” Loan

In 2026, lenders like seeing a mix of credit types. If you only have credit cards, your score will plateau.

- The Move: Open a small Installment Credit-Builder Loan (like those offered by Nyble or KOHO).

- How it works: You pay a small amount monthly ($20–$50), and they report it as a “Personal Loan” payment. This adds “Credit Mix” to your profile, which accounts for 10% of your total score.

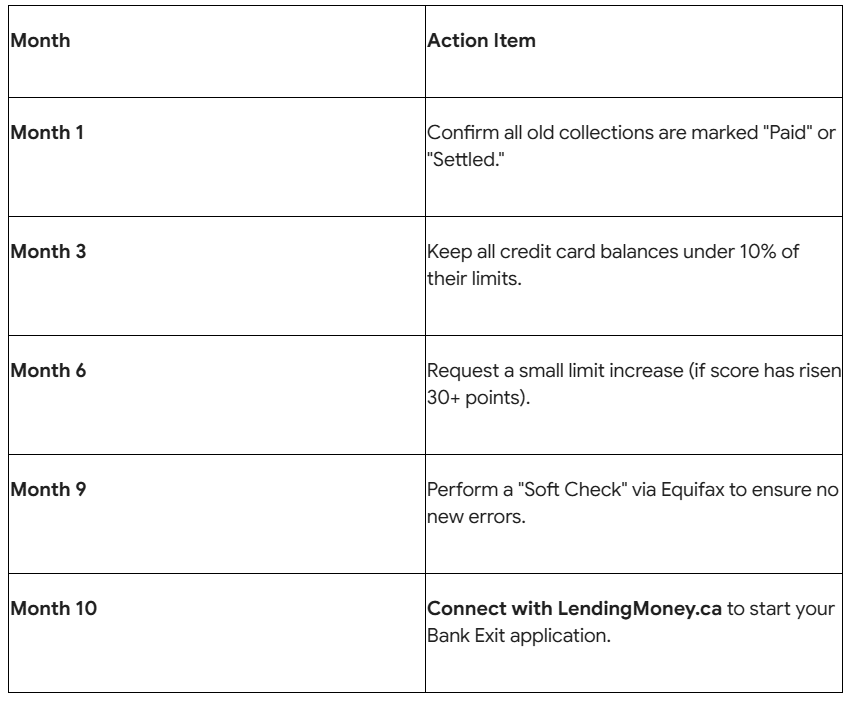

Your 12-Month Credit Rehab Calendar

The Goal: Graduation Day

Fixing your credit while in a private mortgage requires discipline. You are paying a higher interest rate now so that you never have to pay it again. At LendingMoney.ca, we provide the tools and the coaching to ensure that when your private term ends, you are ready for a prime-rate mortgage.

Currently in a private mortgage and want to see your “Graduation Date”? [Get a Free Credit Rehabilitation Roadmap] from LendingMoney.ca today and let’s start moving you back to the bank.

Read blog – Breaking the Cycle: A Guide to Loans for Debt Consolidation with Poor Credit