It is April 2026, and for many Canadians, the arrival of a Notice of Assessment (NOA) from the CRA brings a stomach-turning surprise: a balance owing that wasn’t in the budget.

Whether it’s due to a self-employment tax miscalculation, a clawback of benefits, or a simple filing error, unexpected tax debt is a financial fire that needs to be put out quickly. In 2026, the CRA’s interest rate on overdue tax sits at 7% compounded daily, meaning your debt grows every single morning you leave it unpaid.

At LendingMoney.ca, we specialize in Credit Rehabilitation. We know that tax debt is the #1 hurdle to getting a traditional mortgage or car loan. Here is what you need to do if you find yourself with an unexpected CRA bill this tax season.

1. Don’t Ghost the CRA (File Anyway!)

The biggest mistake homeowners make is delaying their tax filing because they know they can’t pay.

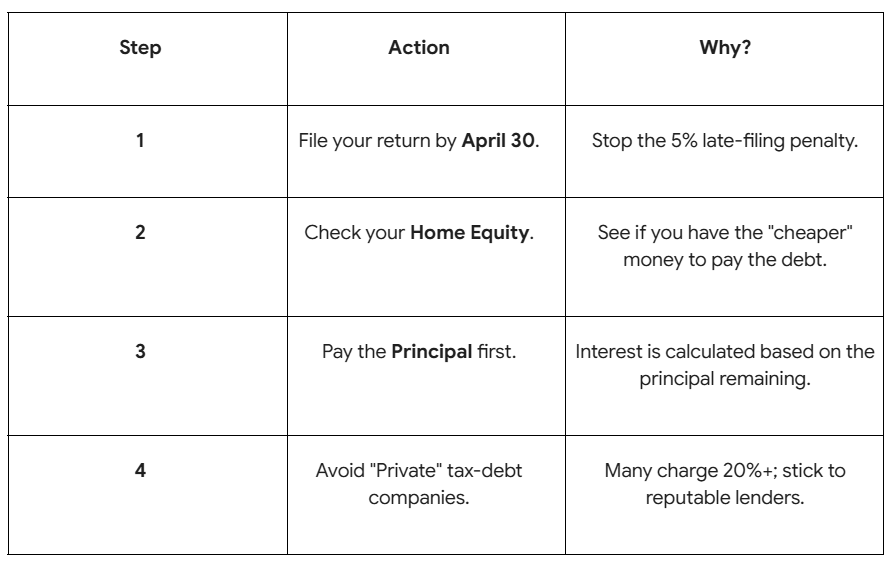

- The Penalty: If you file late and owe money, the CRA hits you with an immediate 5% penalty on the balance, plus 1% for every month you are late.

- The Hero Move: File your taxes by the April 30th deadline (or June 15th if self-employed), even if you have $0 in the bank. Filing on time stops the late-filing penalty, leaving you with only the interest to manage.

2. Request a Payment Arrangement

If you can pay off the debt within a few months, the CRA is surprisingly reasonable-if you talk to them first.

- TeleArrangement: You can call the CRA to set up a “Pre-Authorized Debit” plan to pay your debt over time (usually up to 12 months).

- The Reality: While this stops aggressive collection action (like wage garnishing), the 7% daily interest continues to run. You are essentially taking a high-interest loan from the government.

3. Leverage Your Home Equity (The Interest “Hack”)

If your tax debt is substantial ($10,000 to $100,000+), using a payment plan is often the most expensive way to handle it.

- The 2026 Math: * CRA Interest: ~7% daily compounded (effectively much higher).

- Home Equity Loan: monthly compounded.

- The Move: Using a Home Equity Line of Credit (HELOC) or a Second Mortgage from LendingMoney.ca to pay the CRA in full immediately. You swap “predatory” daily interest for a stable, lower-rate mortgage payment. Plus, the CRA is paid, which clears your name for future bank approvals.

4. The Taxpayer Relief Hail Mary

Did your debt happen because of a serious illness, a death in the family, or a natural disaster?

- The Option: You can apply for Taxpayer Relief (Form RC4288).

- What it does: If approved, the CRA can waive the penalties and interest on your account.

- The Catch: They almost never waive the principal tax you owe. You still need a plan to pay the core debt, which is where an equity-based “bridge” loan becomes essential.

5. Why Banks Say No to Tax Debt

If you walk into a “Big Six” bank with a $20,000 CRA bill, they will likely decline your loan.

- The Reason: Banks view CRA debt as a “Super Lien.” They know the government can freeze your accounts or put a lien on your house that takes priority over the bank’s own mortgage.

- The LendingMoney.ca Solution: As an Alternative Lender, we aren’t afraid of CRA debt. We provide the funds to pay the CRA today, so your credit can begin its Rehabilitation tomorrow. Once the CRA is out of the picture, the big banks will be happy to talk to you again in a year.

CRA Debt Survival Checklist (April 2026)

Turn Your Tax Debt into a Strategy

Unexpected debt to the CRA is a crisis, but it’s also an opportunity to restructure your finances. By using your home equity to clear the slate, you protect your credit score, stop the daily interest bleed, and regain control of your financial future.

Stunned by your 2026 Tax Bill? [Connect with a Financial Hero] at LendingMoney.ca. We’ll look at your home equity and find a way to pay the CRA so you can get back to what matters.

Read blog –How to Pay CRA Debt With Home Equity