If you’ve been struggling with unmanageable debt, you’ve likely heard the term Consumer Proposal. In 2026, more Canadians than ever are choosing this legal pathway over bankruptcy to find relief from high-interest credit cards, tax debt, and unsecured loans.

But what exactly is a Consumer Proposal, and is it the right “hero move” for your financial journey? At LendingMoney.ca, we believe that understanding your options is the first step toward Credit Rehabilitation. Here is everything you need to know about this powerful debt-settlement tool.

What is a Consumer Proposal?

A Consumer Proposal is a formal, legally binding agreement between you and your unsecured creditors. Regulated under the Bankruptcy and Insolvency Act, it allows you to pay back a portion of what you owe- often as little as 20% to 50% – in exchange for full debt forgiveness on the remaining balance.

Unlike informal debt settlement schemes, a Consumer Proposal is a federal process administered by a Licensed Insolvency Trustee (LIT). It is designed to be a “win-win”: you get a monthly payment you can actually afford, and your creditors receive more money than they would if you filed for bankruptcy.

How Does a Consumer Proposal Work? (The 5-Step Process)

The process is structured to give you immediate relief while providing a clear exit strategy from debt.

- The Consultation: You meet with a Licensed Insolvency Trustee to review your finances. They determine if you are “insolvent” (unable to pay your debts as they come due) and if a proposal is your best option.

- The Filing: Your Trustee files the proposal with the government. The moment this happens, a Stay of Proceedings kicks in. This is your legal shield—it immediately stops all collection calls, interest charges, lawsuits, and wage garnishments.

- The 45-Day Voting Period: Your creditors have 45 days to review your offer. For the proposal to be accepted, a simple majority (51%) of your creditors (based on the dollar value of the debt) must vote “Yes.” Once the majority agrees, all your unsecured creditors are legally bound by the deal.

- The Repayment Phase: You make one fixed, interest-free monthly payment to your Trustee for a term of up to 5 years (60 months).

The Certificate of Full Performance: Once your payments are complete and you’ve attended two mandatory financial counseling sessions, you receive a certificate that legally discharges you from all debts included in the proposal.

What Debts Can You Include?

A Consumer Proposal is incredibly versatile. It covers almost all forms of unsecured debt, including:

- Credit Cards: Visa, Mastercard, Amex, and retail store cards.

- Lines of Credit: Both bank-issued and private unsecured lines.

- CRA Debt: Income tax arrears, GST/HST, and even CERB/CRB overpayments.

- Personal Loans: Including high-interest installment loans and payday loans.

- Student Loans: Provided you have been out of school for at least seven years.

Note: Secured debts, such as your mortgage or your car loan, stay outside the proposal. As long as you keep making those specific payments, you keep the assets.

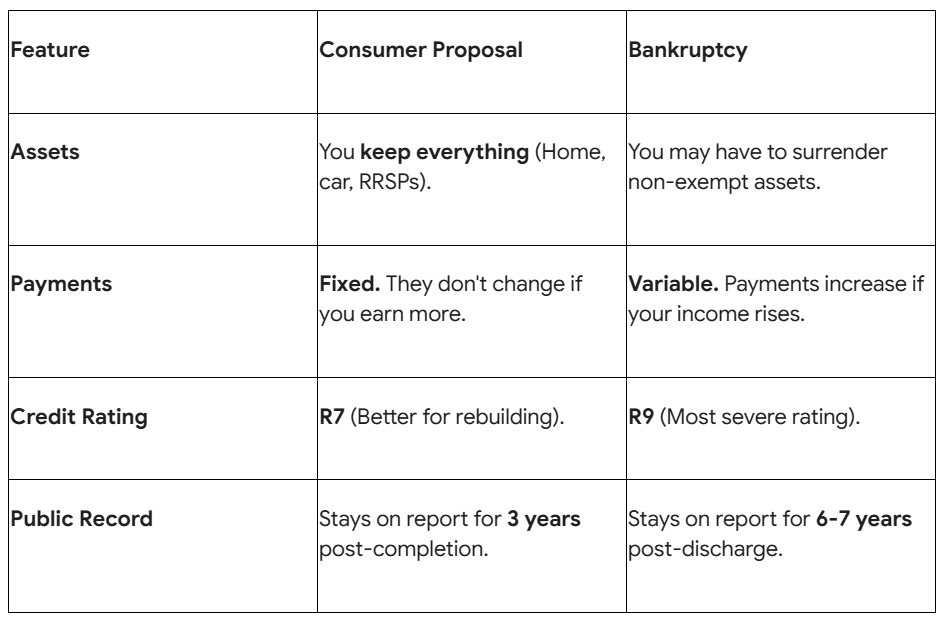

Why Choose a Consumer Proposal Over Bankruptcy?

In 2026, the “stigma” of insolvency is fading as more people realize that a Consumer Proposal is a proactive, responsible choice. Here is why it often beats bankruptcy:

Who Qualifies for a Consumer Proposal in Canada?

To file a Consumer Proposal in 2026, you must meet four main criteria:

- Insolvency: You owe more than you own, or you can no longer meet your monthly minimum payments.

- Debt Limit: Your total unsecured debt must be between $1,000 and $250,000 (excluding your mortgage). If you are filing as a couple, your joint limit is $500,000.

- Residency: You must live in Canada or own property here.

Ability to Pay: You must have a stable source of income (employment, pension, or self-employment) to support the monthly payments.

The Catch: What are the Drawbacks?

While a Consumer Proposal is a powerful tool, it isn’t a “get out of debt free” card. There are a few things to consider:

- Credit Impact: Your credit will be rated as an R7. While this is better than a bankruptcy’s R9, it will make it difficult to get traditional low-interest credit while the proposal is active.

- Public Record: Like all insolvency filings, it is a matter of public record, though it is rarely “advertised” outside of specific credit-search databases.

- Missed Payments: If you miss three monthly payments, your proposal is “annulled,” meaning the legal protection disappears and your creditors can come after you for the full original amount plus interest.

The LendingMoney Advantage: Post-Proposal Recovery

Filing a Consumer Proposal is only half the battle. The real goal is Credit Rehabilitation.

At LendingMoney.ca, we work with clients who are currently in or have recently completed a Consumer Proposal. While big banks might turn you away, we understand the 2026 lending landscape. We help you navigate the “rebuilding phase” with:

- Consolidation Strategies: Helping you manage your proposal payments more effectively.

- Rebuilding Tools: Introducing you to credit-building loans that report to the bureaus while your proposal is active.

- Bridge Financing: Providing the “hero” support you need to reach that Certificate of Full Performance faster.

Final Thoughts: Is It Time to Act?

If you are only making minimum payments and your total debt isn’t going down, you are essentially on a “treadmill” that is going nowhere. A Consumer Proposal allows you to step off that treadmill and start walking toward a debt-free life.

Ready to see if a Consumer Proposal is the “Hero Move” your family needs? [Connect with LendingMoney.ca] today for a no-judgment consultation and start your journey to a 700+ credit score.

Read blog – How to get a Second Mortgage With Bruised Credit