As we settle into 2026, the Canadian mortgage landscape has undergone a significant shift. Between the new OSFI (Office of the Superintendent of Financial Institutions) regulations and a stabilized but “stressful” interest rate environment, many borrowers are finding that the rules of the game have changed.

If you’ve recently been declined by a “Big Six” bank, it’s likely due to one of these top five reasons. Understanding these hurdles is the first step toward your Credit Rehabilitation and a successful approval with an alternative lender.

1. The Stress Test Ceiling (7.25%+)

Even though actual mortgage rates have stabilized, the Mortgage Stress Test remains the #1 reason for declines in 2026.

- The Reality: Federally regulated banks must test your ability to pay at either 5.25% or your contract rate plus 2%, whichever is higher.

- The 2026 Impact: With many contract rates sitting around 5.25%, you are effectively being “tested” at 7.25%.

- The Result: This inflated rate pushes your debt-service ratios over the limit, even if you can comfortably afford the actual monthly payment.

2. The Double-Counting Ban for Investors

A major change that took effect in January 2026 has blindsided many property investors.

- The Rule: OSFI has eliminated the practice of “double-counting” income. Previously, investors could use the same personal or rental income to support multiple mortgage applications.

- The Impact: Now, every property must “stand on its own.” If a rental property isn’t generating enough independent cash flow to cover its own mortgage and expenses, it will trigger a decline for any new applications. This has effectively cut the borrowing power of small investors by nearly 50%.

3. High Debt-to-Income (TDS/GDS) Ratios

In 2026, lenders have tightened their “Total Debt Service” (TDS) requirements.

- The Threshold: Most banks now strictly enforce a 42–44% TDS limit.

- The Culprits: It’s often not the mortgage that causes the fail—it’s the “small” stuff. A $600 car payment or $15,000 in credit card debt can “eat” $50,000 to $80,000 of your potential mortgage principal.

- The 2026 Shift: Lenders are now scrutinizing HELOCs and lines of credit more heavily, counting their full limits against you even if the balance is zero.

4. The CRA Debt Red Flag

As we move through the 2026 tax season, lenders are more focused on tax compliance than ever before.

- The Rule: If you owe money to the Canada Revenue Agency (CRA), most traditional banks will issue an automatic decline.

- The Reason: The CRA has “super-priority” status, meaning they can put a lien on your property that jumps ahead of the bank’s mortgage.

- The Solution: Many of our clients at LendingMoney.ca use an alternative “bridge” loan to pay off their CRA arrears first, clearing the path for a traditional mortgage approval 12 months later.

5. Low Property Appraisals

In 2026, the market has stabilized, but appraisers remain incredibly cautious.

- The Gap: If you buy a home for $800,000 but the bank’s appraiser says it’s only worth $750,000, the bank will only lend based on the lower number.

- The Consequence: You are suddenly responsible for coming up with the $50,000 difference in cash. If you don’t have it, the mortgage is declined for “insufficient collateral.”

- The 2026 Trend: This is especially common in “bidding war” scenarios where emotional buyers overpay beyond what the data-driven appraiser can justify.

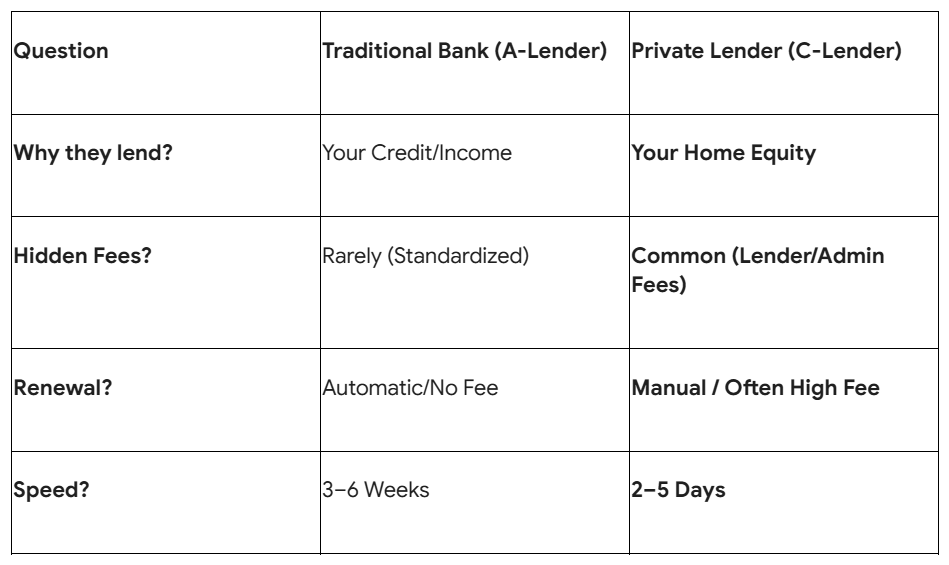

Moving from Declined to Approved

A decline in 2026 isn’t a dead end—it’s a signal to change your strategy. While a Big Bank might see a “fail,” a Financial Hero at LendingMoney.ca sees an opportunity for a workaround.

- We offer Alternative Solutions that don’t use the same rigid stress test.

- We allow “Stated Income” for self-employed individuals.

- We provide Equity-Based Lending that focuses on the value of your home rather than just your credit score.

Did a bank turn you down today? [Upload Your Decline Letter] to LendingMoney.ca and let us find the “Path to Yes” that the big banks missed.