For the self-employed entrepreneur in 2026, the traditional path to a loan is often blocked by a mountain of paperwork. While big banks are still obsessing over your Notice of Assessment (NOA) and “Net Income” after every possible deduction, LendingMoney.ca knows that your taxable income rarely tells your real story.

In the world of Credit Rehabilitation and alternative lending, your bank statement is no longer just a list of transactions-it is your most powerful financial asset. Here is why your cash flow is more important than your tax returns when it comes to securing an unsecured loan.

1. The Paperwork Gap: NOAs vs. Reality

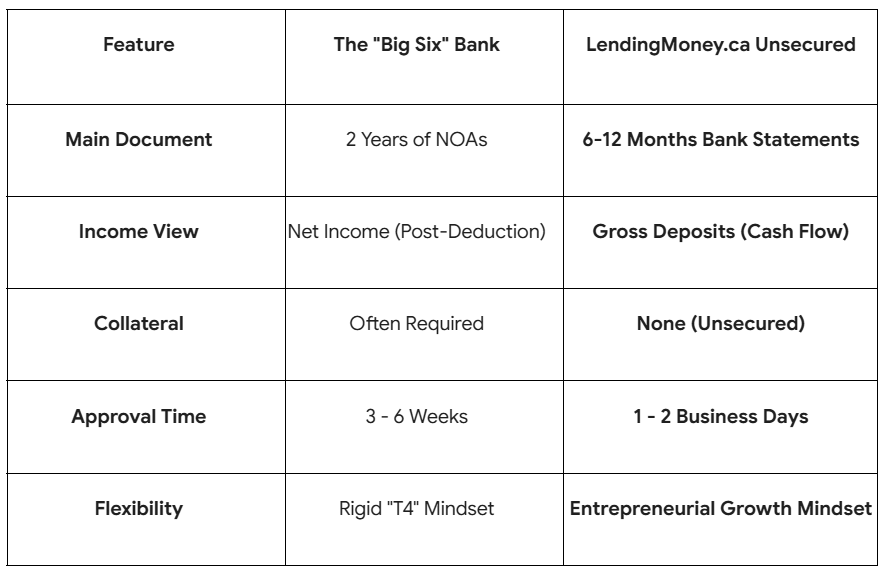

Traditional lenders have a “9-to-5” mindset. They want a T4 slip or a “Line 15000” on an NOA that shows a high personal income.

- The Problem: As a business owner, you likely use legal deductions to reduce your tax bill. While this is smart for your bottom line, it makes you look “broke” to a traditional bank.

- The 2026 Solution: At LendingMoney.ca, we don’t look at what you kept after taxes; we look at what you earned. By reviewing your 6 to 12 months of business bank statements, we see the true revenue your business generates. Your “Stated Income” backed by deposits is the key to unlocking an unsecured loan without the tax-man’s approval.

2. Cash Flow is Your Character

In 2026, the reliability of your deposits is a better indicator of your creditworthiness than a three-digit score.

- The “Stability” Signal: Lenders love seeing consistent, regular deposits into your business account. Whether you are a consultant with three main clients or a contractor with dozens of smaller jobs, your bank statement proves that you have the velocity of money needed to handle a monthly installment.

- The Hero Move: We use digital banking verification to “smooth out” your income. Even if your business is seasonal, your bank statements help us find an average that allows you to qualify for a loan that fits your lifestyle.

3. The Unsecured Freedom for Entrepreneurs

Most business loans in Canada require you to put up collateral – your equipment, your inventory, or even a lien against your personal home.

- Why “Unsecured” Wins: With an unsecured loan from LendingMoney.ca, your business assets remain yours. You are borrowing based on the strength of your income, not the value of your tools.

- The Strategy: This leaves your equipment “clean,” so if you need to lease a new truck or upgrade your tech later, those assets aren’t already tied up in a consolidation loan.

4. Speed: Funding at the Pace of Business

In 2026, opportunities move fast. If you need to buy inventory for a big contract or fix a critical piece of machinery, you can’t wait six weeks for a bank’s “Self-Employed Underwriting Department” to call you back.

- The LendingMoney.ca Advantage: Because we prioritize bank statements over deep-dive tax audits, we can often fund an unsecured loan in 24 to 48 hours.

- The Result: You get the capital you need to keep your business moving, using your own successful history as your primary reference.

Self-Employed Loan Comparison: 2026

5. Building Your B – Lender Bridge

Many of our self-employed clients use an unsecured loan as a stepping stone.

- The Step: If you want to buy a home or refinance your mortgage next year, having a perfect 12-month payment history on an unsecured installment loan is powerful.

- The Graduation: It proves to future “B-Lenders” (Trust Companies) that your business cash flow is stable and that you are a disciplined borrower.

Your Business, Your Rules

Don’t let a low “Net Income” on your tax return stop your growth. If your bank statements show a thriving business, you have all the collateral you need.

Ready to let your cash flow do the talking? [Apply for a Bank-Statement Loan] at LendingMoney.ca today. Let’s turn your business success into your next Financial Hero” moment.