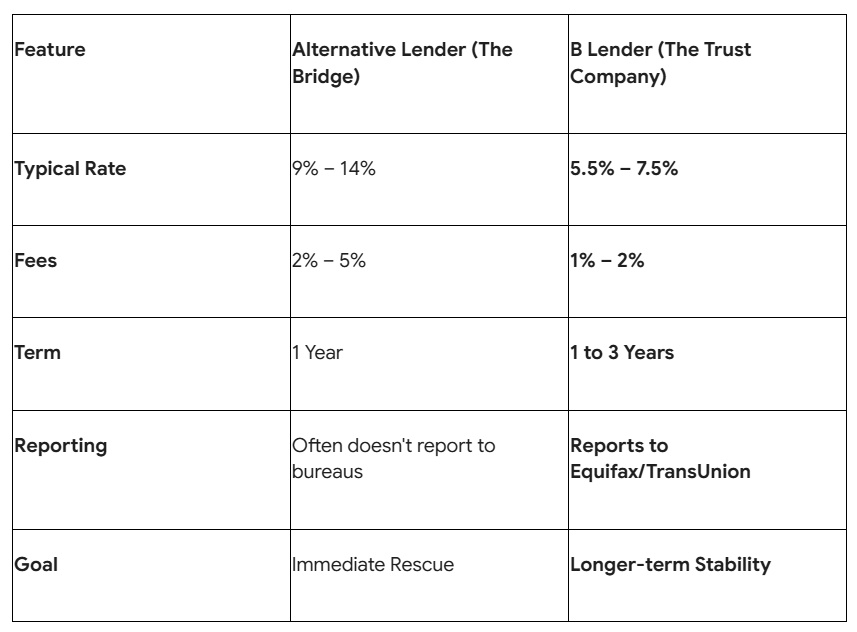

An alternative mortgage is a high-performance bridge, but it isn’t meant to be your forever home. B Lenders offer lower interest rates (often 3% to 5% lower than alternative rates) and longer terms, but they require a higher level of “financial hygiene.”

To make the jump, you need to prove to a Trust Company that the issues that led you to an alternative lender are firmly in the past.

1. The “600 Score” Benchmark

While LendingMoney.ca can work with almost any credit score by focusing on equity, B Lenders (Trust Companies) generally want to see a score of at least 550 to 600.

- The Strategy: Use the 12-month term of your alternative mortgage to aggressively rebuild. If you used your alternative loan to pay off collections, ensure those are now marked as “Paid” on your Equifax report.

- The Requirement: B Lenders look for “Re-established Credit.” This typically means having two new credit cards with at least a $2,000 limit, used responsibly for at least 6–12 months.

2. Clean Up the “Paper Trail”

B Lenders are regulated institutions, which means their underwriters are more detail-oriented than alternative lenders.

- The “No-Lates” Rule: To qualify for a Trust Company, you must show 12 months of perfect payments on your alternative mortgage. One single missed payment on your current mortgage can disqualify you from a B Lender for another year.

- The CRA Factor: If you had tax debt, the B Lender will require a Notice of Assessment (NOA) showing a $0 balance. They won’t “graduate” you until they see the government is fully out of the picture.

3. Shifting from “Equity” to “Income”

Alternative lenders often look at the value of your home first. B Lenders, however, care deeply about your Debt Service Ratios (GDS/TDS).

- The Math: A B Lender wants to see that your total housing costs and debts don’t exceed roughly 50% of your gross income.

- Self-Employed Hero Move: In 2026, B Lenders are very friendly to business owners. They will often use a “Stated Income” approach, where they look at your business bank statements to see your true cash flow rather than just the “Net Income” on your tax return.

4. The 20% Equity Requirement

To move into the B-Lending space, you almost always need to have at least 20% equity in your home (an 80% Loan-to-Value ratio).

- The Appraisal: Since 2026 property values have stabilized, your home may be worth more than when you started your alternative loan. A new, professional appraisal will prove to the Trust Company that their investment is safe.

The “Graduation” Comparison (2026)

5. Timing Your Exit

The best time to move is 3 to 4 months before your alternative mortgage matures.

- Avoid the Renewal: If you wait until the last minute, your alternative lender may charge you a renewal fee (1%–3%) just to stay for another year.

- The LendingMoney.ca Process: At the 9-month mark of your alternative loan, your Financial Hero will reach out to review your credit score. If you’ve hit the 600 mark, we will encourage you to start the application with the Trust Companies immediately to ensure a seamless “hand-off.”

You’ve Earned the Upgrade

Moving from an alternative lender to a B Lender is proof that your Credit Rehabilitation plan is working. It’s the moment your monthly housing costs drop and your financial future becomes more predictable.

Ready to see if you’re ready to “graduate” to a Trust Company? [Request a Graduation Audit] from LendingMoney.ca today. We’ll review your progress and find the B Lender that’s ready to welcome you back to institutional banking.