In the 2026 financial landscape, the Canada Revenue Agency (CRA) has moved toward “Aggressive Automation.” If you owe back taxes, the transition from a friendly reminder to a frozen bank account or a registered lien on your home can happen in weeks, not months.

When the CRA begins “Collection Action,” they are no longer asking for the money-they are taking it. This is where a Second Mortgage from LendingMoney.ca acts as the ultimate defensive shield. Here is how it works.

The CRA Shield: Using a Second Mortgage to Stop Collections

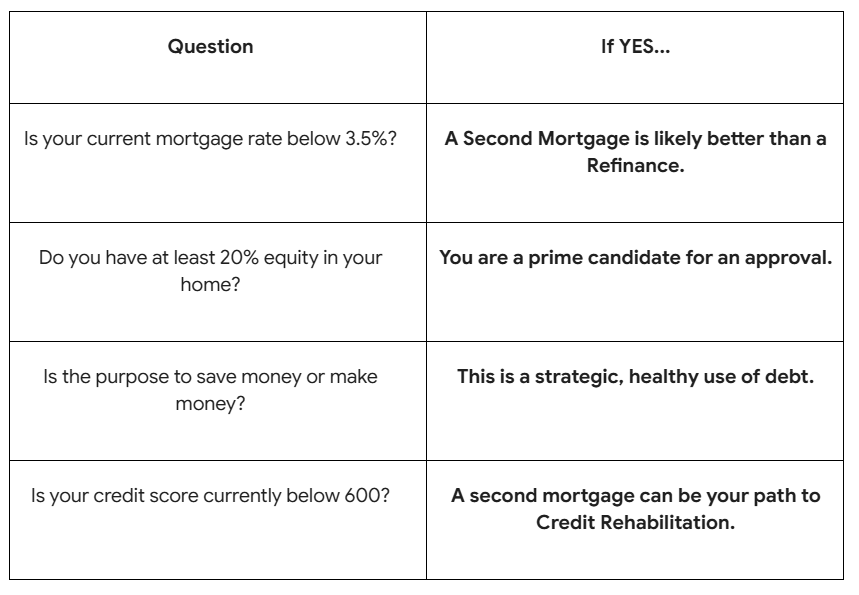

A Second Mortgage is a loan taken out against the equity in your home, sitting behind your primary bank mortgage. While a “Big Six” bank will almost never give you a loan to pay off tax debt, Alternative Lenders see it differently. We see your home equity as the key to your Credit Rehabilitation.

1. Why a Second Mortgage is Faster Than a Refinance

When the CRA is threatening to garnish your wages or freeze your accounts, you don’t have 30 days to wait for a bank appraisal and a full mortgage refinance.

- The Speed: A Second Mortgage can often be funded in 3 to 5 business days.

- The Strategy: You leave your low-rate first mortgage exactly where it is. You only borrow the specific amount needed to “kill” the CRA debt, minimizing your interest costs.

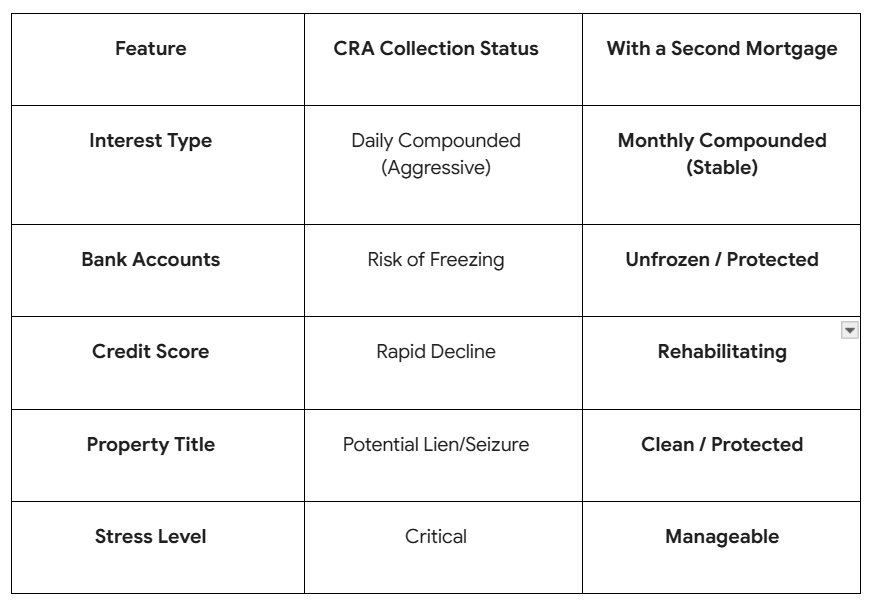

2. Stopping the Daily Compounding Interest

As of April 2026, the CRA’s prescribed interest rate is significantly higher than it was in the early 2020s.

- The Math: CRA interest is compounded daily. This means you are paying interest on yesterday’s interest, every single morning.

- The Move: A Second Mortgage from LendingMoney.ca uses monthly compounding. By paying the CRA in full with a Second Mortgage, you immediately stop the “interest snowball” and move to a predictable, stable monthly payment.

3. Preventing the Notice of Certification (Lien)

The moment the CRA registers a “Notice of Certification” against your property title, your credit score will plummet, and your traditional bank will likely flag your account for “Default.”

- The Hero Move: By using a Second Mortgage to pay the debt before the lien is registered, you keep your property title clean. This is vital for when your primary mortgage comes up for renewal-your bank will never know there was a tax issue, allowing you to renew at the best possible rates.

4. How the Payout Process Works

At LendingMoney.ca, we don’t just give you the cash and hope you pay the government. To protect you, the process is handled legally:

- The Approval: We approve your loan based on your home’s remaining equity.

- The Payout: Our lawyer sends the funds directly to the CRA on your behalf.

- The Proof: We obtain a “Statement of Account” showing a zero balance.

- The Release: If a freeze or garnishment was already in place, the CRA issues a formal release, and your financial life returns to normal within 48 hours.

Second Mortgage vs. CRA Collection Action

Reclaim Your Peace of Mind

Tax debt is the only debt in Canada that can bypass the normal court system to take your assets. Don’t wait for the CRA to make the first move. By using a Second Mortgage as a “Bridge Loan,” you take the power back, clear your name, and buy the time you need to get your finances in order.

Has the CRA sent you a Final Notice or a “Legal Warning”? [Get a Second Mortgage Quote] from LendingMoney.ca today. We specialize in fast, equity-based solutions that stop the taxman in his tracks.

Read blog – Unexpected Debt to the CRA? What can you do to pay what you owe?