Alternative mortgages and B-Lenders are fantastic “stabilization” tools. They gave you the cash to pay the CRA, consolidate debt, or bridge a gap in your self-employment income. But now that the dust has settled, you likely want the lowest possible interest rate and the prestige of a traditional bank mortgage.

Moving back to an A-Lender requires more than just a good score; it requires a “clean” financial story. Here are the five benchmarks you must hit to graduate in 2026.

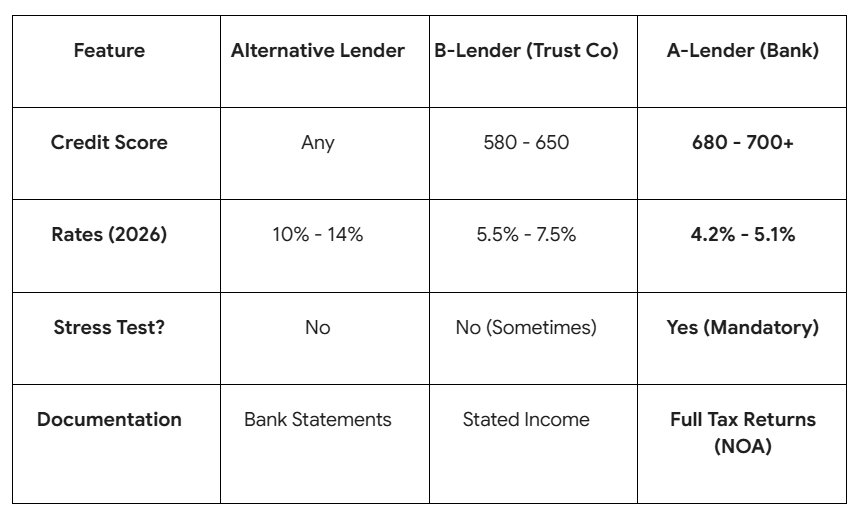

1. The 700 Club: Your New Credit Target

While you can get a B-Lender mortgage with a 600 score, the “Big Banks” in 2026 generally look for a minimum of 680, with 700+ being the “Golden Ticket” for the best advertised rates.

- The Requirement: You need a “clean” credit bureau for the last 24 months. This means zero late payments on any credit card, car loan, or phone bill since you started your alternative mortgage.

- The “Tradeline” Rule: Banks want to see at least two active credit cards with limits over $2,000, both with a history of at least two years.

2. The NOA Standard: Tax Transparence

This is often the biggest hurdle for entrepreneurs and those who previously owed the CRA.

- The Rule: An A-Lender will require your two most recent Notices of Assessment (NOAs). They must show that you owe $0.00 to the government.

- The 2026 Shift: Banks are now using digital verification. They may ask for a “Proof of Income” statement directly from the CRA portal. If there is any hint of a payment plan or outstanding balance, the bank will decline the application immediately.

3. The Federal Stress Test (Guideline B-20)

When you are with an alternative lender or a private lender, you often don’t have to pass the federal stress test. To move back to a bank, you must pass it.

- The Math: In 2026, with the Bank of Canada policy rate near 2.25%, the “Benchmark” stress test is typically around 7.25%.

- The Goal: Your total housing costs (mortgage + taxes + heat) must not exceed 39% of your gross income, and your total debt (including car loans) must not exceed 44%.

4. Stability of Income

Banks love “T4” employees (salaried workers). If you are self-employed, graduating back to a bank is harder but not impossible.

- The 2-Year Average: The bank will take your “Line 15000” income from your last two years of tax returns and average them.

- The Hero Move: If your business has grown significantly, we at LendingMoney.ca advise you to package your corporate financial statements to show “add-backs”-proving your true earning power is higher than what you show the taxman.

5. Property Appraisal & Marketability

A-Lenders are the most conservative when it comes to the “collateral” (your house).

- The Inspection: If you used your alternative mortgage to fund renovations, the bank will want to see that those renovations are 100% complete. They will not take over a mortgage on a “construction zone.”

- Location: Banks prioritize properties in major urban centers. If your home is in a very remote area, graduating back to a Big Six bank may require a higher credit score or a lower Loan-to-Value (LTV) ratio.

The Graduation Roadmap (Alternative → B → A)

Why Use LendingMoney.ca for Your Final Leap?

Most people think they can just walk into their local bank branch once their credit is fixed. However, if that bank sees a history of a private mortgage on your title, they may still be hesitant.

At LendingMoney.ca, we know which A-Lender underwriters are the most flexible with “recovered” borrowers. We tell your story in a way that highlights your successful rehabilitation, ensuring the bank sees you as a low-risk, high-value client.

Are you ready to stop paying “alternative” rates and start paying “bank” rates? [Request a Bank-Ready Audit] from LendingMoney.ca today. We’ll verify your score, your ratios, and your NOAs to see if today is your Graduation Day.

Read blog- How to Pay CRA Debt With Home Equity