One of the most common myths in the 2026 mortgage market is that a low credit score is a “permanent no” for home financing. At LendingMoney.ca, we know that bad credit is often just a snapshot of a difficult moment-not a definition of your future.

While a traditional Big Six bank will almost always decline a second mortgage application if your score is below 650, the alternative and private lending markets work differently. They focus on the asset (your home) rather than just the score.

Here is your 2026 guide on how to qualify for a second mortgage, even if your credit has seen better days.

1. The Golden Rule: Equity is King

In the world of bad credit second mortgages, your home equity is your strongest advocate. Lenders in 2026 categorize risk by LTV (Loan-to-Value).

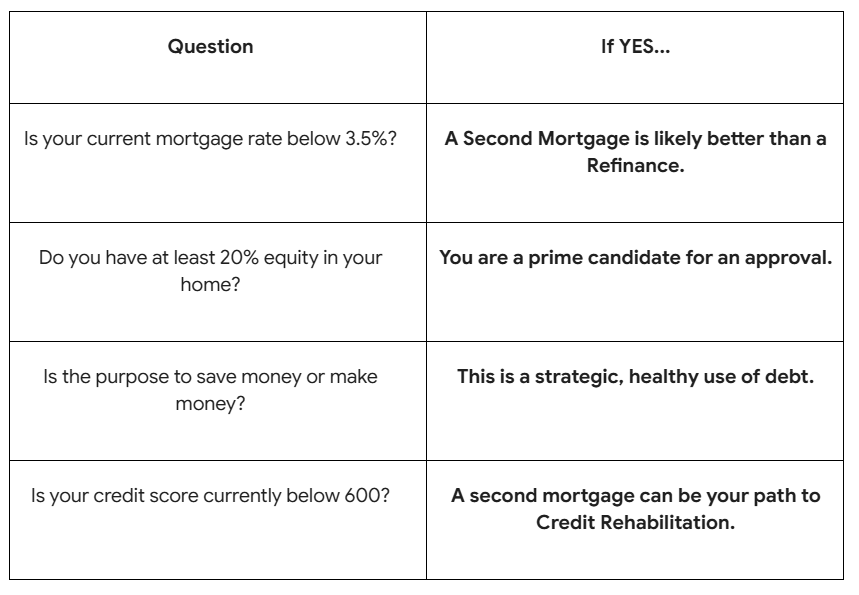

- The Threshold: To qualify with bruised credit, most alternative lenders want to see a combined LTV (your first mortgage + the new second mortgage) of 75% to 80% or less.

- The Math: If your home is worth $600,000 and you owe $350,000 on your first mortgage, you have $250,000 in equity. A lender will likely let you borrow up to a total of $480,000 (80% of value). This leaves you with $130,000 available for a second mortgage, regardless of your credit score.

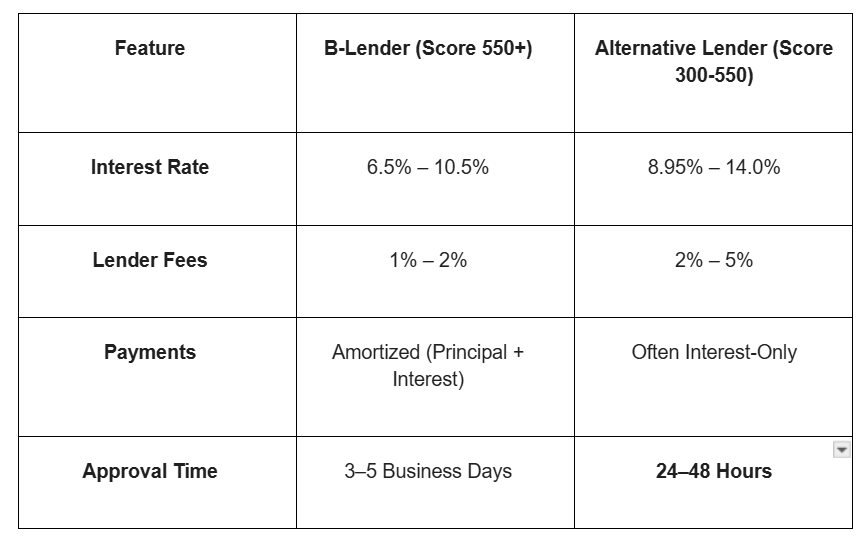

Choosing the Right Path: B Lenders vs. Alternative Solutions (2026)

Depending on your specific Financial Hero journey, we will steer you toward one of these two paths. Both are effective, but they serve different needs:

- B Lenders (Trust Companies): These are federally or provincially regulated institutions like Community Trust, Home Trust or Equitable Bank. They are a step above a traditional bank but more flexible. They can work with scores as low as 550–600. They still require standard income verification (though they are more lenient with self-employed “stated” income) and typically offer 1-to-3-year terms.

- Alternative Lenders (LendingMoney.ca): This is where we excel. As an alternative lender, we often look at Equity-First solutions. We can approve second mortgages that B Lenders might find too complex, such as those involving active CRA debt, recent consumer proposals, or properties with unique valuations. We focus on the asset and the exit strategy, providing the “Bridge” you need when the Trust Companies aren’t an option.

3. The Marketability Factor (Revised)

Because an Alternative Lender is relying on your house as their primary security, the condition and location of your property are the most important factors.

- Urban Hubs: It is much easier to secure an alternative second mortgage in high-liquidity markets like Mississauga, Toronto, or Ottawa.

- The “Hero” Appraisal: We use professional appraisals to prove to our lending partners that your home is a solid investment. A clean, well-maintained home allows us to stretch the LTV (Loan-to-Value) higher, giving you more cash to fix your credit.

4. Prove Your Affordability (The Alternative Way)

Even without a high credit score, we need to show that this loan is a solution, not a burden.

- Bank Statement Underwriting: Unlike the big banks that demand a T4, LendingMoney.ca often uses 6-12 months of bank statements to verify your true cash flow. This is perfect for entrepreneurs who have high revenue but many tax write-offs.

- The Exit Strategy: This is the most important part of our process. We don’t just give you a second mortgage; we build a plan to move you back to a B Lender or an A Lender within 12 to 24 months.

You are More Than a Number

A low credit score shouldn’t lock you out of your own home’s wealth. Whether you’re dealing with the aftermath of a business failure or just a rough year, your equity is your ticket to a fresh start.

Don’t let a “No” from the bank or a Trust Company stop you. [Get an Alternative Equity Review] from LendingMoney.ca today. Let our Financial Heroes show you how your home can fund your comeback.

What to Expect: Bad Credit Second Mortgage Terms (2026)

5. The Credit Rehab Exit Strategy

At LendingMoney.ca, we never want you to stay in a high-interest second mortgage forever. When we help you qualify with bad credit, we build in an Exit Strategy.

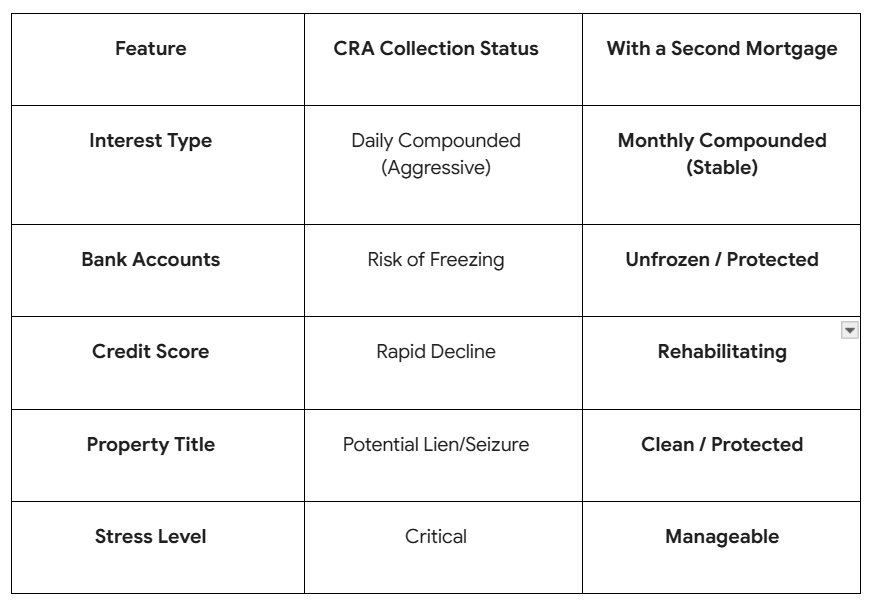

- Step 1: Use the funds to pay off the high-interest collections and maxed-out cards that are tanking your score.

- Step 2: Make perfect payments on the new second mortgage for 12 months.

- Step 3: Once your score bounces back to 680+, you can refinance both mortgages back into a single, low-rate bank mortgage.

You are More Than a Number

A low credit score shouldn’t lock you out of your own home’s wealth. Whether you’re dealing with the aftermath of a business failure or just a rough year, your equity is your ticket to a fresh start.

Don’t let a “No” from the bank stop you. [Get a Confidential Equity Review] from LendingMoney.ca today. Let our Financial Heroes show you how your home can fund your comeback.

Read Blog – How a CRA Lien Affects Your Mortgage Renewal