Being single gives you a unique advantage in the 2026 real estate market: Agility. You don’t need to worry about school zones or extra bedrooms for a growing family. You can focus entirely on location, appreciation, and resale value.

1. Location: The Walk Score ROI

In 2026, the value of a condo is tied directly to its proximity to transit and “lifestyle hubs.”

- The Strategy: Look for “Transit-Oriented Communities” (TOCs) along the GO expansion lines or the Ontario Line.

- The Hero Move: A smaller unit in a prime, walkable location will almost always appreciate faster and be easier to sell than a larger unit in a “sleeper” suburb. As a bachelor, you can sacrifice square footage for a 10-minute commute and better nightlife.

2. The Den Advantage: Future-Proofing for 2026

If your budget allows, prioritize a 1-bedroom plus den over a standard 1-bedroom.

- Why? In the 2026 hybrid-work economy, a dedicated office space is a non-negotiable for most buyers.

- The Resale Edge: When you’re ready to move on, that “den” makes your bachelor pad attractive to young couples who need a nursery or a remote workspace, doubling your pool of potential buyers.

3. High-Ratio Leverage: The 5% Entry

Many single men assume they need a 20% down payment to avoid “wasting money” on mortgage insurance.

- The 2026 Reality: With home prices stabilizing, the cost of waiting to save another $50,000 often exceeds the cost of the CMHC premium.

- The Strategy: Use the new 2026 $1.5M high-ratio ceiling to get in with as little as 5% down. This keeps your cash liquid for other investments or a “Safety Net” fund while you let the market do the heavy lifting for your net worth.

4. Understanding the Carry (Maintenance Fees)

The biggest threat to a bachelor’s budget isn’t the mortgage; it’s the Condo Fees.

- The Red Flag: Avoid buildings with “luxury” amenities you won’t use (like bowling alleys or valet parking). These drive up fees without adding equal value to your resale price.

- The Smart Buy: Look for “Boutique” buildings or well-managed older towers where the fees are stable and include utilities like heat and water.

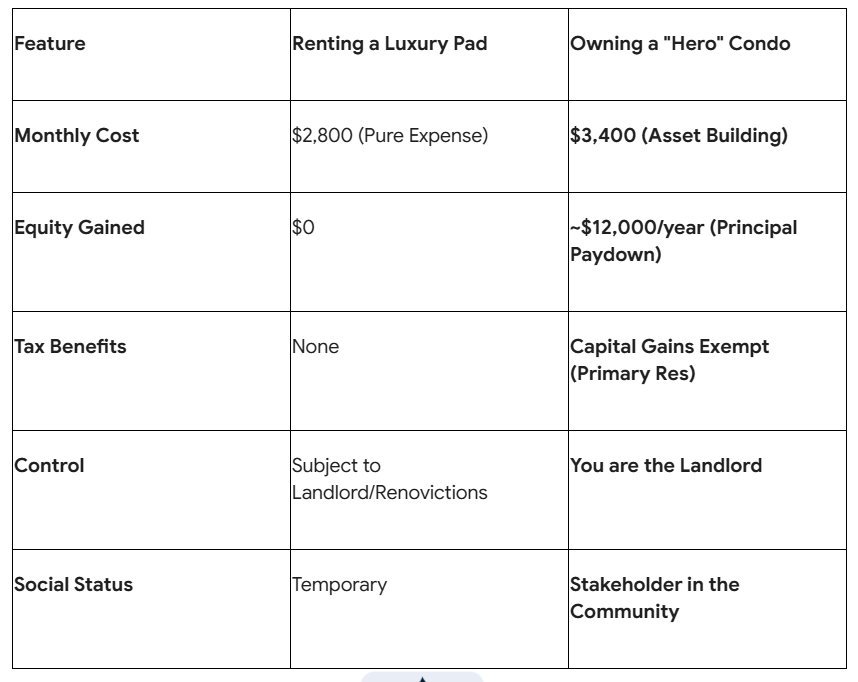

The Bachelor’s Build vs. Buy 2026 Comparison

5. The Bachelor-to-Landlord Pipeline

The best part about a bachelor pad is that it’s the perfect first rental property.

- The Exit Strategy: In 5 years, when you’re ready for a house with a yard, you don’t necessarily have to sell the condo.

- The Move: At LendingMoney.ca, we can help you refinance your condo to pull out equity for your next down payment, keeping the condo as a cash-flowing rental asset. This is how you start your real estate empire.

Your First Move is the Most Important

In 2026, the “Bachelor Pad” isn’t a lifestyle choice-it’s a financial launchpad. Don’t wait for a partner or a “perfect” time. The best time to buy real estate was 10 years ago; the second best time is today.

Ready to stop paying your landlord’s mortgage? [Request a Bachelor Pad Feasibility Study] from LendingMoney.ca today. Let’s look at your income, your FHSA, and the best 2026 condo markets to get you started.