If you’ve been working to build your credit, you’ve likely heard the advice: “Keep your credit card balances below 30% of your limit.” It sounds like a simple rule of thumb, but it’s actually one of the most powerful “hacks” in the financial world. At LendingMoney.ca, we see many clients with high incomes who are baffled as to why their credit score isn’t perfect. Often, the culprit isn’t missed payments-it’s high credit utilization.

What is Credit Utilization?

Your Credit Utilization Ratio is a measure of how much of your available revolving credit (credit cards and lines of credit) you are actually using.

The formula is simple:

Total Balances÷Total Credit Limits=Utilization Ratio

Example: If you have a credit card with a $10,000 limit and you currently owe $4,500, your utilization is 45%.

Why 30% is the Magic Number

Credit scoring models (like those used by Equifax and TransUnion) view credit utilization as a reflection of your financial stability.

- Below 30%: You are seen as someone who uses credit as a convenience rather than a necessity. Lenders view this as low-risk behavior.

- Above 30%: Lenders begin to wonder if you are relying on credit to cover your monthly living expenses. Your score will start to dip.

- Above 70%: This is the “danger zone.” Your score can take a significant hit, and automated banking systems may start flagging you as a high-risk borrower.

The “Exceptional Zone:

While 30% is the threshold for “good” credit, those with exceptional credit scores (800+) typically maintain utilization ratios below 10%.

The Reporting Date Trap

Here is a mistake that trips up even the most diligent budgeters: Credit card companies report your balance to the bureaus on your statement date, not your payment due date.

If you spend $5,000 on a $10,000 limit card throughout the month and then pay it off in full on the due date, your credit report will still show that $5,000 balance for that month.

The Strategy: If you want to optimize your score, make a “mid-cycle” payment a few days before your statement closing date. This ensures that a lower balance is reported to the credit bureaus, instantly boosting your utilization ratio.

How to Fix High Utilization (When You Don’t Have the Cash)

If you are already over 30% and don’t have the extra cash to pay it off, you might feel stuck. This is where debt consolidation becomes a strategic play:

- The Consolidation Sweep: By using a 2nd Mortgage to pay off your high-interest credit card debt, you immediately bring your utilization from, say, 80% down to 0%.

- The Instant Score Jump: Because credit utilization is a “snapshot” metric, your score can reflect this improvement as soon as the balances are updated-often within 30 to 60 days.

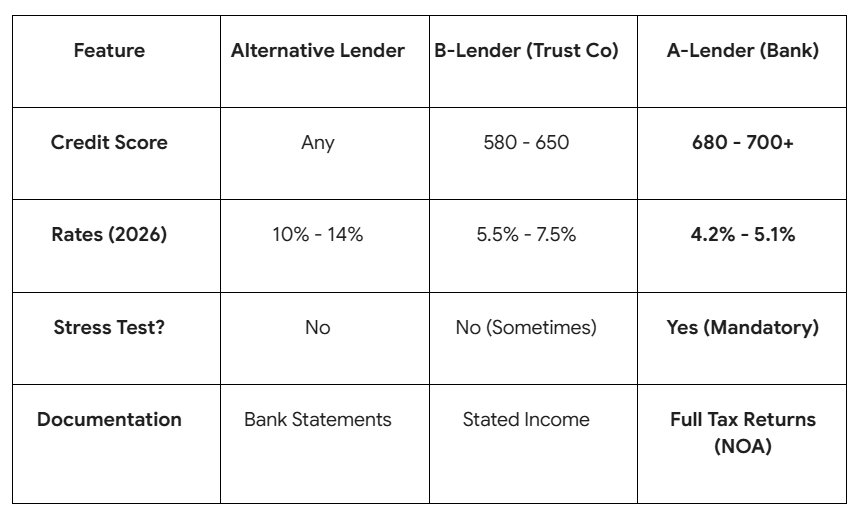

- The Path to “A-Lending”: Once your score jumps, you are no longer viewed as a “high-risk” borrower. You can then apply for lower-interest products, making it easier to keep your debt under control in the future.

Don’t Let a Ratio Hold You Back

Your credit score is your financial resume. If your utilization is high, you are effectively telling lenders that you are stressed and over-extended, even if you are making every payment on time.

Are you ready to see what your credit score could be if your utilization was lower?

[Request Your Free Credit & Debt Audit]

We’ll show you exactly how debt consolidation can wipe out your balances, drop your utilization to 0%, and help you reach that “Exceptional” credit score range.