For many Canadians, the debt spiral feels like a trap with no exit. High-interest credit cards, unexpected medical bills, or a sudden change in employment can lead to missed payments, which in turn causes credit scores to plummet. Once your credit score hits a certain threshold, traditional banks often stop listening.

At LendingMoney.ca, we believe your past doesn’t have to define your future. If you are searching for a loan to consolidate debt with poor credit, you aren’t just looking for money – you’re looking for a strategy. This guide breaks down how debt consolidation works, why your credit score isn’t the only factor that matters, and how you can reclaim your financial freedom.

What is Debt Consolidation?

At its core, debt consolidation is the process of taking out one new loan to pay off several smaller, high-interest debts. Instead of managing five different due dates and five different interest rates, you have one predictable monthly payment.

For those with poor credit, the primary goal of consolidation is twofold:

- Lowering the Cost of Borrowing: Swapping 29.99% credit card interest for a lower installment loan rate.

- Credit Rehabilitation: Streamlining payments so you never miss a due date again, which is the fastest way to boost your score.

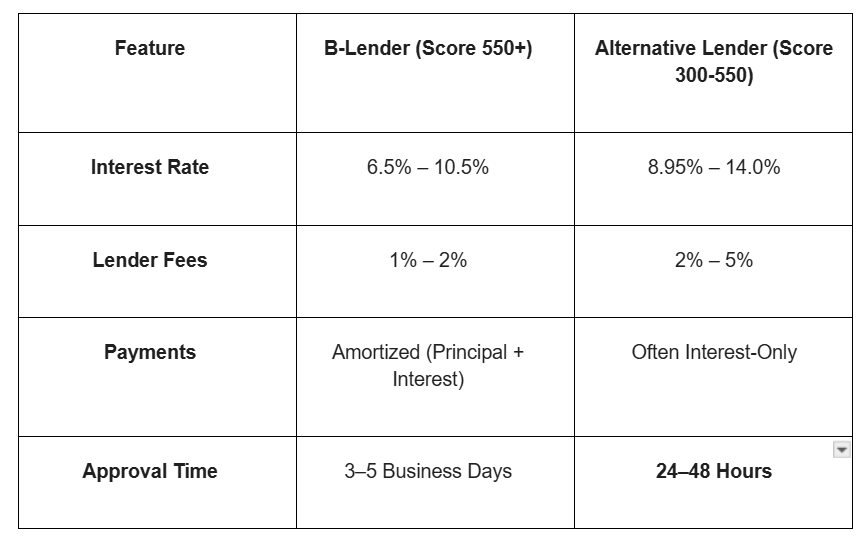

Can You Really Get a Consolidation Loan with Poor Credit?

The short answer is yes. While traditional “Big Five” banks rely almost exclusively on automated credit scores, alternative lenders and private firms look at a broader financial picture.

Why Banks Say No

Traditional lenders use rigid “risk models.” If your score is below a certain number (typically 600–650), their system automatically flags you as high-risk, regardless of your current income or your commitment to change.

Why LendingMoney.ca Says Yes

We focus on Credit Rehabilitation. We look at your current cash flow, your employment stability, and your specific financial goals. We understand that life happens. Our “Hero” approach means we look for reasons to fund you, not reasons to turn you away.

The Benefits of Consolidating Debt

When you secure a loan to consolidate debt with poor credit, the immediate relief is often emotional, but the long-term benefits are purely mathematical.

1. Immediate Interest Savings

If you are carrying a balance on three credit cards at 19% -29% interest, a significant portion of your monthly payment is simply feeding the beast- it never touches the principal balance. By consolidating into a single loan with a fixed term, more of your money goes toward actually erasing the debt.

2. A Boost to Your Credit Score

Credit utilization (how much of your available credit you are using) makes up about 30% of your credit score. When you use a consolidation loan to pay off “maxed-out cards, your utilization drops to zero. This often results in a significant “point jump” in your credit score within 30 to 60 days.

3. Direct Creditor Payment

One of the most effective ways to consolidate is through Direct Creditor Payment. At LendingMoney.ca, we can handle the logistics for you, paying your high-interest creditors directly so the debt is cleared immediately. This removes the temptation to spend the loan money elsewhere and ensures the “slate is wiped clean” on day one.

Types of Loans for Poor Credit Consolidation

Depending on your situation, there are several paths you can take:

Unsecured Personal Loans

These are the most common. They don’t require collateral (like a house or car). They are granted based on your income and your ability to manage the new payment. These are ideal for debts ranging from $500 to $15,000.

Secured Loans or Home Equity

If you are a homeowner, you may have access to much larger sums at lower rates by using the equity in your home. This is a powerful tool for major debt overhauls, allowing for much lower monthly payments over a longer term.

Private Lending

Private lenders often have the most flexibility. They are “real people” looking at real situations, making them a top choice for Canadians who have been through bankruptcy or consumer proposals.

Step-by-Step: How to Consolidate Your Debt

If you’re ready to take the first step in your financial journey, here is how the process works at LendingMoney.ca:

- The Quick Application: Spend five minutes on our secure portal. We ask about your income and the debts you want to crush.

- The Strategy Session: We don’t just send an automated email. We look at your path to rehabilitation. We determine which debts are hurting your score the most and build a plan to pay them off.

- Fast Funding: Once approved, we move quickly. In many cases, your creditors can be paid, or your funds can be deposited, within 24 to 48 hours.

- One Simple Payment: You stop worrying about five different apps and passwords. You make one affordable payment that fits your budget.

Common Myths About Poor Credit Loans

Myth #1: Applying will ruin my credit score.

While a “hard pull” can take a few points off, the long-term gain of paying off maxed-out cards far outweighs the temporary dip of an inquiry.

Myth #2: The interest rates are too high.

“High” is relative. If a consolidation loan is 15% but it’s replacing a 29% credit card, you are saving 14% every single month. That is a massive win for your wallet.

Myth #3: I should just file for bankruptcy.

Bankruptcy should be a last resort. It stays on your record for years and makes it nearly impossible to get a mortgage. Consolidation is a proactive move that shows future lenders you took responsibility and managed your way out of debt.

Why Choose LendingMoney.ca?

We aren’t just a website; we are your partners in this journey. We are affiliated with the Centum LM Group, meaning we have the backing of a major financial network but the heart of a local boutique.

We speak your language. No confusing jargon, no judgment – just a structured path to help you pay off high-interest debt and watch your credit score grow.

Final Thoughts: Your Future Starts Today

Debt is a heavy burden, but it doesn’t have to be permanent. By choosing a loan to consolidate debt with poor credit, you are taking the heroic step of protecting your family’s financial future.

Stop letting high interest dictate your life. Let us help you navigate the road back to a 700+ credit score.

Ready to start your journey? [Apply with Ease Today] and let’s get you back on track.

Read Blog – How to get a Second Mortgage With Bruised Credit