The short answer is yes. In fact, 2026 is one of the most accessible years for newcomers to enter the Canadian real estate market. While traditional banks often require a two-year “history” for standard loans, specialized Newcomer Mortgage Programs are designed to help you bypass that wait.

At LendingMoney.ca, we see many new Canadians who are “income-rich but credit-poor.” Here is how the 2026 rules allow you to move from a rental to your own home in as little as three months.

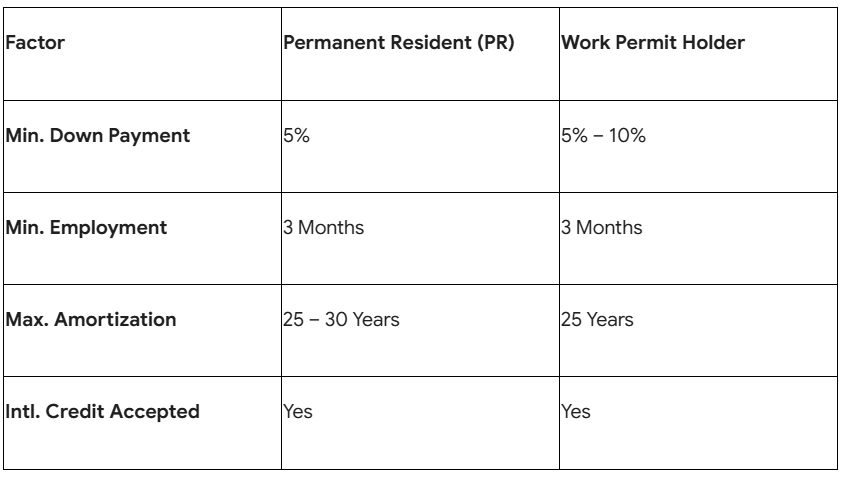

1. The 3-Month Employment Rule

Most newcomers think they need to wait years to prove their stability. In 2026, the standard for most newcomer programs is just 3 months of full-time employment in Canada.

- The Logic: Lenders want to see that you have passed your “probationary period” with a Canadian employer.

- The “Transfer” Bonus: If you were transferred to Canada by the same company you worked for abroad, some lenders may waive the 3-month wait entirely and approve you on Day 1.

2. Down Payment Requirements (5% vs. 35%)

Your down payment amount depends largely on your residency status and your credit profile.

- Permanent Residents (PR): You can qualify for a mortgage with as little as 5% down on the first $500,000 of the home’s value. These are “Insured Mortgages” (backed by CMHC, Sagen, or Canada Guaranty).

- Work Permit Holders: In 2026, many work permit holders can also qualify with 5% to 10% down, provided they have a valid permit and a stable Canadian income.

- The “No-Credit” Route: If you have zero Canadian credit and do not want to use an international report, you may be asked for a 35% down payment. This is a “non-insured” mortgage where your large equity stake offsets the lender’s risk.

3. Alternative Credit: Proving You’re a “Hero” Without a Score

If you haven’t built a 700+ credit score yet, 2026 lenders will look at Alternative Credit to prove your reliability. You will need to show 12 months of “payment consistency” through:

- Rent Receipts: A letter from your landlord and bank statements showing on-time rent.

- Utility Bills: Your Canadian phone, internet, or hydro bills.

- International Credit Reports: Using services like Nova Credit to pull your history from your home country.

4. The 2026 Foreign Buyer Ban Update

It is important to note that as of 2026, the Prohibition on the Purchase of Residential Property by Non-Canadians Act still has specific exemptions for newcomers.

- PR Status: You are exempt and can buy freely.

- Work Permit Holders: You are generally exempt if you have a valid permit and haven’t purchased more than one residential property.

- The 2026 Change: Regulations have been clarified to ensure that newcomers who are truly making Canada their home are not blocked by laws intended to stop offshore speculation.

5. First-Time Home Buyer Incentives in 2026

As a newcomer, you are almost always a “First-Time Buyer” in the eyes of the Canadian government. This unlocks:

- The FHSA (First Home Savings Account): You can contribute up to $8,000 per year ($40,000 lifetime) to this account. Contributions are tax-deductible, and withdrawals to buy a home are tax-free.

- Land Transfer Tax Rebates: In provinces like Ontario and cities like Toronto, you can save thousands of dollars on closing costs through first-time buyer rebates.

Newcomer Mortgage Fast-Facts (2026)

Why Start Your Journey with LendingMoney.ca?

Traditional banks have “Newcomer Packages,” but they also have very rigid boxes. If your situation is unique, perhaps you are self-employed in Canada or your down payment is coming from the sale of a property back home, the bank might say “wait.”

At LendingMoney.ca, we specialize in the “Path to Yes.” We work with alternative lenders who prioritize your future in Canada over your short history here.

Ready to find out how much home you can afford in 2026? [Get a Newcomer Mortgage Pre-Approval] with LendingMoney.ca today and let’s start your Canadian legacy.

Read blog – Welcome to Canada: Your 2026 Guide to Building Credit from Day 1