In the 2026 Canadian mortgage market, underwriters are no longer just looking at your 3-digit score; they are looking at your story. Thanks to new OSFI (Office of the Superintendent of Financial Institutions) guidelines, lenders are required to perform “enhanced due diligence” on any application with historical credit “bruising.”

If a lender asks you for a Letter of Explanation (LOX) regarding a late payment, a collection, or a past insolvency, don’t panic. This is actually a massive opportunity. It’s your chance to move beyond the cold math of the credit bureau and prove your “Hero” status.At LendingMoney.ca, we help our clients draft these letters every day. Here is the 2026 playbook for explaining a credit hit to a mortgage underwriter.

1. The Three Golden Rules of the LOX

Before you start typing, keep these three principles in mind:

- Be Honest: Underwriters have access to more data than ever before. If you try to hide a detail, they will find it, and your application will be declined for “misrepresentation.”

- Be Concise: An underwriter reviews dozens of files a day. They don’t want a 10-page novel; they want three paragraphs that explain the What, the Why, and the Resolution.

- Be Factual: Avoid emotional language. Don’t say, “It was a really hard time.” Instead, say, “Due to a medical leave between June and August 2024, my household income was reduced by 40%.”

2. The Structure of a Winning Explanation

A professional Letter of Explanation should follow this exact 3-part flow:

Part A: The Incident (What Happened?)

Identify the specific item on your credit report.

- Regarding the 30-day late payment on my RBC Credit Card in October 2024…

Part B: The Extenuating Circumstance (The Why)

Explain the specific, one-time event that caused the issue. Underwriters look for “isolated incidents” rather than “chronic habits.”

- “This occurred during a transition between employers where my final paycheck was delayed by three weeks.”

Part C: The Resolution (Why it Won’t Happen Again)

This is the most important part. You must prove that the situation has been fixed and your finances are now stable.

- The account was brought current immediately upon receipt of funds. Since then, I have established a 3-month emergency fund and set up automated minimum payments to ensure no future oversights.

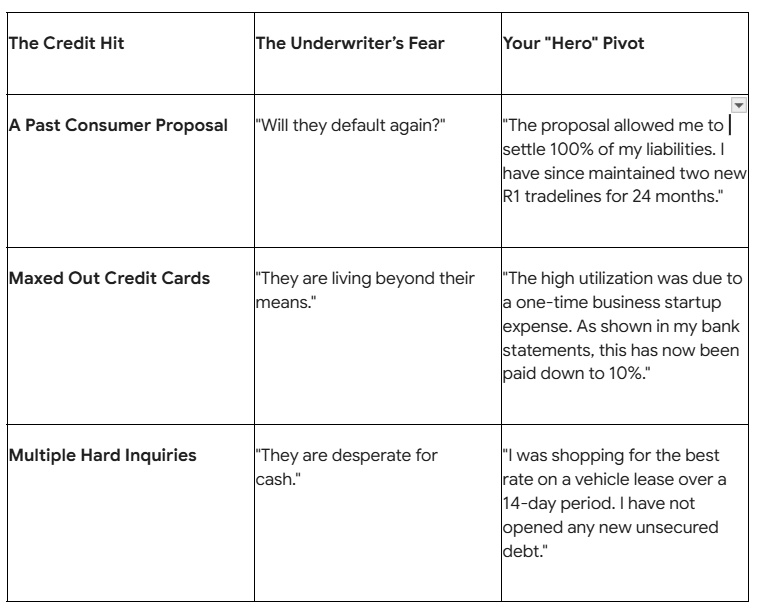

3. Common 2026 “Credit Hits” and How to Pivot Them

4. The Paper Trail (Supporting Documents)

In 2026, a letter isn’t enough – you need receipts. An underwriter is much more likely to accept your explanation if you attach:

- Medical Notes: If a health issue caused the credit hit.

- Termination/Hiring Letters: If it was due to a job gap.

- Release of Lien/Discharge Papers: If it was a legal or tax issue.

- Bank Statements: Showing the specific payment that cleared the debt.

5. Sample Template: The Late Payment Explanation

RE: Mortgage Application #12345 – Letter of Explanation for Credit Inquiry/Late Payment

To the Underwriting Department,

I am writing to provide context regarding the 60-day delinquency on my [Creditor Name] account in early 2025.

During this period, my family experienced a temporary financial strain due to [Reason: e.g., a localized flood not fully covered by insurance]. This was a one-time, unforeseen event.

Since that time, the account has been paid in full and maintained in good standing. My current employment at [Company] is stable, and I have maintained a 700+ score on all other tradelines. I have also implemented a [e.g., automated savings plan] to ensure total financial resilience moving forward.

Thank you for your consideration of my application.

Sincerely, [Your Name]

Why Your Story Matters at LendingMoney.ca

At LendingMoney.ca, we specialize in “Story-Based Underwriting.” We know that life happens—divorce, illness, and business pivots can all leave a mark on your credit report. But a mark isn’t a dead end.

We work with alternative lenders who prioritize the current person over the past score. We help you draft the explanations that turn a Maybe into an Approved.

Need help explaining your credit history to get a mortgage? [Connect with a Financial Hero] today and let’s tell your story the right way.

Read blog – How to Fix Your Credit After a CRA Debt Settlement