Settling a debt with the Canada Revenue Agency (CRA) is a massive relief, but it often leaves a “footprint” on your financial life. In 2026, the CRA does not report your tax balances to credit bureaus like Equifax or TransUnion, but the actions they take to collect that debt certainly do.

If you’ve recently paid off a CRA debt through a settlement, a refinance, or a Consumer Proposal, here is your 2026 roadmap to Credit Rehabilitation.

1. Verify the “Lien Release”

If your tax debt was severe enough that the CRA registered a Notice of Certification (Lien) against your property, paying the debt is only half the battle.

- The Reality: The CRA does not always automatically notify the Land Registry or the credit bureaus that the lien is gone.

- The Hero Move: Ensure your lawyer obtains a Cessation of Charge or a Discharge of Lien. You must send a copy of this document to both Equifax and TransUnion. Until you do, a lender looking at your “Public Records” section will still see an active tax lien, which is a major “Red Flag.”

2. Address “Indirect” Credit Damage

While the CRA itself doesn’t report late payments, the symptoms of tax debt usually hurt your score. If you were behind on taxes, you likely missed other payments or maxed out credit cards to keep up.

- The Audit: Now that the CRA is paid, go through your credit report. Are there “30-day lates” on your credit cards from the months you were struggling with tax debt?

- The Rehabilitation: You cannot delete accurate late payments, but you can “drown them out” with new positive data. Start a streak of 12 months of perfect payments on your remaining accounts. In the 2026 algorithm, recent behavior carries more weight than year-old mistakes.

3. Re-Establish “A-Lender” Tradelines

Many people use a Private Mortgage or a High-Interest Loan to settle their CRA debt. While effective, these “C-Lender” products don’t always help your score.

- The Move: To move back to a bank (A-Lender), you need at least two active tradelines with at least a $2,000 limit.

- The 2026 Strategy: If your cards were closed, open a Secured Credit Card and a Small Installment Loan. At LendingMoney.ca, we recommend using these for small, recurring utility bills to prove to the bank that your “Tax Crisis” was an isolated incident, not a lifestyle.

4. The “Income Stability” Story

In 2026, underwriters are looking for the “Why” behind your tax debt.

- The Narrative: If you settled a CRA debt, be prepared to explain it in your next mortgage application. Was it a one-time business error? A divorce?

- The Proof: Keep your Notice of Assessment (NOA) for the year the debt was settled. Showing a “$0 Balance Owing” on your most recent NOA is the single most important document for a newcomer or self-employed borrower to prove they are back in “Hero” status.

5. Avoid the “Refund Set-Off” Trap

Even after a settlement, the CRA may sometimes “offset” your future tax refunds or GST credits to cover old interest or penalties that weren’t fully cleared.

- The Risk: If you are counting on a tax refund to pay your credit card bill, and the CRA takes it, you could miss a payment and hurt your score again.

- The Hero Move: Check your CRA “My Account” portal one month after your settlement to ensure the balance is exactly $0.00. Don’t assume the file is closed until you see it in digital black and white.

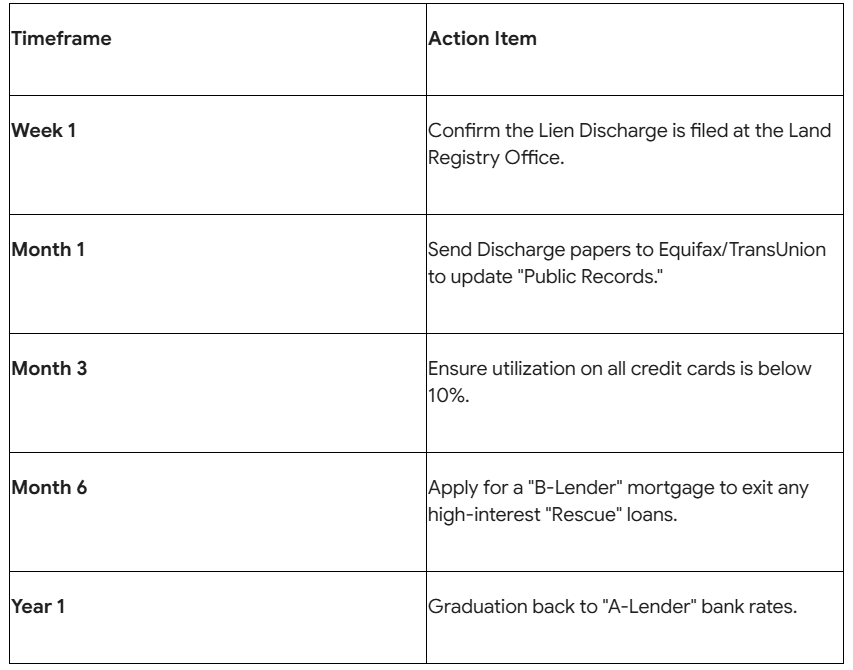

Credit Rehab Timeline After CRA Settlement

Your Fresh Start Starts Now

Paying the CRA is the hardest part. Now that the government is out of your bank account, you can finally focus on building your own wealth. At LendingMoney.ca, we don’t just help you pay the debt; we stay with you for the Credit Rehabilitation that follows.

Just finished a CRA settlement and want to know your next move? [Connect with a Financial Hero] at LendingMoney.ca. We’ll help you clean up the paperwork and get you back on the path to a prime-rate mortgage.