A divorce is more than a legal ending; it is a financial beginning. One of the most significant hurdles in this transition is securing a new home while your assets, income, and credit are in flux.

In 2026, the rules for “newly single” buyers in Canada have become more flexible, but the documentation requirements have become more strict. At LendingMoney.ca, we specialize in helping you navigate this “Bridge Phase” of your life. Here is how to move from a shared matrimonial home to a space that is truly yours.

1. The 90-Day Rule and the New Home Buyers’ Plan (HBP)

One of the best pieces of news for 2026 is that you no longer have to wait four years to be considered a “First-Time Home Buyer” again.

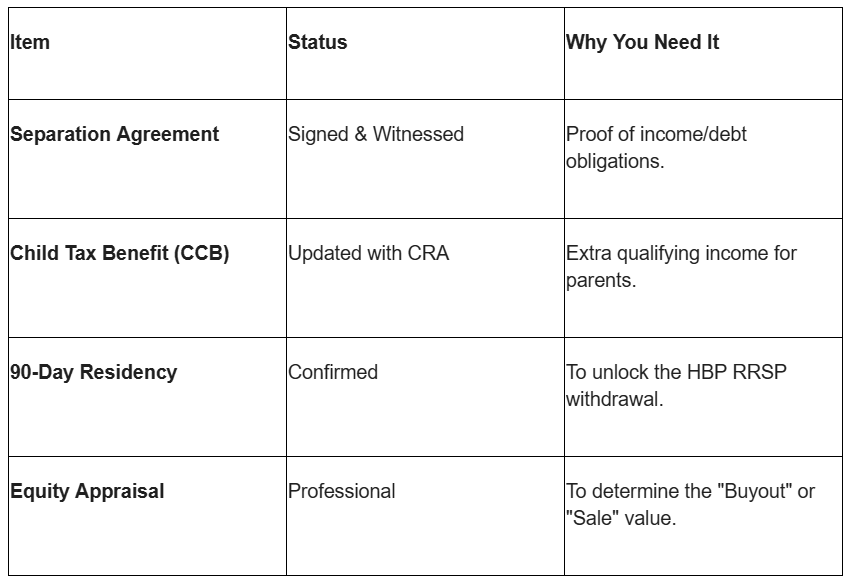

- The Rule: If you have lived “separate and apart” from your spouse for at least 90 days, you can qualify for the federal Home Buyers’ Plan (HBP) even if you previously owned a home together.

- The Benefit: You can withdraw up to $35,000 tax-free from your RRSP to use as a down payment on your new home.

- The Catch: You cannot be living in a home owned by a new spouse or common-law partner at the time of withdrawal.

2. The Power of the Spousal Buyout Program

If you want to stay in your current family home but need to pay out your ex-spouse’s share of the equity, you don’t necessarily need a 20% down payment.

- How it Works: Under special insured programs (CMHC, Sagen, Canada Guaranty), you can refinance your home up to 95% of its value to buy out your partner’s equity.

- Why this is a Hero Move: Usually, a refinance is capped at 80%. This special “Buyout Program” allows you to access the extra 15% of equity you need to settle the divorce and keep the roof over your head.

- Requirement: You must have a legally binding Separation Agreement that specifically outlines the buyout amount.

3. Support Payments: The Double-Edged Sword

In 2026, lenders view spousal and child support through a very specific lens. Depending on whether you are the payer or the receiver, it changes your borrowing power.

- If You RECEIVE Support: Most lenders will count support payments as qualifying income. To use it, you generally need to show a court order or signed separation agreement and 3–6 months of consistent bank deposits proving the money actually arrives.

- If You PAY Support: Lenders treat support payments as a fixed monthly debt (similar to a car payment). Because this is deducted from your income before your “Debt-Service Ratios” are calculated, it can significantly lower the maximum mortgage amount you qualify for.

4. Why the Separation Agreement is Non-Negotiable

You might have a “handshake deal” with your ex, but in 2026, a bank will not touch your application without a Legal Separation Agreement.

- What Lenders Look For: They need to see the final word on asset division, ongoing support obligations, and any “Joint Debts” you are still responsible for.

- The “Zombie Debt” Risk: If your name is still on your ex-partner’s car loan or credit card, the bank counts that full payment against you. Your agreement must clearly state who is responsible for which debt so the lender can “exclude” those items from your ratios.

5. Rebuilding Your Solo Credit Score

Often, divorce involves late payments on joint accounts during the “messy” months of separation. This can tank your credit score right when you need it most.

- The Audit: Check your credit report for any “Joint Accounts” that your ex may have neglected.

- The Rehabilitation: If your score has dropped below 680, you may not qualify for the best bank rates. At LendingMoney.ca, we offer Alternative “Bridge” Mortgages. These allow you to buy your new home now, and we work with you over the next 12–24 months to rebuild your score so you can “graduate” to a lower-rate bank mortgage once the divorce is finalized.

The Post-Divorce Mortgage Checklist (2026)

You Don’t Have to Do This Alone

Navigating a mortgage during a divorce is emotionally draining and technically complex. At LendingMoney.ca, we see the person behind the paperwork. Whether you are buying out a partner or starting fresh in a new neighborhood, we have the alternative lending tools to make it happen.

Starting your next chapter? [Get a Confidential Divorce Mortgage Assessment] from LendingMoney.ca today. We’ll help you find the equity and the path to your new front door.