When you take out a private mortgage, you aren’t just signing a loan; you are entering a high-stakes business partnership. In the 2026 lending environment, private mortgages (often called “C-Lending”) are more common than ever, but they are also more complex.

At LendingMoney.ca, we believe that a “Financial Hero” is an informed borrower. Before you sign that commitment letter, you need to look past the interest rate and ask these five critical questions. The answers will determine whether your mortgage is a helpful bridge or a permanent trap.

1. What is the Total ‘Cost of Borrowing’ (APR)?

The interest rate is only one part of the story. Private lenders often layer on multiple fees that aren’t immediately obvious.

- The Reality: You might see a rate of 9.99%, but once you add the Lender Fee (2%), the Broker Fee (2%), and the Legal Fees ($3,000), your actual Annual Percentage Rate (APR) could be closer to 15%.

- The Hero Move: Ask for a full disclosure of all one-time and recurring fees. If the lender is hesitant to give you a “Truth in Lending” summary, that’s a red flag.

2. Is There a ‘Renewal Fee’ After 12 Months?

Most private mortgages in Ontario are one-year terms. The biggest “Equity Killer” is the surprise fee that hits you when that year is up.

- The Trap: Some private lenders charge the same 2% fee to renew the loan for another year. If you have a $500,000 mortgage, you are paying $10,000 just to stay in the loan.

- The Hero Move: Ask if the renewal fee can be waived or capped if you make all your payments on time.

3. What are the Pre-Payment Penalties?

A private mortgage is meant to be a short-term fix. You want the freedom to leave as soon as your credit score improves or you sell your home.

- The Reality: Many private lenders “lock” you in for the full term. If you try to pay off the mortgage at month 6, they may charge you the remaining 6 months of interest as a penalty.

- The Hero Move: Look for a “3-month interest” penalty or, better yet, a “Fully Open” mortgage. This allows you to “graduate” to a bank-rate mortgage the moment your Credit Rehabilitation is complete without paying a fortune to leave.

4. Is This an ‘Interest-Only’ or ‘Amortized’ Loan?

Most private mortgages are “Interest-Only,” meaning your monthly payment doesn’t reduce the amount you owe.

- The Risk: If you borrow $400,000, you will still owe exactly $400,000 a year from now. If the housing market dips, you could end up owing more than the house is worth.

- The Hero Move: Confirm exactly where your money is going. If it’s interest-only, you must have a separate plan to save for a principal reduction or a plan to refinance into an amortized “B-Lender” loan as soon as possible.

5. What Happens if I Miss a Single Payment?

Private lenders don’t have the same “Loss Mitigation” departments as big banks. Their tolerance for late payments is much lower.

- The Trap: Some contracts include “Default Interest Rates” that can jump to 24% or higher the moment a payment is missed. They may also initiate Power of Sale proceedings after just 15 days of default.

- The Hero Move: Ask about the “Grace Period” and the “NSF Fees.” You need to know exactly how much time you have to fix a mistake before legal action begins.

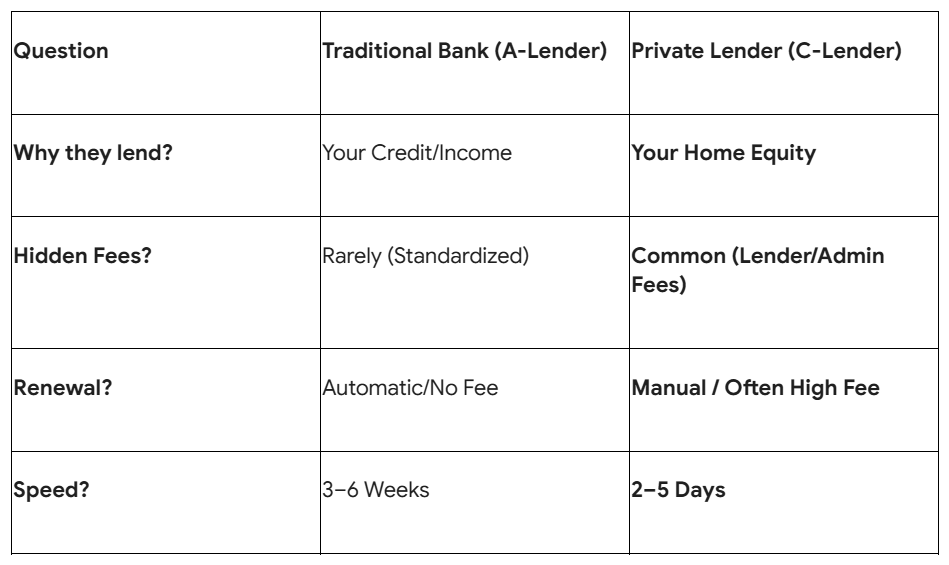

Comparison: Standard Bank vs. Private Lender Questions

Don’t Sign Until You’re Certain

At LendingMoney.ca, we act as your protective shield. We vet every private lender in our network to ensure their terms are fair and their “Exit Strategy” is clear. We don’t just want you to get the money; we want you to keep your equity.

Considering a private mortgage offer? [Upload Your Commitment Letter] for a “Second Opinion” from a Financial Hero at LendingMoney.ca. We’ll help you spot the traps before you sign.