Moving to a new country is a monumental achievement. You’ve navigated the immigration process, secured a place to live, and perhaps started a new career. However, many newcomers face a frustrating catch-22: you need credit to rent an apartment, get a phone plan, or buy a car, but you can’t get credit because you have no Canadian history.

In 2026, the Big Six banks and alternative lenders like LendingMoney.ca have new tools to help you bridge this gap. Here is your roadmap to building a Financial Hero profile in your first 12 months.

1. The 2026 Reality: Your Foreign History Matters (Finally)

For decades, your credit history stayed behind in your home country. In 2026, that has changed thanks to cross-border data partnerships.

- The Bridge Program: Companies like Nova Credit now partner with Canadian lenders to pull your credit history from countries like India, the UK, Brazil, the Philippines, and more.

- The Hero Move: Before you apply for a standard Newcomer Package, ask if the lender can use an international credit report. This could allow you to skip the secured card phase and go straight to a high-limit unsecured card.

2. Step One: The Newcomer Banking Package

Every major Canadian bank (RBC, TD, Scotiabank, etc.) offers a specific “Start Right” or Newcomer bundle.

- What’s included: Usually a chequing account with no fees for a year and a specifically designated newcomer credit card.

- The 2026 Advantage: Many of these cards now offer limits up to $5,000 to $15,000 without a Canadian credit score, provided you show proof of your Permanent Residency (PR) or a valid Work Permit.

3. The Cell Phone Credit Hack

In 2026, your phone bill is one of your most powerful credit-building tools.

- The Strategy: Avoid “Pre-paid” plans. While they are easy to get, they don’t report to the credit bureaus.

- The Move: Opt for a “Post-paid” monthly plan with a provider like Rogers, Bell, or Telus. These providers report your on-time payments to Equifax, helping you build a “tradeline” before you even have your first credit card statement.

4. Rent Reporting: Making Your Biggest Expense Count

Historically, paying rent did nothing for your credit score. In 2026, Rent Reporting has become a standard feature for savvy newcomers.

- How it works: Services like Chexy or Landlord Credit Bureau allow you to report your monthly rent payments to Equifax and TransUnion.

- The Benefit: Since rent is likely your largest monthly payment, showing 12 months of on-time rent can boost a newcomer’s score by 40 – 70 points faster than a credit card alone.

5. Beware of the Hidden Credit Checks

As a newcomer, you are often applying for many things at once: an apartment, a car, a phone, and electricity.

- The Risk: Each Hard Inquiry can drop your score slightly. Too many in your first month can make you look “credit hungry.”

- The 2026 Strategy: Use Digital ID (like the new GC Sign-In or provincial digital wallets) where possible. Many landlords and utility providers in 2026 now accept “Digital Identity Verification” which uses a Soft Inquiry that doesn’t hurt your score.

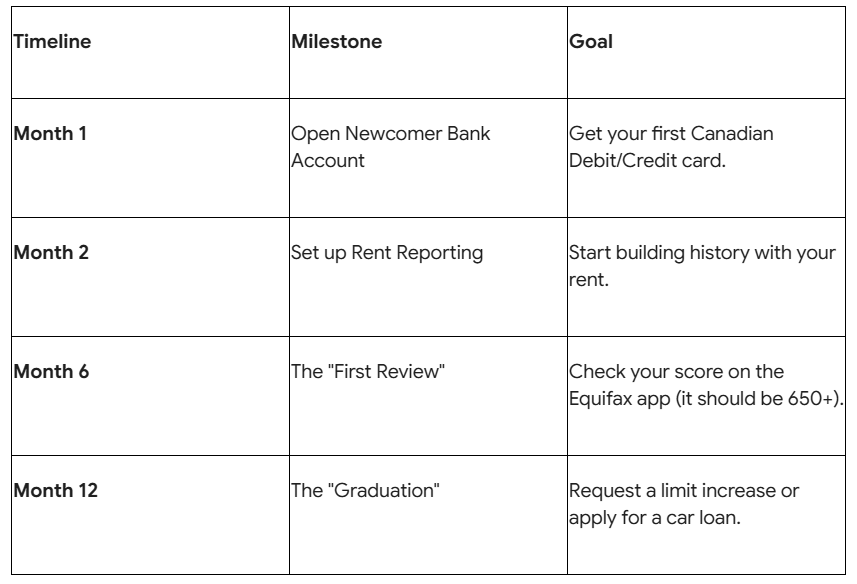

Your First 12 Months: The Credit Milestone Map

Why LendingMoney.ca Loves Newcomers

At LendingMoney.ca, we don’t think No History means No Potential. We work with alternative lenders who look at your Global Professional Standing and your Canadian Income rather than just a 3-digit number.

If you’re a newcomer with a high-paying job but the bank says you need to wait two years for a mortgage, we have the Alternative solutions to get you into a home sooner.

Just landed in Canada and ready to build your future? [Connect with a Financial Hero] at LendingMoney.ca. We’ll help you navigate the system and fast-track your credit journey.