If you have received a Notice of Sale Under Mortgage, the most important thing to know is that you still own your home. In Ontario, the “Power of Sale” is a legal process, and like any process, it can be stopped, but the clock is ticking.

In 2026, lenders are moving faster to protect their capital, often initiating the process after just two missed payments. Here are the top five ways to pull the emergency brake and stop a Power of Sale today.

1. Pay the Arrears and Reinstate (The Cleanest Break)

The most direct way to stop a Power of Sale is to “cure” the default. Under Section 22 of the Mortgages Act, you have the right to bring the mortgage back into good standing by paying exactly what is owed.

- What you pay: You must pay the total of all missed payments, any late penalties, and the lender’s actual legal costs incurred to date.

- The Result: Once paid, the Power of Sale is legally voided, and your mortgage continues as if the default never happened.

- Hero Tip: If you’ve recently returned to work or received an inheritance, this is your best move. Always get a written “Statement of Arrears” from the lender’s lawyer to ensure you are paying the correct amount.

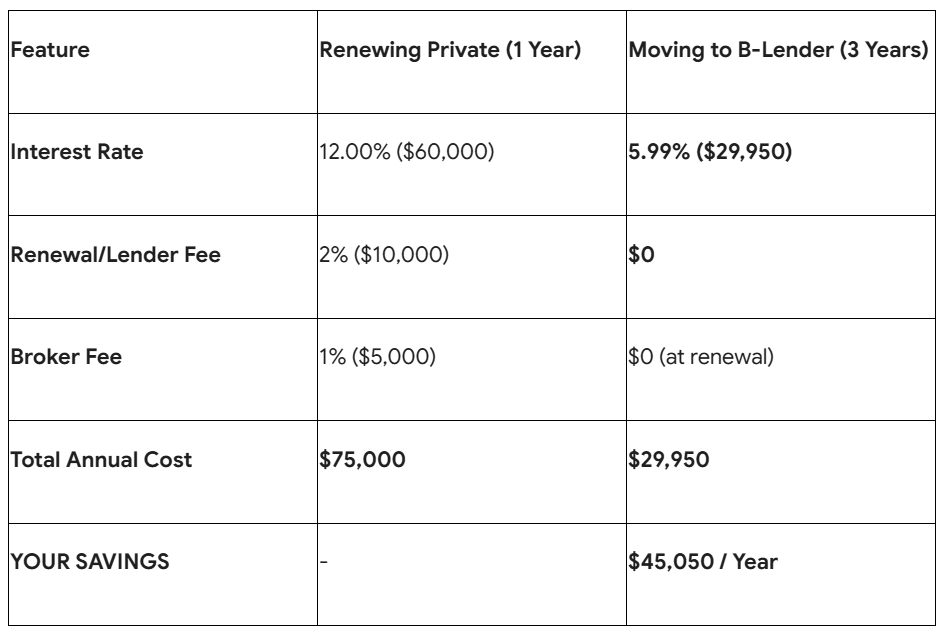

2. Refinance with an Alternative or Private Lender

If you cannot come up with the cash to pay the arrears, you can replace the entire mortgage. Traditional banks will not touch a file in Power of Sale, but Alternative Lenders (like LendingMoney.ca) specialize in this.

- How it works: A new lender pays off your old bank in full (including all legal fees and penalties). The Power of Sale is cancelled because the debt no longer exists.

- The 2026 Strategy: This is a “Bridge” strategy. You take a 1-year term with an alternative lender to save your home today, then use that year for Credit Rehabilitation so you can switch back to a lower-rate bank later.

3. Sell the Property Privately (Protect Your Equity)

If you know you cannot afford the mortgage long-term, you should sell the home yourself before the lender does.

- The Math: When a lender sells your house under Power of Sale, they often sell it “as-is” and may not push for the highest price, they just want their money back. By listing it yourself, you control the marketing and the price.

- The Legal Window: You can list and sell your home even after a Notice of Sale is issued, provided the sale closes before the lender completes their own transaction. This ensures that the surplus equity (the profit) stays in your pocket, not the bank’s legal fees.

4. Negotiate a Forbearance or Repayment Plan

Believe it or not, most lenders do not actually want your house; they want their money. In 2026, many institutions have “loss mitigation” departments.

- The Ask: Request a formal Forbearance Agreement. This is a legal document where the lender agrees to “pause” the Power of Sale if you agree to a strict schedule to pay back the arrears over 3–6 months.

- The Hero Move: You are more likely to get a “Yes” if you can pay a small “good faith” lump sum immediately.

5. Challenge the Process (The Legal Defense)

If the lender has made a mistake in the paperwork, a judge can stay (stop) the Power of Sale.

- Common Errors: Failing to wait the mandatory 15-day default period before sending the notice, or failing to serve the notice to all registered owners (including ex-spouses).

The Catch: This requires a specialized real estate lawyer and can be expensive. It is usually a “delay tactic” to buy you more time to execute Option 2 or Option 3.

Comparison of Your “Rescue” Options

The 35-Day Redemption Clock

In Ontario, once you receive the Notice of Sale Under Mortgage, you have a 35-day redemption period (40 days if it’s a matrimonial home). During this window, the lender cannot sell the property. This is your “Golden Window” to act. Once this period expires, the lender can list the property on the MLS, and your options become much more expensive.

Warning: Do not wait until Day 34. Appraisals and alternative mortgage funding take time.

Is the clock ticking on your Notice of Sale? [Connect with a Financial Hero] at LendingMoney.ca immediately. We can often secure an equity-based approval in 24 hours to stop the sale and save your home.

Read blog – What is a Power of Sale in Ontario? Your 2026 Emergency Guide