Life in 2026 is expensive. Between groceries, utilities, and the new reality of higher mortgage rates, it only takes one unexpected event, a job transition, a medical emergency, or a major home repair, to fall behind on your mortgage.

If you’ve missed a payment, you might be avoiding your bank’s calls out of fear. But in Canada, lenders actually prefer helping you catch up over the long, expensive process of a “Power of Sale.” Here is your step-by-step Credit Rehabilitation plan to get back on track.

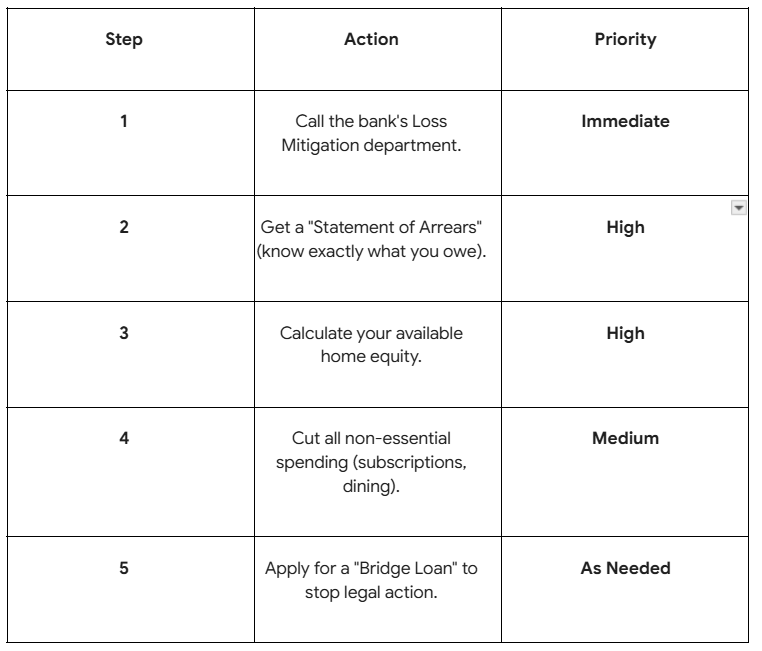

1. The First Strike Rule: Call Your Lender

The moment you know a payment is going to bounce, or if you’ve already missed one, pick up the phone.

- What to Ask For: Ask to speak to the Loss Mitigation Department.

- The 2026 Options: Most “Big Six” banks and credit unions have structured relief programs, including:

- Capitalizing the Arrears: The lender takes the missed payments and adds them back into your total mortgage balance, spreading the cost over the remaining years.

- Payment Deferral: Some lenders may allow a “pause” for up to 4 months if you can prove the hardship is temporary.

Interest-Only Payments: A temporary shift where you only pay the interest, giving you a 3–6 month window to stabilize your income.

2. Leverage Your Hero Tool: Home Equity

If your bank isn’t willing to work with you, or if you owe more than three months of payments, the “institutional” door may close. This is where your home’s value becomes your lifesaver.

- The Equity Bailout: If you have at least 20% equity in your home, you can use a Second Mortgage or an Alternative Equity Loan from LendingMoney.ca to “clear the slate.”

- Why this works: We provide the lump sum needed to pay the bank the full amount of your arrears (including their legal fees). This stops the foreclosure process instantly. You then have a manageable monthly payment with us while you get back on your feet.

3. The Amortization Stretch

If the reason you fell behind is that your monthly payment is simply too high for your current income, a “catch-up” payment is only a temporary fix. You need a structural change.

- The Move: Re-amortize your mortgage. If you have 15 years left, ask to move back to a 25 or 30-year schedule.

- The Result: This lowers your monthly obligation, making it much harder to fall behind again in the future.

4. Watch Out for the Legal Fee Trap

In 2026, once a mortgage goes into “Default,” lenders move quickly.

- The Danger: After 2 or 3 missed payments, the bank’s lawyer will issue a “Statement of Claim.” The moment this happens, thousands of dollars in legal fees are added to your debt.

- The Strategy: The faster you act, the less you pay. Settling your arrears in month two might cost you $200 in fees; waiting until month four could cost you $5,000.

5. The CRA Connection

Check your tax status. In 2026, many mortgage arrears are actually caused by the CRA freezing a homeowner’s bank account due to unpaid taxes.

- The Fix: If your mortgage is bouncing because your accounts are frozen, you must resolve the CRA issue simultaneously. Using home equity to pay off both the CRA and the mortgage arrears is the ultimate “Double-Hero” move.

Your “Catch-Up” Checklist (2026)

You Don’t Have to Lose Your Home

At LendingMoney.ca, we specialize in the “Second Chance.” We know that being behind on your mortgage is a heavy burden, but we have the alternative lending tools to lift it. We help you pay the arrears, stop the legal fees, and build a plan to return to a traditional lender when your Credit Rehabilitation is complete.

Are the calls from the bank getting louder? [Get an Arrears Rescue Quote] from LendingMoney.ca today. Let’s protect your equity and keep your family in their home.