If your phone is vibrating multiple times a day with incoming calls from blocked numbers or strange area codes, you are living under a state of financial siege. The constant pressure of knowing a debt collector is on the other line creates a level of ambient stress that impacts your sleep, your work, and your relationships.

As we hit the mid-point of 2026, household debt across Canada has broken historical records. More consumers find themselves facing collection agencies than at any point since 2009.

If you are looking for a way out, you have likely tried downloading call-blocking apps, ignoring unknown numbers, or putting your phone on “Do Not Disturb.” But these are temporary bandages. To stop collection calls permanently, you have to understand your legal rights under Canadian law and execute a strategic financial exit.

Here is the exact playbook on how to silence the collection agencies and reclaim your peace of mind.

Step 1: Use the Law to Force an Intermission

Many collection agencies count on you not knowing provincial consumer protection laws. In Canada, debt collectors are bound by strict operating rules. If they violate these rules, you can file a formal complaint with your provincial consumer protection ministry, which can result in heavy fines for the agency.

By auditing their behavior against the law, you can immediately push back:

- The 3-in-7 Rule: In provinces like Ontario, a collection agency is legally permitted a maximum of 3 successful contacts within a 7-day period per debt. A contact means speaking to you, leaving a voicemail, or sending an email. If they are blowing up your phone 10 times a day, they are breaking the law.

- The Holiday Ban: Collectors are strictly forbidden from calling you on statutory holidays, Sundays before 1:00 PM or after 5:00 PM, and any other day before 7:00 AM or after 9:00 PM.

- The Workplace Limit: A collector can only call your employer once to confirm your employment status. They cannot call repeatedly, and they are legally forbidden from discussing your debt with your boss or co-workers.

The Legal Shift: You have the legal right to demand that the agency communicate with you only in writing. You can send a registered letter or an email stating: “I dispute this debt / require all future communications to be in writing only to my email/mailing address.” Once received, they are legally required to stop calling your voice lines.

Step 2: Understand the Danger of Ghosting

While forcing the communication to writing stops the phone from ringing, it does not solve the root problem. Completely ignoring an active collection file is a dangerous gamble.

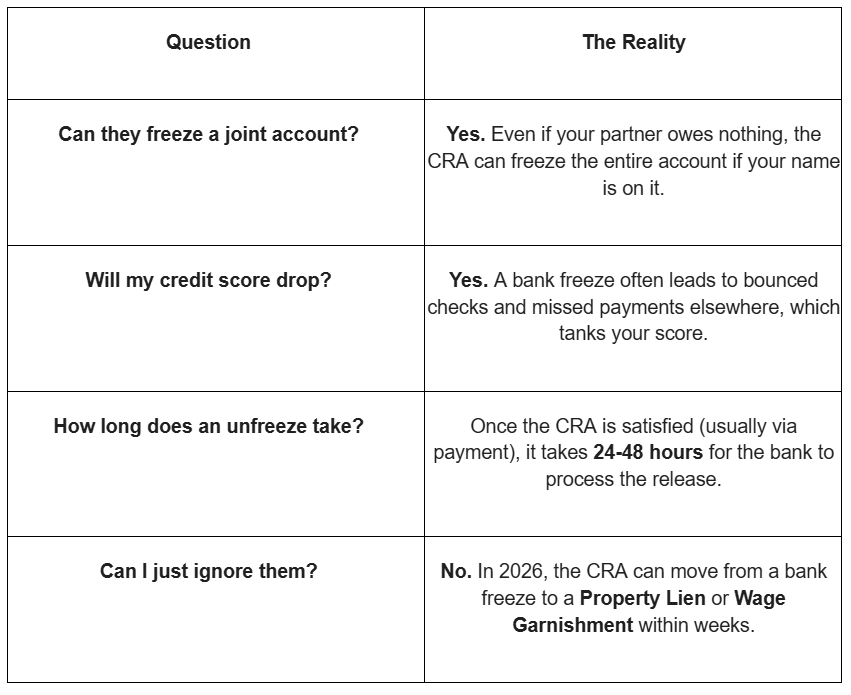

If a collection agency realizes they cannot reach you by phone, they will pass your file to their legal department. Under provincial statutes of limitations (which is two years from default in Ontario, BC, and Alberta), an agency can sue you in court. If you ignore the court documents, they win an automatic default judgment.

A default judgment hands the collection agency massive legal powers, including the right to garnish your paycheque, freeze your bank accounts, or register a lien directly against your home’s property title.

Step 3: The Permanent Solution (The Direct Payout Intercept)

To stop the calls forever without risking a legal escalation, you must satisfy the debt. But if you try to negotiate a settlement on your own, collectors will often try to trick you into a high-interest, long-term monthly payment plan that keeps your credit score trapped in a downward spiral.

This is where LendingMoney.ca steps in to act as your financial shield. If you have stable current income or equity locked inside your home, we provide the alternative capital you need through structured unsecured personal loans (up to $15,000) or short-term 2nd mortgages.

We don’t just hand you a lump sum of cash; we step between you and the collection agency, managing the payout directly.

The LendingMoney.ca Direct Payout System

- The Immediate Cease-and-Desist: The moment you are pre-approved, our underwriting specialists contact the collection agency. We notify them that an institutional lender is handling the file. Legally, they must stop contacting you and route all communication through us. Your phone goes silent instantly.

- The Written Discount Lockdown: We deal with the collection agency institution-to-institution. We negotiate a “Full and Final Settlement,” frequently slashing the total balance by 40% to 60%. We force the agency to issue an official Settlement Release Letter in writing before any money moves.

- The Secure Payout: We disburse the settlement funds directly to the agency from your loan proceeds, securing an indisputable bank-to-bank electronic paper trail proving the liability is dead.

- The Credit Score Reset: We ensure the collection agency updates Equifax and TransUnion promptly, changing your status permanently to “Paid Collection” or “Settled.” This stops the active damage to your report and begins your timeline to graduate back to traditional bank rates.

Take Back Your Phone, Take Back Your Life

You do not have to spend the rest of 2026 living in fear of your phone lighting up. Hiding from unknown numbers is exhausting, but taking a proactive stand with an alternative, structured settlement puts you back in the driver’s seat.

Let LendingMoney.ca handle the collectors, secure the written discounts, and execute the direct payouts so you can finally leave your phone face-up on the table.

[Request a Confidential Collection Settlement Analysis]

100% secure online application. No obligation and absolutely no hard credit inquiry to view your options. Let us make the phone stop ringing today.