When you’re a few days away from your next paycheck and an unexpected expense hits—a car repair, a dental bill, or a late utility notice – the “Instant Cash” sign at a payday lender can look like a lifesaver. It’s fast, there’s no credit check, and the fee seems small: “Just $14 per $100 borrowed.”

But in the world of Canadian finance, that $14 is a wolf in sheep’s clothing. At LendingMoney.ca, we specialize in Credit Rehabilitation, and the first step in that journey is stopping the “payday cycle.” Here is the reality of what those loans actually cost you and why they are the most expensive way to borrow money in 2026.

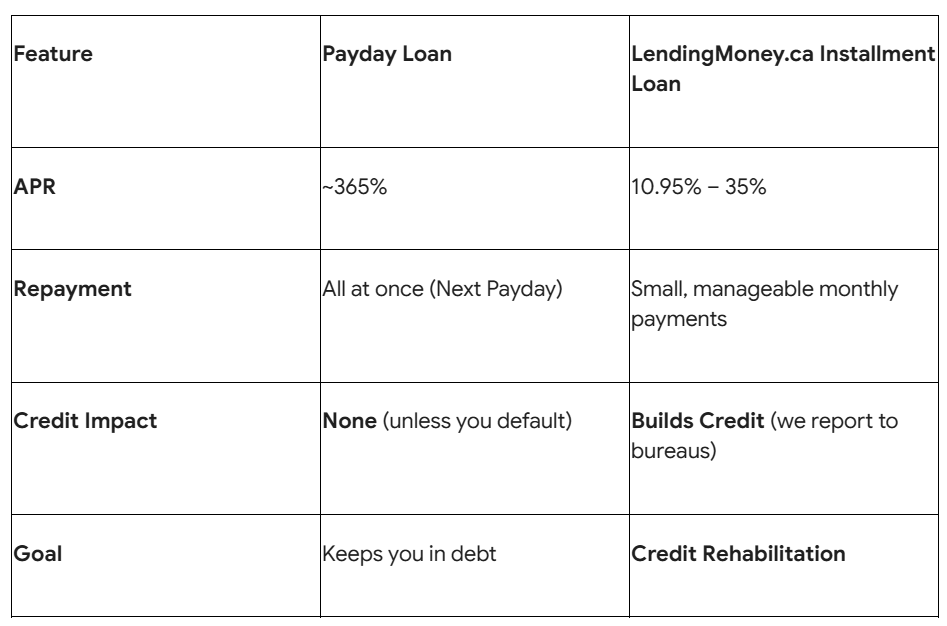

1. The APR Shock: 365% vs. 10.95%

Payday lenders often talk in “fees” rather than “interest rates” to hide the true cost of the loan. Under 2026 Canadian regulations, the maximum a lender can charge in most provinces is $14 for every $100 borrowed for a 14-day term.

While $14 sounds manageable, let’s look at the Annual Percentage Rate (APR):

- A typical credit card has an APR of 19.99%.

- A personal installment loan from a lender like LendingMoney.ca might range from 10.95% to 35%.

- A payday loan has an APR of 365%.

If you borrowed that same $100 for a full year at payday rates, you wouldn’t owe $114 – you would owe hundreds in compounding fees. You are essentially paying “VIP prices” for a “budget” service.

2. The “Invisible” Fees: NSFs and Bounced Cheques

The $14 fee is only the beginning. The real “hidden” costs kick in if anything goes wrong:

- The Bank Hit: If the payday lender tries to withdraw the repayment and you don’t have the funds, your bank will charge you an NSF (Non-Sufficient Funds) fee, which in 2026 averages $45 to $50.

- The Lender Hit: On top of your bank’s fee, the payday lender can charge a “Dishonoured Payment” fee (capped at $20 in most provinces).

- The Result: A simple $300 loan can suddenly cost you an extra $70 in fees in a single day – all before you’ve even touched the principal.

3. The Silent Credit Killer

One of the biggest myths is that paying back a payday loan helps your credit score. It does not.

- No Upside: Most payday lenders do not report your on-time payments to Equifax or TransUnion. You can pay back 50 loans perfectly and your credit score won’t move an inch.

- Massive Downside: If you miss a payment, they will sell your debt to a collection agency. That agency does report to the bureaus, resulting in an R9 rating (the same as bankruptcy) that can haunt your report for six years.

4. The Debt Spiral (The Rollover Trap)

The most devastating hidden cost of a payday loan is the loss of your future income. Because the loan is due in full on your next payday, many borrowers find themselves short on cash for rent or groceries the very next day.

This leads to the “Cycle of Debt”:

- You take a loan to pay a bill.

- Your next paycheck goes entirely to the lender.

- You immediately take another loan to survive the month.

- You are now paying a “subscription fee” of $14 per $100 just to access your own salary.

[Image: The Payday Cycle – A hamster wheel of debt]

5. New 2026 Protections: What You Need to Know

As of 2025 and 2026, the Canadian government has significantly tightened the rules to protect you:

- Criminal Interest Rate: The federal criminal interest rate has been lowered to 35% APR for most personal loans. While payday loans have a specific exemption, the “net” is closing in on predatory lenders.

- Cooling-Off Periods: In provinces like Ontario and BC, you have two business days to cancel a payday loan contract without any penalty. If you realize you’ve made a mistake, you can give the money back and walk away for free.

The Hero Alternative: The Installment Loan

At LendingMoney.ca, we offer a different path. Instead of a 14-day “trap,” we provide Installment Loans with terms from 9 to 60 months.

Final Thoughts: Stop Feeding the Machine

Payday loans are designed to be easy to get into and impossible to get out of. If you are caught in the cycle, the best “Hero Move” you can make is to consolidate those high-interest “fires” into one structured, lower-interest loan that actually helps your credit score.

Are you ready to break the cycle? [Apply for an Installment Loan] today and let’s get you on the path to true financial freedom.

Read Blog –Breaking the Cycle: A Guide to Loans for Debt Consolidation with Poor Credit