When you fall behind on credit card payments, the bank sends letters. When you fall behind on your taxes, the CRA moves in.

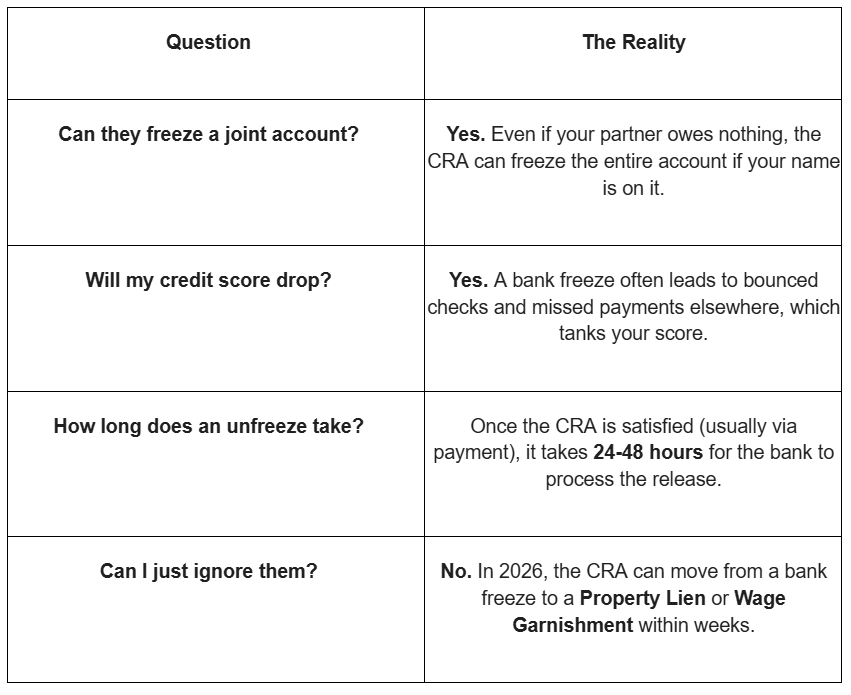

Unlike standard lenders, the Canada Revenue Agency (CRA) does not need a court order to take aggressive action against you. They can freeze your bank accounts, garnish your wages, and even register a tax lien against your home. If you’re juggling credit card debt and tax arrears, you aren’t just facing a financial headache-you’re facing a crisis.

At LendingMoney.ca, we specialize in using your home equity to stop the CRA collection cycle before it escalates, allowing you to settle your arrears and clear your high-interest debt simultaneously.

Why Tax Arrears Are Different (And Dangerous)

Most people prioritize their credit cards because they worry about their credit score. This is a mistake. While a late credit card payment hurts your score, an unpaid CRA balance can threaten your lifestyle and your property.

- Compound Interest: The CRA charges daily compound interest on overdue balances. As of mid-2026, this rate sits at 7%, but it can climb, and it is calculated on top of penalties for late filing.

- The Power of the Lien: If the CRA registers a lien on your home, your ability to sell or refinance becomes severely limited. You effectively lose control over your property until that debt is cleared.

- Asset Seizure: The CRA is one of the few creditors that can “offset” your tax refunds, freeze your operating accounts, or even work with your employer to deduct money directly from your paycheque.

The Debt Sweep Strategy: A Two-Fold Solution

When you come to us for debt consolidation, we look at your “Total Debt Picture.” If you have credit cards and tax debt, we structure a 2nd Mortgage that kills both birds with one stone.

How it Works:

- The Priority Payout: We use the funds from your 2nd mortgage to pay the CRA arrears first. This removes the threat of liens, garnishment, and bank freezes. It gives you “breathing room” to get your tax filings current.

- The Credit Card Cleanup: We then pay off your high-interest credit card debt. You move from paying 22%+ interest to a single, structured mortgage payment.

- The Fresh Start: With your taxes paid and your credit cards at $0, your cash flow is restored. You stop paying the CRA’s compounding interest, and you start using your monthly income for your life, not for damage control.

The Critical Timing Factor

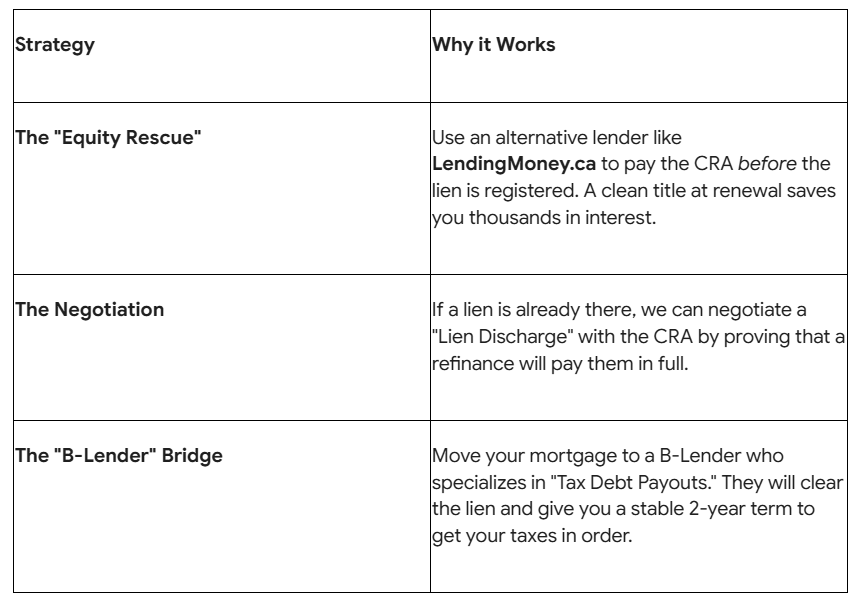

The most important thing to know about CRA debt is this: You must act before the lien is registered.

Once a tax lien is on your property, the legal and administrative costs to refinance your home skyrocket. If you are starting to see “Notice of Assessment” letters that you can’t pay, do not wait for the “Final Notice” or “Requirement to Pay” letters.

Does your current situation look like this?

- You are self-employed and had a tough tax year?

- You have unfiled returns that are preventing you from getting bank financing?

- Your credit score is suffering because you’ve had to use credit cards to keep up with your tax installments?

If so, you are a prime candidate for an Equity-Based Debt Sweep.

Why LendingMoney.ca?

Traditional banks will rarely touch a file where taxes are owing. They view it as a high-risk situation and will simply deny your application, leaving you to deal with the CRA alone.

We understand that entrepreneurs and families have ups and downs. We look at your Equity Position, not just your tax clearance letter. We can provide the bridge financing you need to settle your CRA debt, giving you the time and stability to get your records back in order.

Don’t let the CRA dictate your financial future. Let us help you settle your arrears and get back to zero.

[Request Your Confidential Debt Sweep Analysis]

It only takes two minutes. No obligation, no hard credit pull, and complete confidentiality.

Read Blog – Second Mortgages Explained: The Strategy Behind the Loan