We’ve all been there: an unexpected car repair, a dental emergency, or a utility bill that’s higher than usual. When you need cash today and the bank has already said no, a neon sign for a payday loan can look like a beacon of hope.

In Ontario, names like Money Mart are everywhere, promising “instant cash” with “no credit check.” But in 2026, the price of that speed has reached a breaking point for many Canadian families. At LendingMoney.ca, we believe that true Credit Rehabilitation starts with understanding why payday loans are designed to keep you in debt-and how alternative lending can set you free.

1. The 365% Reality Check

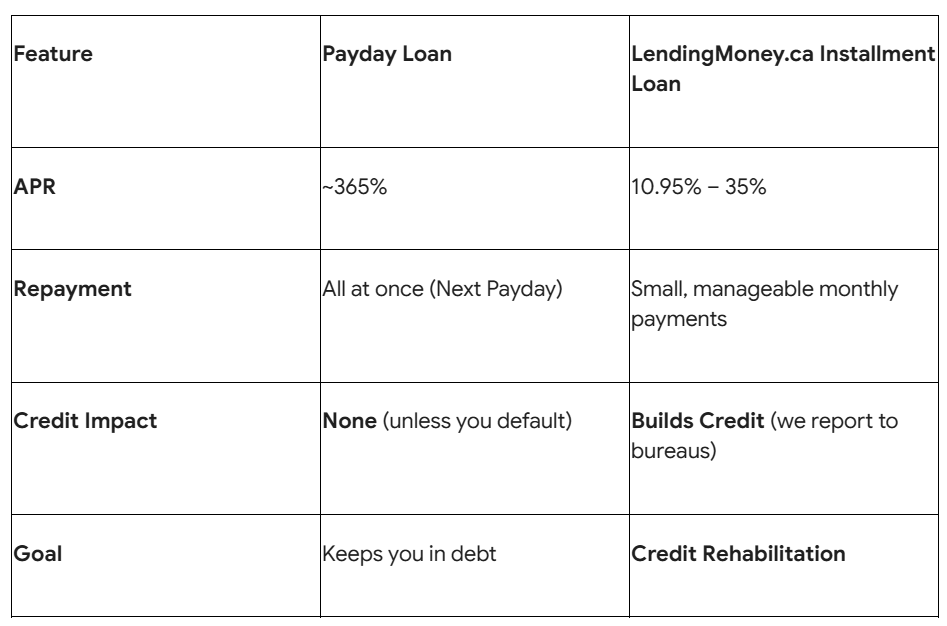

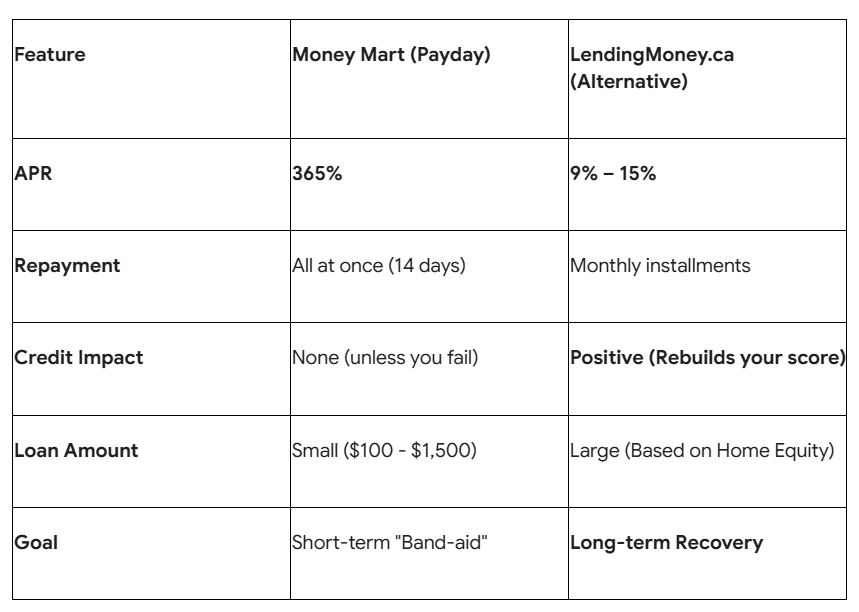

In Ontario, the law limits payday lenders to charging $14 per $100 borrowed. On the surface, $14 doesn’t sound like much. But payday loans are designed to be paid back in just 14 days.

- The Math: If you borrow $500 for two weeks, you pay $70 in fees. If you were to carry that same debt for a full year, the Annual Percentage Rate (APR) is a staggering 365%.

- The Comparison: At LendingMoney.ca, an alternative equity loan or second mortgage typically carries an APR between 9% and 15%. That is a difference of over 350%.

2. The Vicious Cycle of Re-Borrowing

The biggest pitfall of a payday loan isn’t the first one—it’s the second one.

- The Trap: When your next paycheck arrives, the payday lender takes their $570 (principal + fees) directly from your account. This leaves you with $570 less to pay your rent and buy groceries for the next two weeks.

- The Result: Most borrowers find themselves short again within days, forcing them to take out a new payday loan to cover the gap left by the first one.

- The 2026 Data: Statistics Canada reports that the average payday loan user in 2026 takes out 8 to 10 loans per year. This isn’t a “bridge”-it’s a treadmill.

3. The No Credit Check Illusion

Payday lenders often advertise “No Credit Check” as a benefit. While this makes it easy to get the money, it has a hidden sting: Payday loans almost never help your credit score.

- The Logic: Because they don’t report your on-time payments to Equifax or TransUnion, you get zero “points” for paying them back.

- The Sting: However, if you miss a payment, they will send the debt to a collection agency immediately, which will tank your score. It is a “no-win” scenario for your Credit Rehabilitation.

4. The Balloon Payment vs. Installments

A payday loan is a “balloon” payment—the whole amount is due at once. This is the hardest way to pay back debt.

- The LendingMoney.ca Difference: We offer Installment-Based alternative loans. Instead of losing $500 of your next paycheck, you might pay $50 a month over a longer term. This protects your daily cash flow and allows you to breathe.

5. Aggressive Collection Tactics in 2026

With the 2026 digital banking updates, payday lenders use “Pre-Authorized Debit” agreements that are notoriously difficult to stop. If you try to block the payment to buy food, they may charge you NSF fees of $20–$50 on top of the 30% default interest they are legally allowed to charge.

Payday Loan vs. LendingMoney.ca Alternative Loan

Stop Digging. Start Building.

If you are currently using payday loans to stay afloat, you aren’t alone-but there is a better way. If you own your home, your equity is a “Financial Hero” waiting to be used.

At LendingMoney.ca, we use your home equity to provide a low-interest alternative to the payday trap. We pay off the high-interest lenders, lower your monthly payments, and start the process of moving you back to a traditional bank.

Ready to break the cycle? [Get a Payday Loan Exit Quote] from LendingMoney.ca today. Let’s trade your 365% debt for a plan that actually works.

Read blog – Breaking the Cycle: A Guide to Loans for Debt Consolidation with Poor Credit