A CRA lien is one of the most serious red flags a mortgage lender can encounter. In the 2026 lending environment, banks have become even more cautious about property titles, and a lien from the Canada Revenue Agency (CRA) can bring your mortgage renewal to a grinding halt.

If you are approaching your renewal date and have an outstanding tax debt, here is how a CRA lien changes the game and what you can do to save your home.

1. The Super Priority Problem

The reason banks fear a CRA lien is simple: The government usually gets paid first. In Canada, the CRA can exercise Super Priority for certain debts (like unremitted GST/HST or Payroll Source Deductions). Even if your bank registered their mortgage years ago, a CRA “Deemed Trust” claim can actually leapfrog the bank in the payout line.

- The Impact on Renewal: When you renew, your bank performs a title search. If they see a CRA lien (Notice of Certification), they may refuse to renew your mortgage because their security is now at risk. They don’t want to be “second in line” behind the taxman.

2. You Lose Your Switching Power

In 2026, many homeowners shop around at renewal to find a lower interest rate.

- The Trap: A new lender will never take on a mortgage if there is an existing CRA lien on the title. You are effectively “trapped” with your current lender, who may charge you a much higher “default” rate because they know you can’t leave.

- The Result: You lose all your negotiating leverage. You are forced to accept whatever rate your current lender offers-if they offer one at all.

3. The Automatic Payout Requirement

If your current lender does agree to renew or if you are trying to refinance to get extra cash, the CRA lien must be dealt with as part of the legal process.

- How it works: Your lawyer is legally required to use the mortgage funds to pay off the CRA lien before any money goes to you or your other debts.

- The Risk: If the tax debt is large enough, it might eat up all your equity, leaving you with a larger mortgage but no actual cash in hand to fix your financial situation.

4. The 2026 Risk Premium

Lenders in 2026 use AI-driven risk modeling. A CRA lien is seen as a sign of “systemic financial distress.”

- The Cost: Even if a lender agrees to renew with a lien on title, they may add a “Risk Premium” to your interest rate. You could end up paying 2% to 3% more than a neighbor with a clean title. Over a 5-year term, this can cost you tens of thousands of dollars.

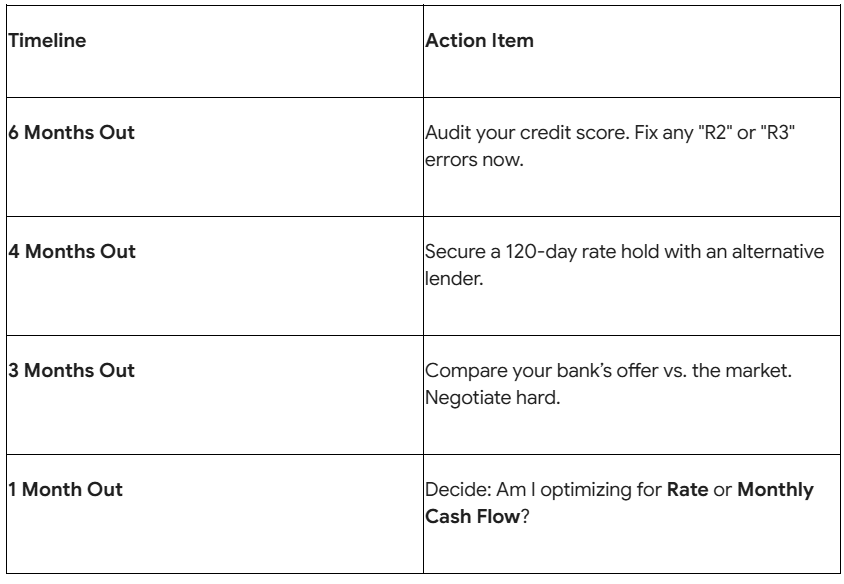

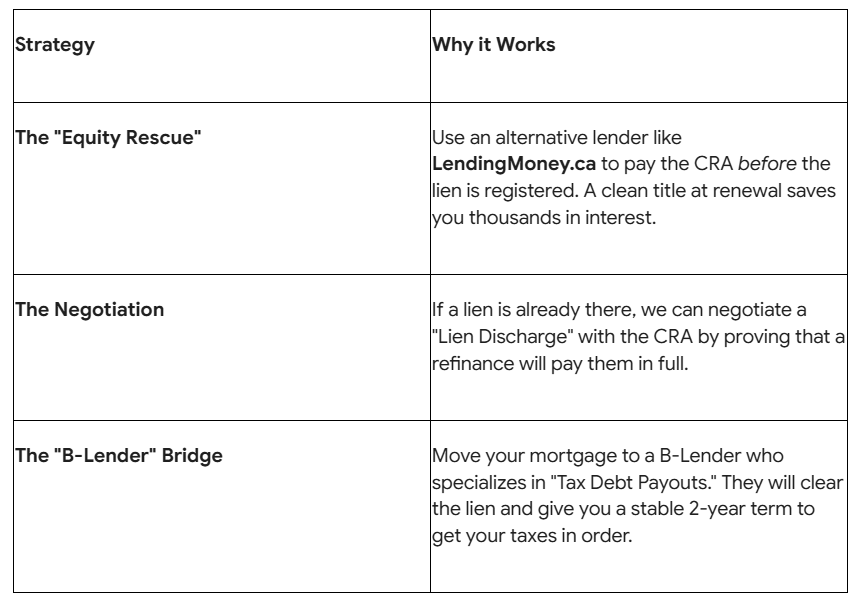

How to Fix the Situation Before Renewal

If you know you have a CRA debt but they haven’t placed a lien on your house yet, now is the time to act.

Don’t Let a Lien Steal Your Home

A CRA lien is a legal lock on your house, but LendingMoney.ca has the keys. We specialize in helping homeowners pay off the government so they can walk into their mortgage renewal with a clean title and a Financial Hero status.

Is your mortgage renewal coming up while you owe the CRA? [Connect with a Tax-Debt Specialist] at LendingMoney.ca today. We’ll help you clear the title and keep your home.

Reed More Blog – How to Fix Your Credit After a CRA Debt Settlement