The Great Renewal Wave of 2026 is officially here. Approximately 60% of all Canadian mortgages are coming due this year, and for many homeowners, the timing couldn’t be trickier. If you are entering your renewal window carrying high credit card balances, car loans, or CRA debt, you are facing a “Double Squeeze”: higher interest rates on your home and higher costs on your lifestyle.

At LendingMoney.ca, we don’t want you to just sign and hope when your bank sends that renewal letter. We want you to use this moment as a Financial Pivot. Here is how to navigate a 2026 mortgage renewal when your debt load is heavy.

1. The 2026 Reality: The Payment Shock is Real

If you locked in a rate of 1.5% to 2.5% back in 2021, your renewal in April 2026 will likely be in the 4.0% to 5.5% range.

- The Math: For a $500,000 mortgage, this jump could mean an extra $600 to $900 per month just for the house.

- The Danger: If you are already struggling to pay $1,000 a month in credit card interest, this “payment shock” could push your household budget into the red.

2. Don’t Auto-Renew Out of Fear

When you have high debt, you might feel like you have to stay with your current bank because you’re afraid a new lender will reject you.

- The Trap: Your current bank knows this. They may offer you a “posted rate” that is 1% higher than the market lead, assuming you won’t shop around.

- The Hero Move: In late 2024, the rules changed-uninsured borrowers (those with 20%+ equity) can now switch lenders at renewal without undergoing the Stress Test, provided the loan amount stays the same. This gives you massive leverage to find a better deal.

3. The Consolidation Renewal Strategy

This is the most powerful move for a high-debt homeowner in 2026. Instead of a “Straight Switch,” you perform a Refinance at Renewal.

- How it works: You increase your mortgage amount to pay off all your high-interest credit cards and loans.

- The Benefit: You move 22% interest debt into a ~5% mortgage. Even if your mortgage rate goes up, your total monthly debt payments usually drop by $1,000 or more.

- The Catch: This does require a stress test. If your debt is too high to qualify at a big bank, that’s where LendingMoney.ca steps in with alternative solutions.

4. Watch Your “GDS/TDS” Ratios

In 2026, lenders are looking closely at your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios.

- The Limit: Most banks want your total debt payments to be under 44% of your gross income.

- The 2026 Problem: Higher mortgage rates make these ratios climb quickly. If your credit cards are maxed out, you might exceed the 44% limit, causing a traditional bank to decline your renewal/refinance.

Renewal Options: Which Path is Yours?

| Strategy | Best For… | The Result |

| The Straight Switch | Good credit, but high rates. | Lower mortgage rate; no stress test. |

| Amortization Extension | Extreme cash-flow pressure. | Lower monthly payment; more total interest. |

| Debt Consolidation | High credit card/CRA debt. | Massive monthly savings; one payment. |

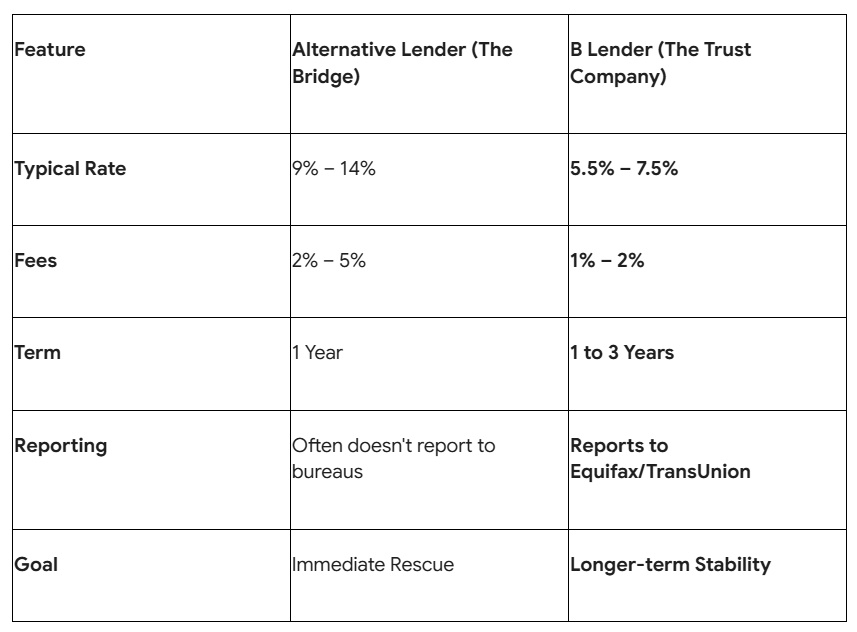

| Alternative Bridge | Bruised credit/Bank decline. | Clears the debt; prepares for 2027 bank return. |

5. The 120-Day Clock

In 2026, the market is volatile. Bond yields are shifting due to geopolitical tensions, and rates can change weekly.

- The Move: Start your renewal process 4 months before your expiry date.

Why Your Bank Won’t Tell You the Whole Truth

Your bank wants to keep your mortgage, but they don’t necessarily want to help you consolidate your debt-they make too much money off your 21% credit cards!

At LendingMoney.ca, we look at your Total Net Worth. We don’t just want to renew your mortgage; we want to restructure your entire financial life so that you actually start building equity again instead of just servicing interest.

Is your 2026 renewal notice sitting on your kitchen table? [Upload Your Renewal Offer] to LendingMoney.ca for a free “Debt-Load Analysis.” Let’s see if we can turn that renewal into a $1,200-a-month raise for your family.