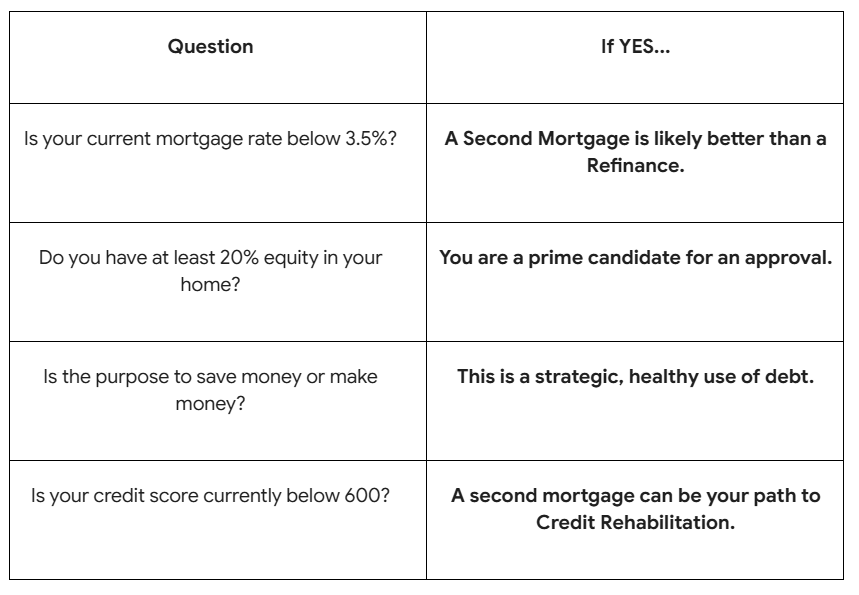

1. Why a Second Mortgage Beats a Bank Refinance

Many parents in 2026 are still holding onto low-rate first mortgages from 2021 or 2022 (around 2%-3%).

- The Bank Trap: If you ask your bank to “add $100,000” to your mortgage for your child’s down payment, they will likely force you to break your entire mortgage and refinance at today’s rates (likely 5%-6%).

- The Hero Move: A Second Mortgage from LendingMoney.ca sits behind your current mortgage. You keep your 2% bank rate on the bulk of your debt and only pay a higher rate on the new $100,000. This saves you thousands in interest and avoids massive prepayment penalties.

2. Turning Equity into a Gifted Down Payment

To help your child qualify for an “A-Lender” mortgage, the money you give them must be a gift, not a loan.

- The Gift Letter: Most lenders require a signed letter stating that the funds are a non-repayable gift.

- The Benefit: By providing a 20% down payment (e.g., $120,000 on a $600,000 condo), you save your child from paying CMHC Mortgage Insurance, which can cost them $15,000 to $25,000 upfront.

3. The Living Inheritance Strategy

In 2026, many Canadians are choosing to “give while living.

- Tax Efficiency: In Canada, there is no “gift tax” on cash given to your children. Giving the money now allows you to see the impact of your hard work while reducing the future size (and potential probate fees) of your estate.

- Property Protection: Using a Second Mortgage to provide a down payment keeps the child’s mortgage in their name only. This encourages their own financial independence while your primary home remains securely in your hands.

4. Protecting Yourself: The Equity Buffer

At LendingMoney.ca, we never want a parent to put their own retirement at risk. We follow a strict “Equity Buffer” rule:

- We typically recommend only borrowing against equity that exceeds 35% to 40% of your home’s value.

- This ensures that even if the 2026 market fluctuates, your own home remains safe, and you still have plenty of equity left for your own future needs (like long-term care or travel).

The Cost of Giving: $100,000 Case Study (2026)

| Feature | Breaking First Mortgage | LendingMoney.ca Second Mortgage |

| Prepayment Penalty | ~$12,000 – $20,000 | $0 |

| New Rate (Bulk of Debt) | 5.85% (Entire Balance) | 2.85% (Stays the same) |

| Approval Time | 2-3 Weeks | 3-5 Business Days |

| Impact on Mom & Dad | Higher monthly costs. | Small, manageable interest-only payment. |

| Impact on Child | Entry into Market Today. | Entry into Market Today. |

5. The Co-Signing Alternative

If your child has the down payment but lacks the income to pass the 2026 Stress Test, parents often consider co-signing.

- The Warning: Co-signing makes you 100% liable for their debt. It also counts against your credit, which might make it harder for you to get a car loan or renew your own mortgage later.

- The Better Way: Often, providing a larger “Gifted Down Payment” via a Second Mortgage allows the child to qualify on their own, keeping your name (and your credit) off their legal documents.

Be the Hero of Their Story

The “Great Wealth Transfer” is happening right now. You’ve worked hard to build equity in your home; a Second Mortgage is simply the tool that lets you deploy that wealth when your family needs it most.

Want to help your kids buy their first home in 2026? [Get an Equity Assessment] from LendingMoney.ca today. Let’s look at your home’s value and find a way to fund their future without compromising yours.

Read Blog – Second Mortgage Stops CRA Collections