For many, the term “second mortgage” once carried a certain stigma. It was something whispered about in times of crisis. However, as we move through 2026, the narrative has shifted. Today’s homeowners are using second mortgages to protect their low-rate first mortgages, fuel business growth, and navigate a complex tax environment.

A second mortgage is a loan secured against your property that sits behind your primary mortgage on the title. Because the lender is in “second position,” they take on more risk (if the home is sold, the first lender is paid first), which results in higher interest rates. But despite the cost, the benefits often far outweigh the price of the interest.

Here are the primary reasons why second mortgages have become the “Hero Move” for Ontario homeowners this year.

1. Protecting a Low-Rate First Mortgage

This is the #1 reason for a second mortgage in 2026. Many homeowners locked into 5-year fixed rates in 2021 or 2022 at rates between 1.5% and 2.5%.

If you need $50,000 today, you have two choices:

- Refinance: Break your entire mortgage and move the whole balance to today’s rate (likely 4.5% – 5.5%). This triggers massive prepayment penalties and increases the cost of your entire debt.

- The Second Mortgage: You leave your 2% mortgage exactly where it is. You only pay a higher rate on the new $50,000.

By keeping your “A-Lender” rate untouched, you save thousands in interest over the remaining years of your term.

2. High-Interest Debt Consolidation

In 2026, credit card interest rates have climbed to 21% – 24%, and personal lines of credit aren’t far behind. For a homeowner carrying $40,000 in consumer debt, the monthly interest alone can be “choking” their cash flow.

A second mortgage allows you to:

- Replace 22% interest with 9% – 12% interest.

- Collapse five or six monthly payments into one.

- The Credit Rehab Win: By paying off your credit cards in full, your credit utilization drops to zero, often causing your credit score to jump 50 to 100 points in a single 90-day cycle.

3. Resolving CRA Tax Arrears

As we’ve discussed in our tax series, the CRA is the only creditor in Canada with “Super Priority.” They don’t need a court order to freeze your bank account or garnish your wages.

Traditional banks will almost never give you money to pay off the CRA. They view tax debt as a sign of instability. A private second mortgage lender, however, is happy to lend you the funds to “kill” the tax debt.

- The Goal: Pay the CRA today to stop the 7% daily compounding interest and prevent a lien from being registered on your title.

4. Funding Value-Add Renovations

In 2026, many Canadians have decided to “Love It, Don’t List It.” With the costs of moving (land transfer taxes, real estate commissions, and legal fees) reaching $50,000+, many families prefer to renovate their existing space.

A second mortgage is perfect for:

- ADUs (Additional Dwelling Units): Converting a basement or garage into a rental suite to generate extra income.

- Major Overhauls: Kitchens and bathrooms that add more value to the home than the cost of the loan.

- Speed: Unlike a bank-led “Improvement Mortgage,” which requires multiple inspections and draws, a second mortgage provides the cash upfront so you can pay your contractors and get the job done.

5. Business Capital and Entrepreneurial Growth

Banks are notoriously difficult for small business owners. If you are self-employed or starting a new venture in 2026, a bank will likely want to see two years of perfect tax returns before they lend you a dime.

Entrepreneurs use second mortgages as working capital:

- To buy inventory in bulk at a discount.

- To fund a marketing push or hire a key employee.

- To bridge the gap while waiting for large invoices to be paid.

Since the loan is based on equity, not your business’s current P&L statement, it is the fastest way to inject cash into a growing company.

6. Helping the Next Generation (The Bank of Mom and Dad)

With the 2026 real estate market still challenging for young buyers, many parents are using second mortgages to “gift” a down payment to their children.

- By taking out a $100,000 second mortgage, parents can help their child enter the market today rather than waiting 10 years to save. This allows the family to build wealth across two properties simultaneously.

7. Emergency and Life Events

Life doesn’t always follow a budget. Unexpected medical expenses, a sudden divorce settlement, or helping a family member in a crisis can require a large amount of liquidity instantly.

A second mortgage can be funded in as little as 3 to 5 business days, making it the “Emergency Fund” for homeowners who are asset-rich but cash-poor.

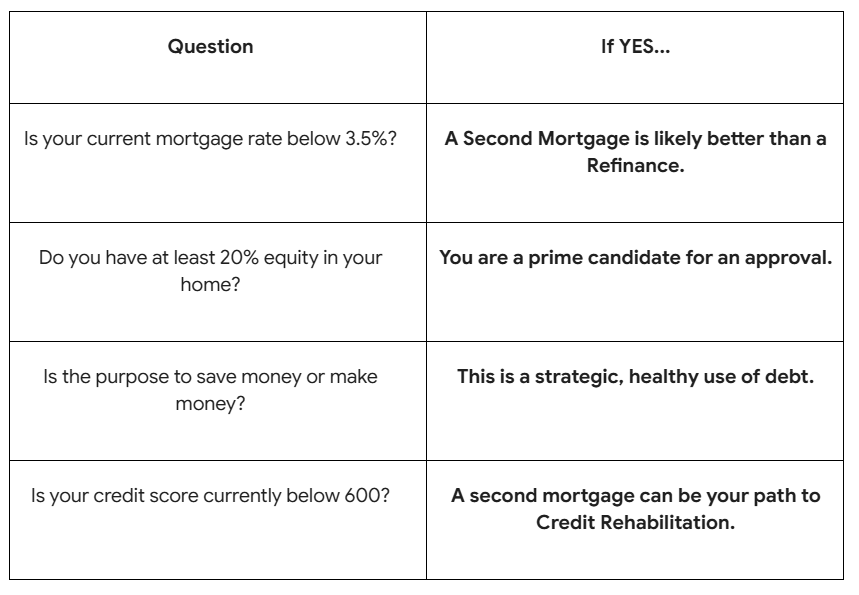

Is a Second Mortgage Right for You? (The 2026 Checklist)

Your Home, Your Future

At LendingMoney.ca, we don’t just see a second mortgage as a loan; we see it as a pivotal financial moment. Whether you are consolidating debt to save your credit or investing in your business to save your future, we match you with the lenders who value your equity and your story.

Ready to see how much equity you can unlock? [Get a Second Mortgage Quote] from a Financial Hero at LendingMoney.ca today. We’ll help you do the math and find the smartest path forward.