When an emergency strikes-a broken furnace in an Ontario winter or a sudden car repair-speed is usually your top priority. High-interest lenders capitalize on this urgency, offering “instant” cash that sounds manageable in small doses but becomes a predatory cycle over time.

To understand the 300% difference, we have to look past the per $100 marketing and focus on the Annual Percentage Rate (APR) and the velocity of repayment.

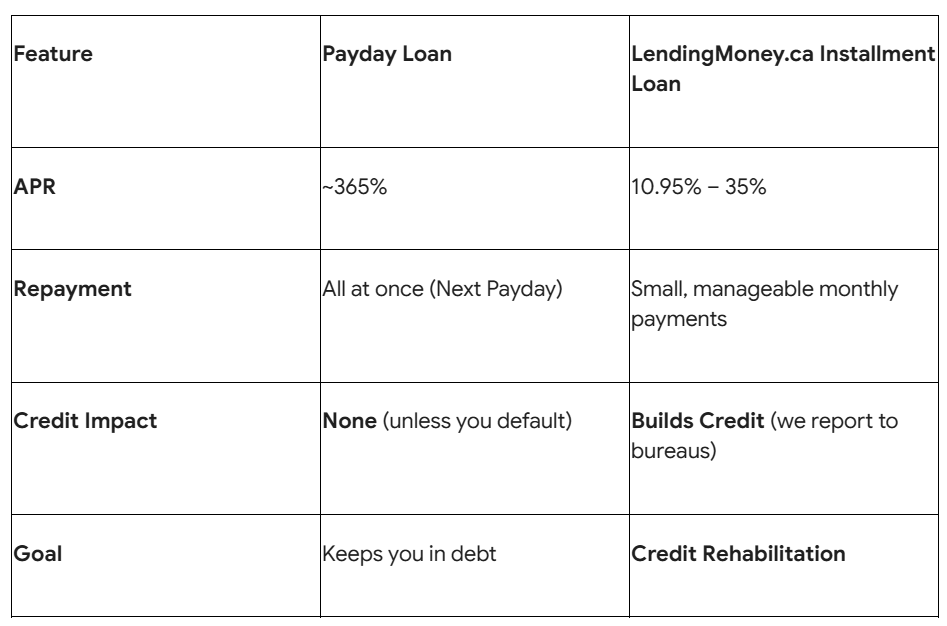

1. The Payday Loan: A 365% APR Sprint

Even in 2026, with tighter regulations, payday loans remain the most expensive way to borrow money in Canada. In Ontario, the legal limit for a payday loan is $14 per $100 borrowed.

The Math of the Trap

If you borrow $500 for a period of 14 days, you pay a $70 fee. On the surface, $70 for $500 sounds like a fair “convenience fee.” However, because that $70 is charged for only two weeks of use, the math looks very different when annualized:

- Payday Loan APR: ~$14 \times 26$ pay periods per year = 364% APR.

The Velocity Problem

The real danger of a payday loan isn’t just the rate; it’s the velocity. You must pay the entire $570 back the moment your next paycheck hits your account. For most families, losing $570 of a single paycheck creates a new “cash gap,” forcing them to borrow again immediately. This is the “Payday Treadmill”-a cycle designed to keep you paying fees without ever reducing your debt.

2. The Unsecured Installment Loan: A Structured Recovery

At LendingMoney.ca, our unsecured installment loans are designed for Credit Rehabilitation. Instead of a 14-day sprint, an installment loan is a marathon that you are actually equipped to win.

The Math of the Solution

An unsecured installment loan from a “Financial Hero” lender typically carries an APR between 8.9% and 34.9%, depending on your credit profile.

- The Installment Difference: Even at the higher end of the 2026 legal cap (35%), the APR is ten times lower than a payday loan.

The Cash Flow Advantage

Unlike the payday loan that demands $500 back in two weeks, an installment loan spreads that same $500 (or $5,000) over 12 to 60 months.

- Scenario: A $1,000 loan from a payday lender costs $1,140 in 14 days.

- The Alternative: A $1,000 unsecured loan from LendingMoney.ca might cost roughly $90 per month.

By lowering the “velocity” of repayment, you keep more of your paycheck for essentials like rent and groceries, effectively breaking the cycle of re-borrowing.

3. The 300% Difference: A Tale of Two Borrowers

Let’s look at the “Real Cost” of borrowing $1,500 for one year.

Borrower A (The Money Mart Path)

Borrower A takes a $1,500 payday loan and “rolls it over” every two weeks because they can never afford to pay it all back at once.

- Fees per 2 weeks: $210

- Total Fees after 1 Year: $5,460

- Principal still owed: $1,500

- Total Cost: $6,960

Borrower B (The LendingMoney.ca Path)

Borrower B takes a $1,500 unsecured installment loan at an APR of 19.9%.

- Monthly Payment: ~$139

- Total Interest after 1 Year: $168

- Principal paid off: $1,500

- Total Cost: $1,668

The Verdict: Borrower A paid over 300% more than Borrower B and is still in debt. Borrower B is debt-free and has an improved credit score.

4. Why Unsecured Loans Build Credit (And Payday Loans Don’t)

In 2026, your credit score is influenced by Credit Mix.

- Payday Loans: These are “invisible” to credit bureaus when you pay them on time, but “poisonous” if you fail. They do nothing to help you move back to a traditional bank.

- Unsecured Installment Loans: These are reported to Equifax and TransUnion every month. By making small, predictable payments, you are building a history of “Installment Credit,” which is one of the fastest ways to rehabilitate your score and qualify for an A-Lender mortgage in the future.

5. Avoiding the Optional Insurance Trap

In the 2026 high-interest market, many installment lenders (like the “Big Box” stores) try to close the 300% gap by selling “Loan Protection Insurance.”

- The Money Mart Tactic: They may offer a 35% loan but add a $90/month insurance premium. This can jump your total repayment from $13,000 to $16,000 over three years.

- The LendingMoney.ca Promise: We focus on transparency. Our unsecured loans are about Credit Rehabilitation, not “add-on” profits. We show you the total cost of borrowing upfront, with no hidden fees.

6. Self-Employed? Your Income is Your Asset

One reason people turn to payday loans is that banks won’t look at “Stated Income.” At LendingMoney.ca, we use 2026 Open Banking protocols to look at your real-time bank statements. If you have a steady cash flow from your business, you qualify for a “Heroic” unsecured loan, even without a high credit score or traditional T4 slips.

Stop Sprinting. Start Rebuilding.

The 300% difference is more than just a number; it is the difference between surviving paycheck-to-paycheck and actually building a future. If you are currently trapped in the payday loan cycle, it’s time to trade that 365% APR for a structured, manageable plan.

Ready to see the 300% difference for yourself? [Check Your Unsecured Rate] at LendingMoney.ca today. Our Financial Hero team will help you consolidate your high-interest debt into one simple, credit-building payment.