You’ve done the hard work: you’ve improved your credit, stabilized your income, or sold your property. Now comes the final step in your “Private-to-Bank” journey: The Discharge.

In 2026, discharging a private mortgage in Ontario is a formal legal process. While a bank discharge is often automated, a private discharge requires coordination between two sets of lawyers and a “Cessation of Charge” on your property title. At LendingMoney.ca, we consider this the “Graduation Day” of your Credit Rehabilitation.

Here is your 2026 guide to the final step of exiting a private mortgage.

1. Requesting the Payout Statement

The discharge process begins with a document called a Payout Statement (or Discharge Statement). This isn’t just your remaining balance; it is a legally binding breakdown of every dollar needed to release the lender’s claim on your home.

- What’s Included: The principal balance, interest owing up to the payout date, and the Lender’s Discharge Fee (typically $300–$600 in 2026).

- The “Daily Interest” Factor: Payout statements include a “per diem” (daily) interest amount. This ensures that if your new bank loan closes a day late, the private lender still gets their exact interest.

- The Hero Move: Request your statement at least 10 business days before your closing date. Private lenders are often individuals or small firms and may not produce documents as quickly as a big bank.

2. The Lawyer’s Role: Cessation of Charge

In Ontario, you cannot simply hand a check to a private lender and be done. The “Charge” (the mortgage) is registered against your home’s title at the Land Registry Office.

- The Process: Your lawyer sends the funds to the lender’s lawyer. In exchange, the lender’s lawyer provides a Discharge of Charge (Form 4).

- The 2026 Registry: Once this is electronically filed, the mortgage is “discharged,” and your title is officially clear. This is vital because you cannot secure a new “A-Lender” mortgage or sell your home until the old private charge is gone.

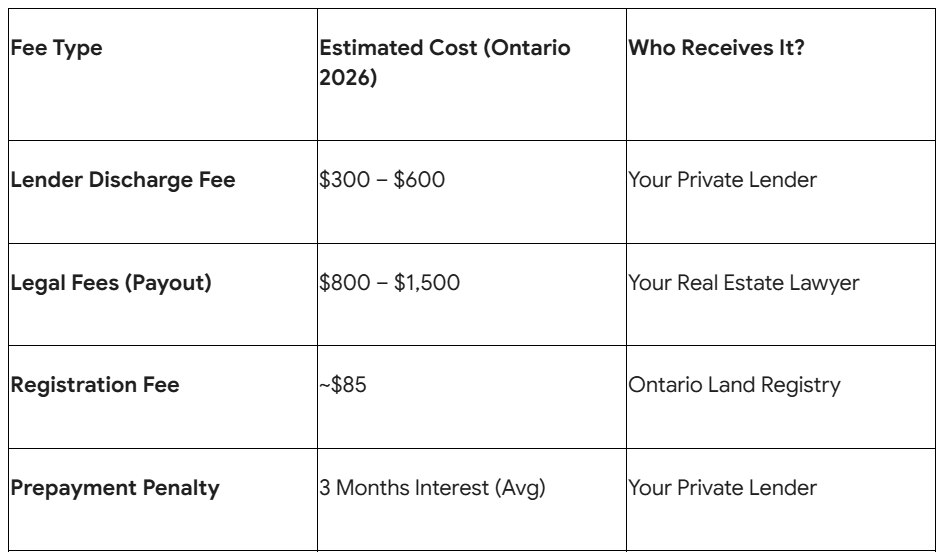

3. 2026 Payout Costs: What to Expect

Discharging a mortgage isn’t free. In 2026, you should budget for the following “Exit Costs”:

The Strategy: At LendingMoney.ca, we try to bake these costs into your new mortgage so you don’t have to pay them out of pocket on closing day.

4. The Holdback Trap

Sometimes, a private lender will “hold back” a small amount (e.g., $500–$1,000) for a few days after the payout to ensure all checks clear and there are no outstanding property tax issues.

- The Hero Move: Ensure your lawyer confirms in writing that the holdback will be released within a specific timeframe (usually 48–72 hours).

5. Dealing with Difficult Private Lenders

Under the Ontario Mortgages Act (Section 22), a lender cannot “refuse” to give you a discharge statement if you are paying them in full.

- The Reality: In 2026, if a private lender is ignoring your requests or trying to charge “mystery fees” at the last minute, your lawyer can apply for a Court Order to discharge the mortgage.

Discharge Checklist (2026)

- [ ] 15 Days Out: Confirm your lawyer has requested the Payout Statement.

- [ ] 10 Days Out: Review the statement for any “hidden fees” we didn’t agree to in the original commitment.

- [ ] Closing Day: Ensure the funds are wired (not mailed) for the fastest discharge.

- [ ] Post-Closing: Ask your lawyer for the “Registered Discharge” or a copy of your new, clean Title Search.

Celebrate Your Graduation

Discharging your private mortgage is the final hurdle in your Credit Rehabilitation. It means you have moved from “Emergency Financing” back into “Mainstream Stability.”

At LendingMoney.ca, we love seeing our clients reach this stage. It means the “bridge” did its job, and you are now standing on solid financial ground.

Getting ready to pay off your private loan? [Connect with our Discharge Specialist] at LendingMoney.ca. We’ll coordinate with your lawyer and ensure your exit is as smooth (and cheap) as possible.