In 2026, the marketing around “fast cash” has become incredibly sophisticated. Big-name lenders like Money Mart are no longer just “payday” shops; they have aggressively pivoted into High-Cost Installment Loans.

While these might look like a better deal than a 14-day payday loan, the “Real Cost” over 12 to 36 months can be devastating to your long-term wealth. At LendingMoney.ca, we believe in Credit Rehabilitation, which means using the lowest cost of capital available to you-your home equity-to kill high-interest debt forever.

Here is the breakdown of the real cost between high-interest installments and an alternative equity-backed loan.

Payday vs. Installments vs. Equity: What’s the Real Cost?

When you’re in a financial pinch, lenders know you are focused on one number: the monthly payment. But the monthly payment is a mask. To see the true cost of a loan, you have to look at the Total Cost of Borrowing.

In 2026, the federal government has capped the criminal interest rate at 35% APR. While this sounds like a win for consumers, high-cost lenders have responded by adding “optional” insurance, administration fees, and longer terms to keep their profits high.

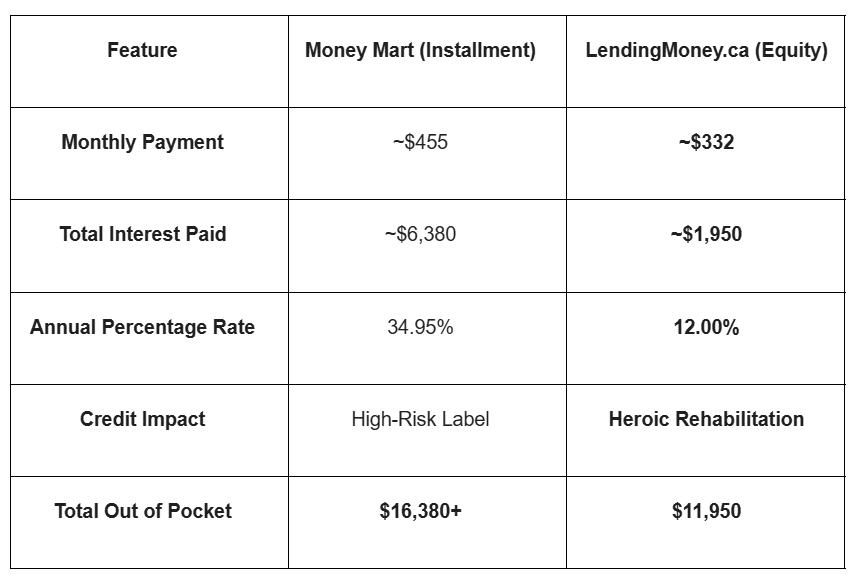

1. The Money Mart Installment Loan (35% APR + Fees)

If you borrow $10,000 from a high-cost installment lender in 2026 to consolidate your debts, your contract might look like this:

- Interest Rate: ~34.95% APR

- Term: 36 Months

- Monthly Payment: ~$455.00

- Optional Insurance: ~$92.00/month (often “highly recommended” for approval)

The Real Cost: After 3 years, you haven’t just paid back $10,000. You’ve paid back roughly $16,380 (or over $19,000 with insurance). You have effectively paid for your debt nearly twice.

2. The Payday Loan Treadmill (The 365% Trap)

If you skip the installment loan and go for a classic $500 payday loan:

- The Fee: $14 per $100 borrowed ($70 fee).

- The Cycle: Because you have to pay the full $570 back in 14 days, you likely have to borrow again to pay rent.

- The Real Cost: If you “roll over” this debt for just six months, you will have paid over $900 in fees while still owing the original $500.

3. The LendingMoney.ca Alternative (9% – 15% APR)

Now, let’s look at using a Second Mortgage or Equity Loan to solve the same $10,000 problem:

- Interest Rate: ~12% APR

- Term: 36 Months (Amortized)

- Monthly Payment: ~$332.00

- Insurance/Hidden Fees: $0 (We focus on the equity in your home, not selling you add-ons).

The Real Cost: After 3 years, you’ve paid back $11,950.

2026 Cost Comparison: Borrowing $10,000

Why the Alternative Path Wins Every Time

The reason Money Mart’s costs are so high is that they are lending to thousands of people with no collateral. They expect many of them to fail, so you (the person who pays) have to cover the cost of those who don’t.

At LendingMoney.ca, we use your Home Equity as your “Financial Hero.” Because the loan is secured by your home, the risk is lower, which allows us to provide a rate that is one-third the cost of an unsecured installment loan.

The Hidden Danger of High-Interest Installments

In 2026, many banks see a “High-Interest Installment Loan” on a credit bureau as a sign of financial instability. Even if you pay it on time, it can actually make it harder to graduate to a traditional bank mortgage later. An equity-backed loan from LendingMoney.ca, however, shows you are a savvy homeowner using your assets strategically.

Stop Overpaying for Your Own Money

Every dollar you pay in 35% interest is a dollar taken away from your retirement, your children’s education, or your next home. If you own your home, you have already earned the right to lower interest rates.

Comparing a loan offer from Money Mart or another high-cost lender? [Upload Your Quote] to LendingMoney.ca for a “Real Cost Analysis.” Let us show you how much of your own money you can keep.

Read blog – Navigating Your Options: A Guide to Professional Debt Consolidation Services in Canada