If you have a private mortgage, you probably remember the “Lender Fee and Broker Fee you paid to get it. What many homeowners don’t realize is that most private lenders charge those fees every single year you stay with them.

In 2026, with private interest rates already sitting between 10% and 15%, adding a 2% renewal fee means you are effectively paying an APR of nearly 17%. If you have a $500,000 mortgage, that’s $10,000 vanished in a single signature. Here is how to stop the bleed.

1. The 120-Day Rule (Start Before They Do)

Private lenders count on you being “trapped.” They often send your renewal notice just 21 to 30 days before the term ends, leaving you with no time to find an alternative.

- The Hero Move: Start your search 4 months (120 days) before your maturity date.

- The LendingMoney.ca Advantage: We track your maturity date from day one. At the 4-month mark, we perform a “Financial Health Check” to see if your Credit Rehabilitation is far enough along to move you to a B-Lender or a Credit Union where there are zero renewal fees.

2. Leverage Your Improved Story

A private lender charges a renewal fee because they claim the “risk” is still high. You need to prove them wrong.

- Show the Progress: Since you took the private loan, have you paid off a collection? Has your income increased? Have you made every private mortgage payment on time?

- The Negotiation: At LendingMoney.ca, we use these “wins” to negotiate. We tell the lender: “Our client’s credit score has jumped 60 points. They are now eligible for a B-Lender. If you want to keep this loan, you must waive the renewal fee.”

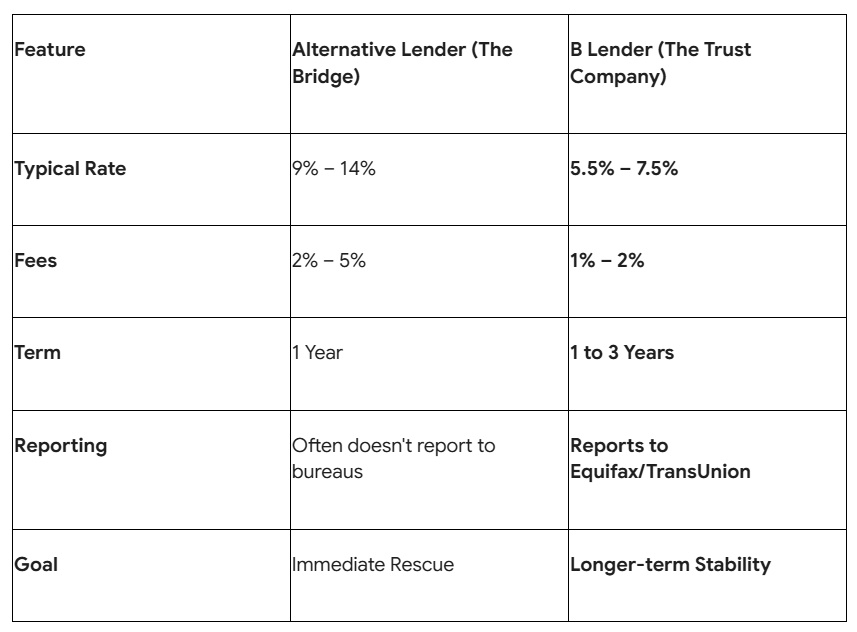

3. The B-Lender Pivot (The Fee-Free Zone)

The best way to avoid private renewal fees is to stop being a private borrower. In 2026, the jump from “Private” (C-Lender) to “Alternative” (B-Lender) is the most important step in your journey.

- B-Lenders (Trust Companies): Unlike private individuals, B-Lenders are regulated institutions. They generally do not charge renewal fees. Once you are in, you simply renew at the current market rate.

- The Savings: Moving to a B-Lender doesn’t just lower your interest rate; it saves you that 1%–2% annual fee forever.

4. Don’t Auto-Renew by Silence

Many private mortgage contracts have a clause that says if you don’t respond, the mortgage “auto-renews” for another year, including the fees.

- The Action Step: Read your original commitment letter. Look for the “Renewal” section.

- The 2026 Reality: Some lenders are now charging “Exit Fees” if you leave. We review your contract to ensure the cost of leaving is smaller than the cost of staying. Usually, paying a small discharge fee is much cheaper than paying a massive renewal fee.

5. Use a Bridge-to-Bank Strategy

If your credit isn’t quite ready for a bank yet, we can sometimes find a “Semi-Private” institution. These are lenders that sit between a private individual and a bank.

- The Benefit: They offer 2-year or 3-year terms.

- Why this works: By taking a 3-year term, you only pay a fee once instead of paying a renewal fee every 12 months. This gives you three years of stable payments to finish your Credit Rehabilitation.

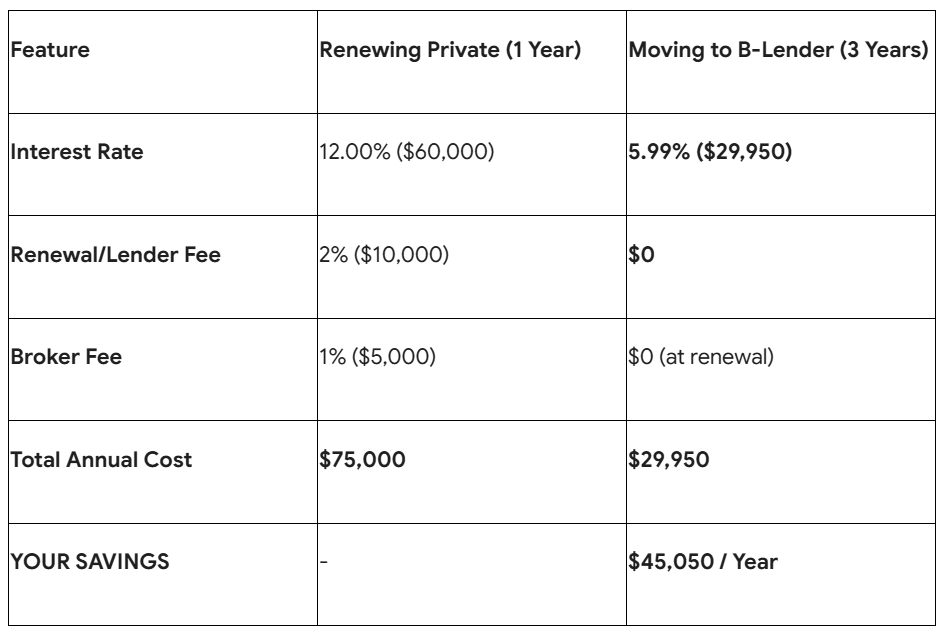

Comparison: The Cost of Staying vs. The Cost of Moving (2026)

Based on a $500,000 Mortgage

Your Equity Belongs to You, Not the Lender

At LendingMoney.ca, we believe private mortgages should be short, sharp, and successful. If you are entering your second or third year in a private loan, you are no longer using a “bridge”, you are living on it.

Is your private mortgage renewal coming up in the next 120 days? [Upload Your Current Statement] for a free Exit Analysis. Let’s stop the fees and start your graduation back to the bank.