Power of Sale, pay off a large CRA debt, or bridge a gap while self-employed. But a private mortgage is like a spare tire: it’s designed to get you to the repair shop, not to drive on for years.

In 2026, many Ontario homeowners are finding that their “temporary” private loans have become permanent weights. If you’re paying 12% or higher interest plus monthly fees, you’re likely not making a dent in your principal. At LendingMoney.ca, we specialize in the “Private-to-Bank Pivot.” Here is how to renegotiate your position and lower your rates.

1. Why You Need an Exit Strategy Now

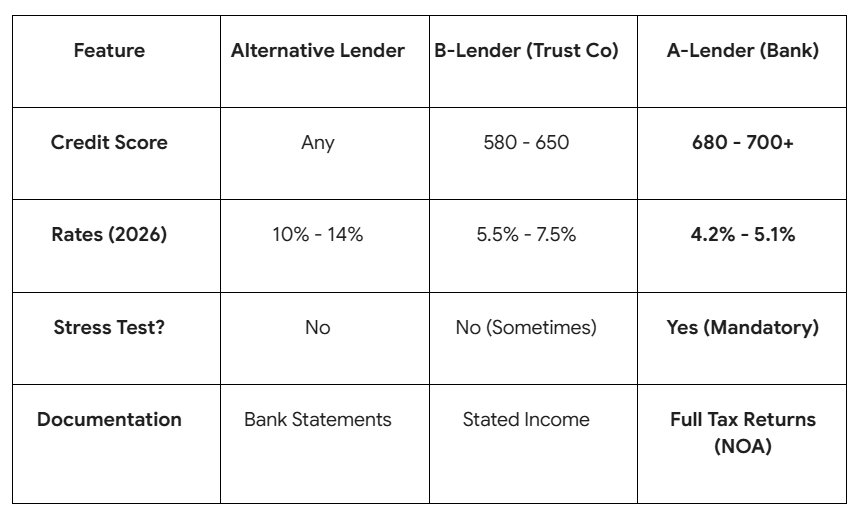

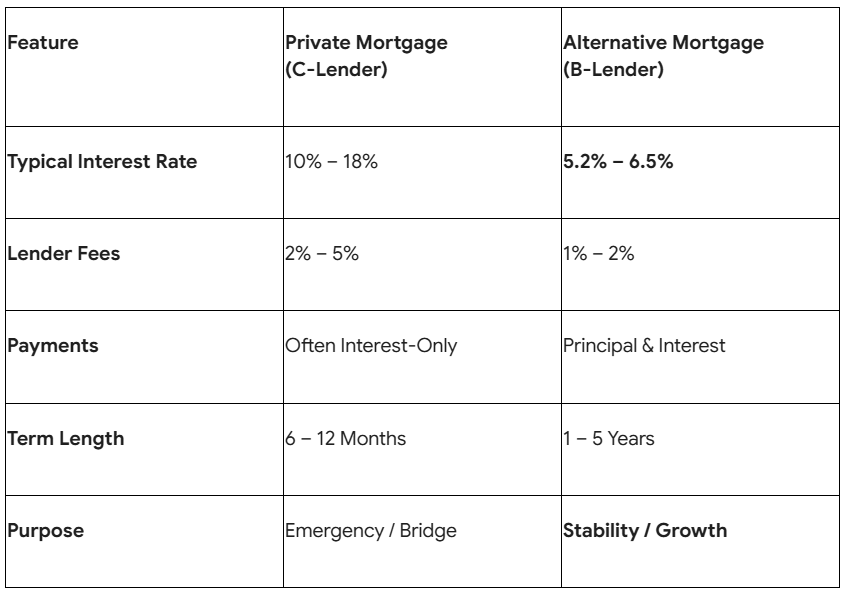

In 2026, the Bank of Canada has stabilized rates around 2.25%, meaning “B-Lenders” (Trust Companies) are offering rates in the 5% to 6% range.

- The Cost of Waiting: If you have a $500,000 private mortgage at 12%, you are paying $5,000 per month in interest alone.

- The B-Lender Alternative: Moving that same loan to a B-Lender at 5.9% would drop your interest cost to roughly $2,450 per month.

- The Result: That’s $2,550 per month back in your pocket—money that could be used to actually pay off your home.

2. Step 1: The Mid-Term Credit Audit

Most private mortgages have 12-month terms. The biggest mistake homeowners make is waiting until month 11 to think about an exit.

- The LendingMoney.ca Approach: We start your Credit Rehabilitation on Day 1. If you took a private loan because of a low credit score, we use the first 6 months of that term to ensure your “tradelines” (credit cards and small loans) are being paid perfectly.

- The Goal: To move to a B-Lender, you generally need a credit score of 550–600. To move back to an A-Lender (Bank), you need 680+. We track your progress to ensure you hit these benchmarks before your private loan expires.

3. Step 2: Income Storytelling

Many people are in private mortgages because they are self-employed and the bank didn’t “understand” their income.

- The Renegotiation: At LendingMoney.ca, we don’t just send your tax returns to a lender. We package your bank statements, contracts, and business growth plans.

- The 2026 Shift: In today’s market, alternative lenders are much more willing to look at “Gross Revenue” rather than “Net Income.” We use this to prove you can handle a lower-interest institutional loan.

4. Step 3: The Equity Appraisal Update

In 2026, home values in Ontario have stabilized. If your home has increased in value since you took your private mortgage, your Loan-to-Value (LTV) ratio has improved.

- Why LTV Matters: Private lenders take the highest risk, so they charge the highest rates. As your equity grows, your risk profile drops.

- The Move: We order a new appraisal to show that you now have 25% or 30% equity. This “unlocks” the door to B-Lenders who require a 20% equity stake but offer rates that are half of what you’re currently paying.

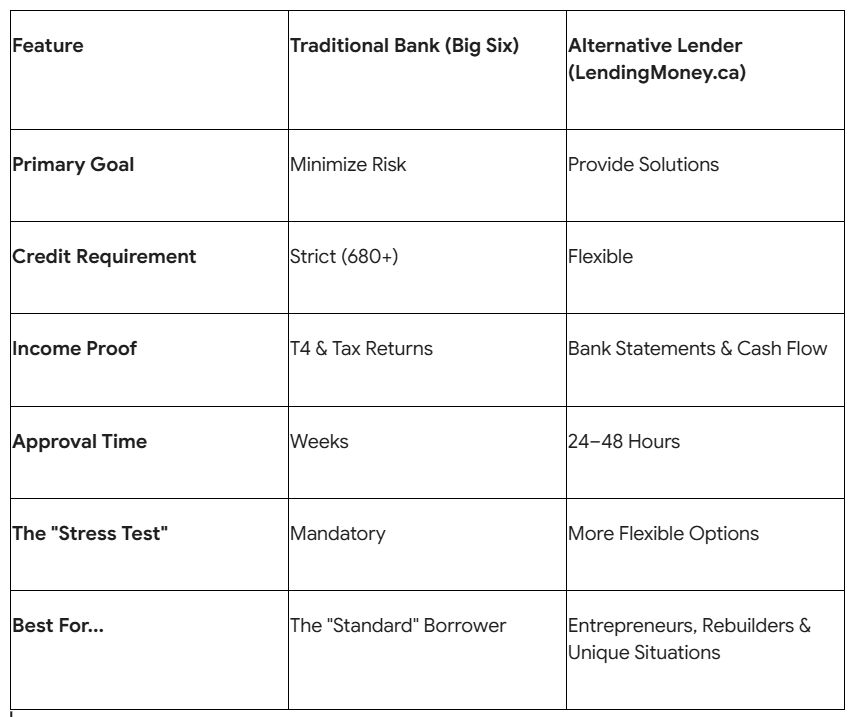

Private vs. B-Lender Comparison (2026)

5. How LendingMoney.ca Renegotiates for You

When you work with a Financial Hero at LendingMoney.ca, we act as your advocate. We don’t just wait for your private lender to send a renewal notice (which often comes with a massive “Renewal Fee”).

- We Negotiate the Add-Backs: We argue for your business expenses and one-time costs to be added back to your income, qualifying you for better rates.

We Manage the Paperwork: Moving from a private individual to a regulated institution requires a lot of documentation. We handle the heavy lifting so you don’t have to.

Don’t Renew Your Stress-Refinance Your Future

A private mortgage renewal notice is a wake-up call. Don’t just sign it and accept another year of high interest. Use the equity you’ve built to “graduate” to a better class of lender.

Is your private mortgage term coming to an end? [Request a Private-to-Bank Analysis] from LendingMoney.ca today. Let’s see how much we can drop your rate and start your journey back to the bank.