If you are currently juggling multiple payday loans from lenders like Money Mart, you aren’t just paying high interest-you are losing your cash flow. To stop the cycle, you need to replace “emergency” money with equity money. Here is the 2026 step-by-step roadmap to making the transition.

1. Stop the Re-Borrowing Reflex

The hardest part of the transition is the first 14 days. When your paycheck hits and the payday lender takes their share, your first instinct will be to walk back into the store and borrow it again.

- The Transition Move: Before your next payday, [connect with LendingMoney. We can often secure an alternative equity loan in as little as 3 to 5 business days. Having the approval in place before your paycheck disappears gives you the confidence to break the re-borrowing habit.

2. Calculate the Freedom Number

List every single payday loan, high-interest installment loan, and “cash advance” app balance you currently have.

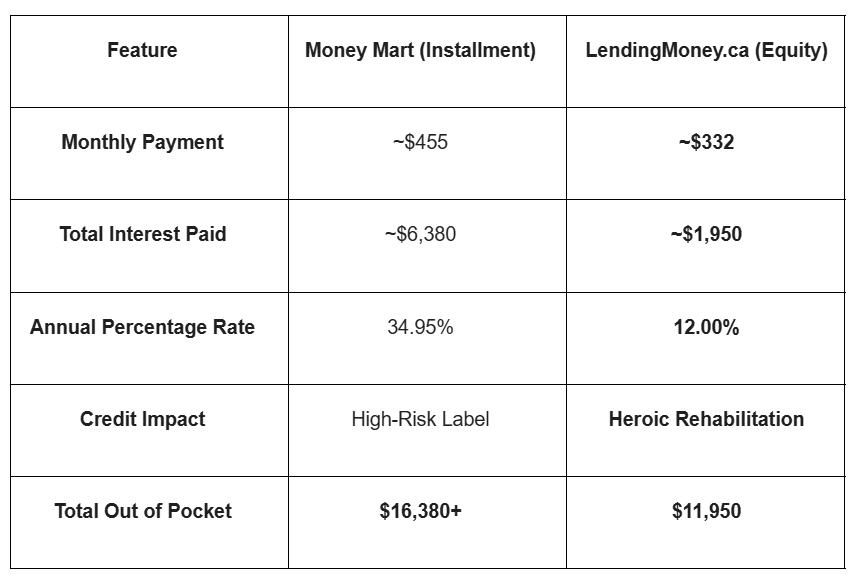

- The 2026 Reality: In Ontario, even with new caps, a $500 payday loan costs $70 in fees every two weeks. If you have three of these, you are losing $140 per week just to stay in debt.

- The Strategy: Your “Freedom Number” is the total amount needed to pay every one of these lenders to zero. This is the amount we will target with your home equity loan.

3. Leverage Your Quiet Equity

You don’t need a perfect credit score to use your home equity. In 2026, alternative lenders focus on the LTV (Loan-to-Value) ratio.

- The Math: If your home is worth $700,000 and you owe $400,000, you have $300,000 in equity. We can use a small slice of that (e.g., $15,000) to pay off all your payday loans.

- The Comparison: * Payday Loan: ~365% APR (due in 14 days).

- Equity Loan: ~10% – 12% APR (due over 12–24 months).

4. The Direct Payout Method

To ensure you successfully break the cycle, LendingMoney.ca will facilitate a direct payout.

- How it works: Instead of putting the money in your bank account (where a payday lender might try to grab it via a pre-authorized debit), the funds can be used to pay the lenders directly.

- The Result: You wake up the next morning with zero payday debt. Your “Requirement to Pay” agreements are cancelled, and your paycheck is finally yours again.

5. Rebuild Your inancial Hero Score

Payday loans are “invisible” to your credit score when you pay them, but “poison” when you don’t. An equity loan from an alternative lender is different.

- The Rehabilitation: By paying off the high-interest debt, your “Debt-to-Income” ratio improves instantly.

- The Next Step: Once the payday “noise” is gone from your bank statements, you become a candidate for B-Lending and eventually A-Lending at much lower rates.

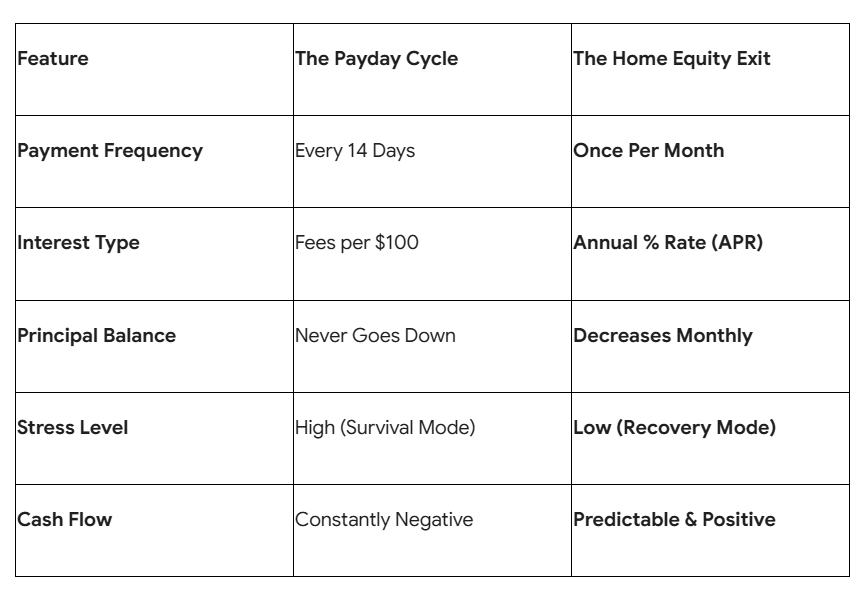

Transition Comparison (2026)

Your Home is Your Way Out

If you own a home in Ontario, you have a “Financial Hero” sitting in your driveway. There is no reason to pay 365% interest to a payday lender when you have equity available at a fraction of the cost.

Are you ready to stop the payday treadmill? [Request an Equity Rescue Analysis] from LendingMoney.ca today. Let’s use your home to buy back your paycheck.