When you’re buried under high-interest debt, the goal is always the same: find a way out. In the Canadian financial landscape of 2026, two primary paths emerge: the Debt Consolidation Loan and the Consumer Proposal.

While they might sound similar – both result in one monthly payment – they are fundamentally different tools. Choosing the wrong one could cost you thousands of dollars or years of unnecessary stress. At LendingMoney.ca, we’re here to help you weigh the pros and cons so you can make an informed decision for your financial future.

The Debt Consolidation Loan: The Refinance Strategy

A debt consolidation loan is a new personal loan used to pay off all your smaller, high-interest debts (like credit cards). You are essentially moving your debt from several “expensive” places to one “cheaper” place.

The Pros:

- Protects Your Credit Score: As long as you make your payments on time, your credit score usually stays stable or even improves as your credit utilization drops.

- Total Control: You aren’t entering a legal process. You maintain your relationship with your bank and keep your current credit limits (though we recommend closing them to avoid re-spending!).

- Simplified Life: One due date, one interest rate, and a clear “end date” for your debt.

The Cons:

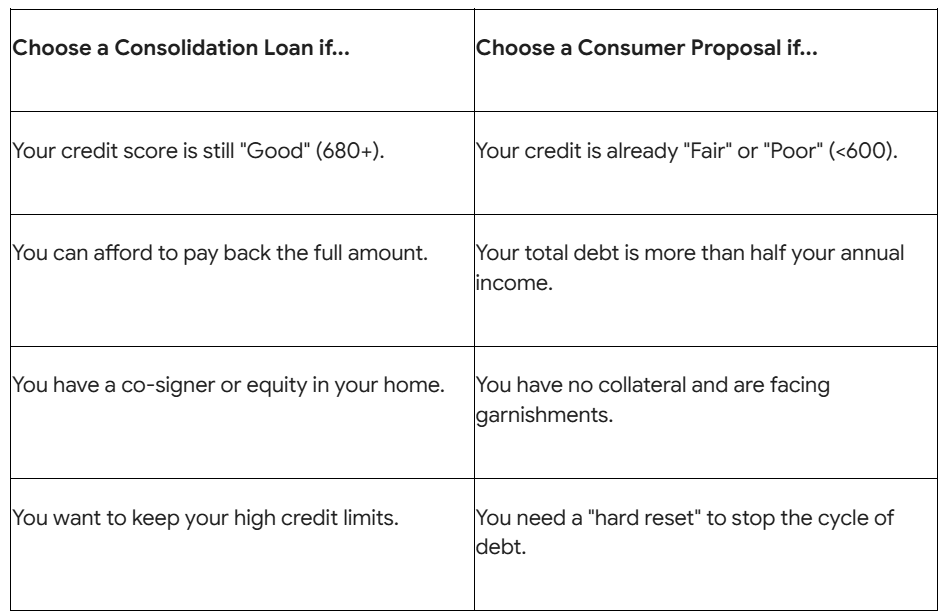

- Harder to Qualify: In 2026, lenders have tightened their belts. To get a rate low enough to make consolidation worth it, you typically need a credit score of 680 or higher.

- No Debt Reduction: You still owe 100% of the principal. If you owe $40,000, you are still paying back $40,000 plus interest.

- The “Debt Trap” Risk: If you don’t change your spending habits, you might end up with a consolidation loan plus new credit card balances.

The Consumer Proposal: The Settlement Strategy

A Consumer Proposal is a legal agreement where you offer to pay your creditors a percentage of what you owe, interest-free, over a period of up to five years.

The Pros:

- Principal Reduction: You can often reduce your total debt by 50% to 80%. If you owe $40,000, you might only pay back $12,000.

- Legal Protection: The moment you file, all interest stops, and creditors are legally forbidden from calling you or garnishing your wages.

- No Interest: Every dollar you pay goes directly toward the principal.

The Cons:

- Credit Impact: It carries an R7 rating on your credit report. This will make it difficult to get traditional low-interest loans for a few years.

- Public Record: It is a formal insolvency proceeding.

- The “R7” Footprint: It stays on your credit report for 3 years after you finish the payments (or 6 years after you start, whichever is sooner).

Which One is Right for You?

The LendingMoney.ca Verdict

At LendingMoney.ca, we don’t believe in a one-size-fits-all approach. If you have the credit to qualify, a Consolidation Loan is a fantastic way to save on interest while keeping your credit score pristine. However, if the math simply doesn’t add up and you’ll be in debt for the next 20 years, a Consumer Proposal is the more heroic choice for your long-term health.

Confused about which path to take? [Speak with a Financial Hero] today. We’ll run the numbers with you and find the strategy that fits your 2026 goals.