In the middle of a separation, your focus is likely on legal fees, living arrangements, and your family’s well-being. However, there is a silent observer watching every move: the credit bureaus.

In 2026, the financial ties between couples are more digital and integrated than ever before. A single missed payment by an ex-partner on a joint card can drop your score by 100 points overnight, potentially locking you out of a new home or car exactly when you need them most.

At LendingMoney.ca, we believe that Credit Rehabilitation starts with a strong defense. Here is your step-by-step playbook to shielding your credit score during a separation.

1. The Audit Phase: Know What’s Joint

You cannot protect what you don’t know exists. Many couples have “ghost” accounts – store cards or old lines of credit they haven’t used in years.

- Action Step: Download your free reports from both Equifax and TransUnion.

- The Hunt: Look specifically for accounts labeled as “Joint,” “Co-Applicant,” or “Secondary Cardholder.”

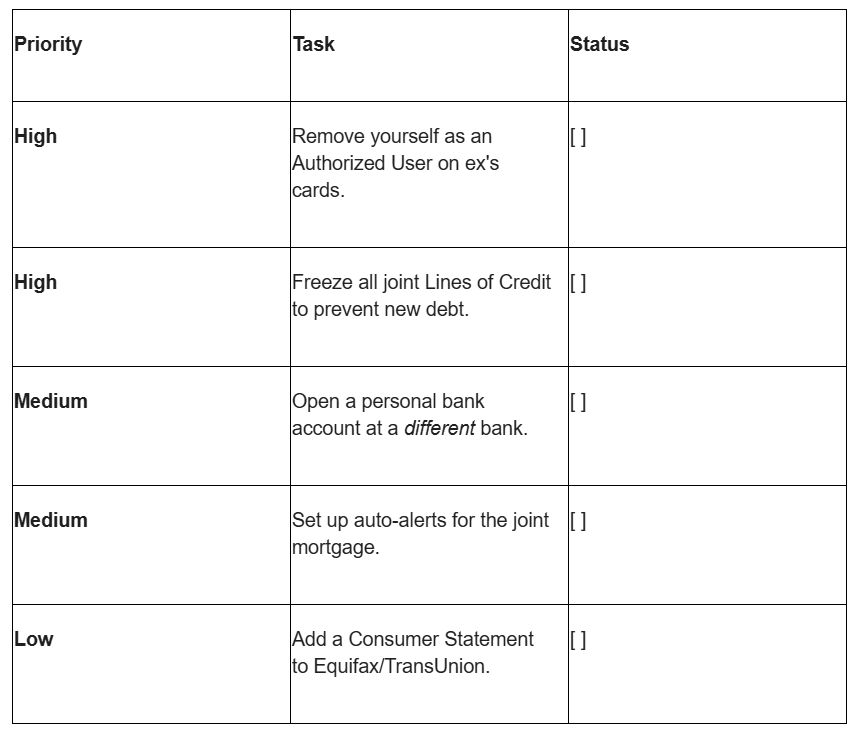

- The “Authorized User” Trap: Even if you aren’t a joint owner, being an “Authorized User” on your ex’s card can impact your score. If they max out the card, your Utilization Ratio will skyrocket.

2. Freeze and Close (The Clean Break)

A separation agreement is a contract between you and your spouse – it is not a contract between you and the bank.

- The Reality: If your name is on a $20,000 Line of Credit, you are 100% liable for that debt, regardless of what your lawyer says.

- The Move: Contact your lenders immediately to “freeze” joint lines of credit and credit cards so no new charges can be made.

- The Goal: Work toward closing these accounts. If there is a balance, it must be paid off or moved to an Individual Consolidation Loan in one person’s name.

3. The Stay in Touch Strategy (For the Mortgage)

The biggest threat to your credit during separation is the mortgage.

- The Problem: If your ex stays in the house and “forgets” to pay the mortgage for two months, your credit is ruined.

- The Solution: Set up Account Alerts. Most Canadian banks in 2026 allow you to receive a text or email the moment a payment is made (or missed).

- The Hero Move: If you see a payment is about to be missed, pay it yourself. It feels unfair to pay for a house you don’t live in, but it is much cheaper than trying to rebuild your credit after a foreclosure or “Notice of Default” hits your report.

4. Establish Solo Tradelines Immediately

If all your credit history was tied to your spouse, you might find yourself with a “Thin File” once the joint accounts are closed.

- The Strategy: Apply for a small Individual Credit Card or a Secured Card in your name only.

- Why it Matters: You need to show the bureaus that you are a stable, independent entity. Having your own history helps “dilute” the impact of any old joint accounts that might be dragging you down.

5. Add a Notice of Change to Your File

In Canada, you have the right to add a 100-word “Consumer Statement” to your Equifax and TransUnion reports.

- The Statement: “I am currently going through a legal separation. All joint accounts are being addressed via a Separation Agreement. Please contact me directly for any new credit applications.”

- The Benefit: While this doesn’t stop your score from dropping if a payment is missed, it alerts future lenders (like a car dealership or a landlord) that any recent “bruising” on your credit is due to a temporary life transition rather than chronic irresponsibility.

6. Update Your Address Everywhere

“I didn’t get the bill” is not a legal excuse for a late payment.

- The Risk: Utility bills (hydro, water, internet) are often in one name but tied to the “family home.” If your ex moves out and stops paying the gas bill that’s in your name, you won’t know until a collection agency calls you at your new place.

- The Move: Redirect your mail through Canada Post for at least 12 months and ensure every utility account is either closed or transferred to the person actually living in the property.

Separation Credit Checklist (2026)

Protecting Your Future

A separation is a transition, not a destination. By being proactive today, you ensure that when the dust settles, you have the credit score you need to buy a new home, start a business, or simply enjoy your financial independence.

Going through a transition and need to consolidate joint debt? [Talk to a Financial Hero] at LendingMoney.ca. We’ll help you untangle your finances and protect your score for the next chapter of your life.