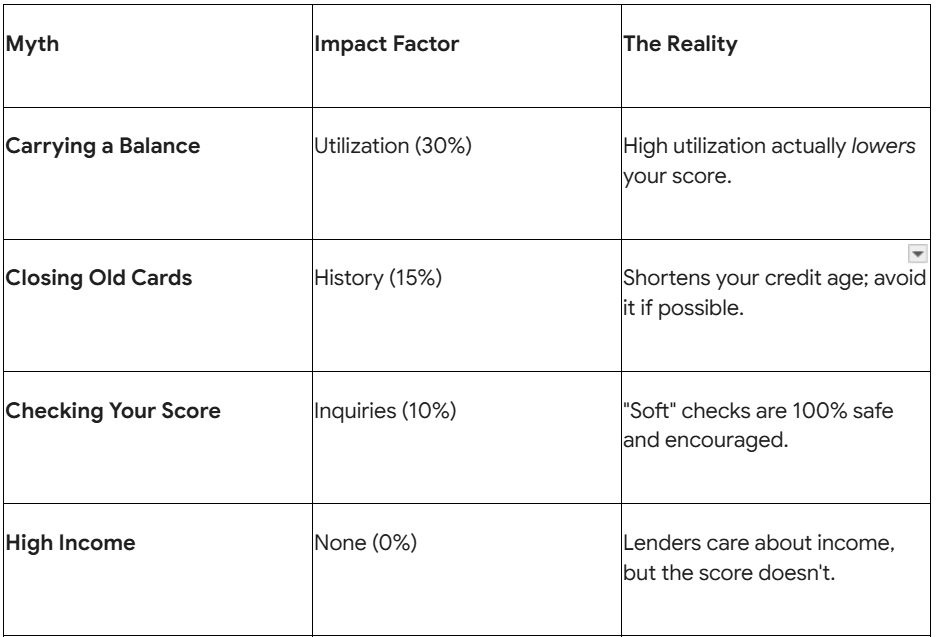

Myth 1: Carrying a Balance Boosts Your Score

The Myth: “You need to leave $20 or $30 on your credit card every month so the bank sees you’re using it and earns some interest.”

The 2026 Truth: Carrying a balance does nothing for your score except cost you money. In 2026, with credit card interest rates still averaging 19%–22%, “carrying a balance” is just a donation to the bank.

- The Hero Move: The credit bureaus only care that you used the card and paid the bill. Pay your statement in full every single month. Your score will be higher, and your bank account will be fuller.

Myth 2: Checking Your Own Score Lowers It

The Myth: “If I log into an app to see my score, it counts as an ‘inquiry’ and drops my points.”

The 2026 Truth: Checking your own score is a Soft Inquiry, and in 2026, it is considered a vital habit for financial health. Whether you use the Equifax app, TransUnion, or a third-party service like Borrowell, checking your own data has zero impact on your score.

- The Hero Move: Check your score once a month. With the rise of AI-driven identity theft in 2026, being the first to spot a suspicious inquiry is your best defense.

Myth 3: Closing Old Accounts “Cleans Up” Your Report

The Myth: “I don’t use that old $500 card from college anymore; I should close it to simplify my life.”

The 2026 Truth: Closing your oldest account is like deleting the first five chapters of a book. 15% of your score is based on Credit History Length. If you close your oldest card, your “average age of accounts” drops, and so does your score.

- The Hero Move: Keep the old card open. Put one small, recurring bill on it (like a $15 Spotify sub) and set it to auto-pay. This keeps the “history” alive without you having to carry the physical card.

Myth 4: Your Income Impacts Your Credit Score

The Myth: “I just got a big promotion and a $20,000 raise, so my credit score should go up next month.”

The 2026 Truth: The credit bureaus have no idea how much money you make. Your credit report tracks behavior, not wealth. A person making $40,000 a year can have a perfect 850 score, while a CEO making $500,000 can have a 500 score if they are disorganized with payments.

- The Hero Move: While income doesn’t help your score, it does help your Debt-to-Income (DTI) ratio. Use that raise to pay down your balances; that is what will trigger the score jump.

Myth 5: “No Debt” Means a Perfect Score

The Myth: “I pay for everything in cash and have no loans, so my credit must be amazing.”

The 2026 Truth: In the eyes of a 2026 lender, “No Credit” is almost as risky as “Bad Credit.” If you have no history of borrowing and repaying money, a lender has no data to predict if you’ll pay them back.

- The Hero Move: You need “Active Tradelines.” Even if you have the cash, use a credit card for daily purchases and pay it off immediately. You want to prove you can manage credit responsibly before you need a major loan, like a mortgage.

2026 Credit “Quick Stats”

Don’t Let Myths Stop Your Progress

The 2026 financial world moves fast, and “common knowledge” is often outdated. At LendingMoney.ca, we help you cut through the noise with facts. Whether you’re recovering from a consumer proposal or just trying to break the 800-point barrier, we provide the Credit Rehabilitation tools to get you there.

Ready to see the real story behind your credit score? [Connect with a Financial Hero] at LendingMoney.ca today and let’s build a strategy based on 2026 facts, not 1990 myths.