If you bought or refinanced your home in 2021, you likely enjoyed some of the lowest interest rates in Canadian history—some as low as 1.5% to 2%. As you approach your 2026 renewal, the landscape has changed. With the Bank of Canada holding its policy rate at 2.25% and fixed rates averaging between 4% and 5%, most homeowners are facing a monthly payment increase of 15% to 25%.

At LendingMoney.ca, we don’t want you to just “sign and send” your renewal papers. We want you to use this moment to optimize your entire financial life. Here is the 2026 guide to winning your renewal.

1. The Reality of the “2026 Payment Jump”

For a typical $500,000 mortgage, jumping from a 1.99% rate to a 4.79% rate means your monthly payment will climb by roughly $700 per month.

- The “Auto-Renewal” Trap: Your bank will send you a letter about 21 days before your term ends. It will likely offer you their “posted rate,” which is often 0.5% higher than what you could get by shopping around. Never sign the first offer.

- The “Stress Test” Myth: If you stay with your current lender, you do not have to re-qualify or pass the stress test. However, if you want to switch lenders to find a better rate, you may need to pass the 7.25% stress test.

2. Strategy: The 120-Day “Rate Hold”

In 2026, volatility is the only constant.

- The Move: Start shopping four months before your renewal date. Most lenders (and all Financial Heroes at LendingMoney.ca) can lock in a rate for you for 120 days.

- The Win: If rates go up before your renewal, you are protected at the lower locked-in rate. If rates go down, you can simply take the new, lower market rate. It’s a “no-lose” strategy.

3. Extending Amortization: The Cash-Flow Lifesaver

If the new 2026 payments are going to break your household budget, you have a powerful lever: Amortization.

- The Pivot: If you originally had a 25-year mortgage and you are 5 years in, your remaining amortization is 20 years. At renewal, you can often “stretch” that back out to 25 or even 30 years.

- The Result: While this increases the total interest you pay over the life of the loan, it can drop your monthly payment by $300 to $500, giving your family the breathing room you need to stay stable.

4. The “Consolidation Renewal” (Credit Rehab Move)

This is the most popular strategy at LendingMoney.ca in 2026. If you are renewing your mortgage but also carrying $30,000 in credit card debt at 22%, you are fighting a losing battle.

- The Move: Instead of a “Straight Renewal,” do a Refinance Renewal. Roll that high-interest debt into your new mortgage.

- The Result: Even if your mortgage rate goes up to 5%, you are still “killing” 22% debt. Your total monthly outflow for all debts will likely decrease, and your credit score will skyrocket as your utilization drops to zero.

5. New 2026 Rules for Investors (OSFI Changes)

If you are renewing a mortgage on a rental property, be prepared for new scrutiny.

- The “Independent Qualification” Rule: As of January 2026, OSFI requires that rental properties “stand on their own” for qualification if you switch lenders.

The Catch: If your rental isn’t generating enough cash flow to cover the new, higher interest rates, you may be “trapped” with your current lender. This makes it even more important to have a clean credit profile before your renewal date.

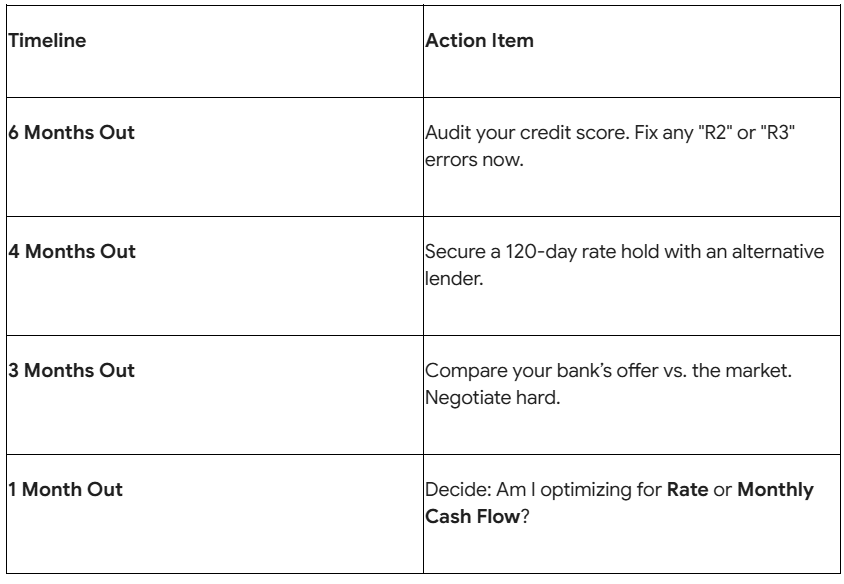

Your 2026 Renewal Checklist

Why Renew with LendingMoney.ca?

The big banks see renewal as an automated process. We see it as a financial reset. Whether you need to extend your amortization to save your budget or consolidate debt to save your credit, we are the alternative lending partnership to make it happen.

Is your renewal notice arriving soon? [Upload Your Renewal Offer] to LendingMoney.ca and let our Financial Heroes find you a better deal.