In the world of Canadian tax planning, a “good year” for your accountant is often a “bad year” for your mortgage broker. As we move through 2026, the gap between tax savings and borrowing power has widened, with lenders applying forensic-level scrutiny to self-employed applications.

If you are a business owner planning to buy or refinance a home, you need to understand that every dollar you “write off” to save $0.25 in taxes could cost you $5.00 in mortgage qualifying room. Here are the top five tax deductions that are most likely to hurt your mortgage odds in 2026.

1. Aggressive Vehicle Expenses (Section 9)

While the CRA allows you to deduct fuel, insurance, and repairs based on your business-use percentage, lenders in 2026 are wary of high vehicle write-offs.

- The Problem: If you brought in $100,000 but claimed $25,000 in “vehicle expenses,” a bank sees your income as $75,000.

- The 2026 Impact: Lenders now require 24 months of detailed logs to prove these expenses are “non-discretionary.”

- The “Hero” Strategy: Some alternative lenders will “add back” 15–20% of vehicle expenses to your income, but traditional “A-Lenders” will not. If you’re buying soon, consider scaling back the “detailed method” of vehicle deductions.

2. Large Capital Cost Allowance (CCA) Claims

CCA is “depreciation”—a non-cash expense that allows you to write off the cost of big items like computers (Class 50) or equipment over several years.

- The Problem: In 2026, the “Immediate Expensing” rules allow you to write off up to $1.5M in equipment instantly. This can drop your taxable income to near-zero.

- The Lender’s View: While this is a “paper loss” (you didn’t actually lose the money this year), most banks use your Line 15000 (Net Income) as the starting point for their math.

- The Strategy: At LendingMoney.ca, we work with lenders who understand that CCA is a “non-cash” add-back. We can often add this back to your income to boost your borrowing power, whereas a big bank might just see a “loss” on your T1 General.

3. High Travel & Entertainment Costs

In a post-pandemic world, the CRA has increased scrutiny on “Meal and Entertainment” (50% deductible). Mortgage lenders have followed suit.

- The Problem: High travel and dining costs suggest a “lifestyle-heavy” business. Lenders worry that if your business hits a slow patch, these costs are actually “essential” to keeping your clients, meaning they aren’t truly discretionary.

- The 2026 Rule: Lenders are now comparing your entertainment-to-revenue ratio. If you’re spending 15% of your gross income on “networking meals,” it raises a red flag regarding your actual take-home pay.

4. Heavy Home Office Deductions (T2125)

In 2026, the “flat rate” $2/day method is a distant memory. Business owners must use the “Detailed Method,” pro-rating rent, utilities, and mortgage interest.

- The Problem: While it’s great to write off 15% of your home costs, the lender sees this as a reduction in your net income.

- The Irony: You are using your home to save on taxes, but that very deduction might prevent you from buying a better home.

- The Strategy: If you are within 12 months of a mortgage application, speak to your accountant about “smoothing” these deductions. It might be worth paying a little more tax to show the $10,000 higher income the bank needs to see.

5. “Bad Debt” Write-Offs

If a client didn’t pay you and you write it off as “Bad Debt,” it tells a story to a lender.

- The Problem: Beyond the lower income, a high “Bad Debt” line tells a lender that your business may have “collection issues” or “low-quality clients.”

- The 2026 Impact: Lenders are looking for stability. They would rather see a slightly lower gross income than a high gross income with 10% in bad debt write-offs. It signals a lack of cash-flow predictability.

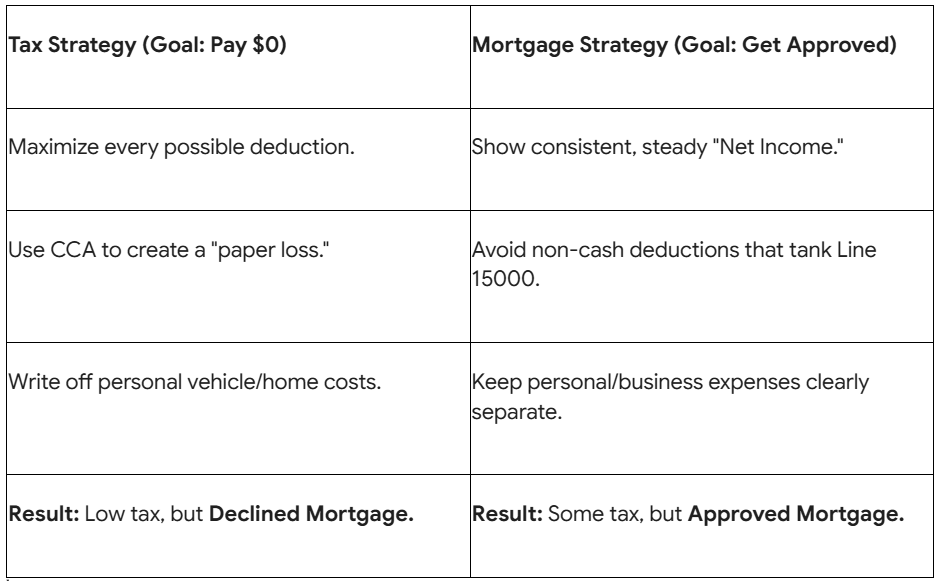

Comparison: Tax Strategy vs. Mortgage Strategy

The LendingMoney.ca “Add-Back” Solution

At LendingMoney.ca, we specialize in Credit Rehabilitation for the self-employed. We use an “Add-Back” approach that many big banks refuse to use. We can often take your net income and “gross it up” by adding back:

- Amortization/Depreciation (CCA)

- Home Office Expenses

- One-time legal or professional fees

Don’t let a “great” tax return ruin your mortgage dreams. [Connect with a Financial Hero] at LendingMoney.ca for a “Pre-Tax Review” of your application today.