When a “Big Six” bank says no, most Canadians assume their only remaining option is a high-interest private loan. However, there is a massive middle ground occupied by B Lenders and Alternative Lenders.

While both are “alternatives” to traditional banks, they serve very different purposes. At LendingMoney.ca, we want you to understand exactly where you fit on this spectrum so you can choose the right tool for your financial recovery.

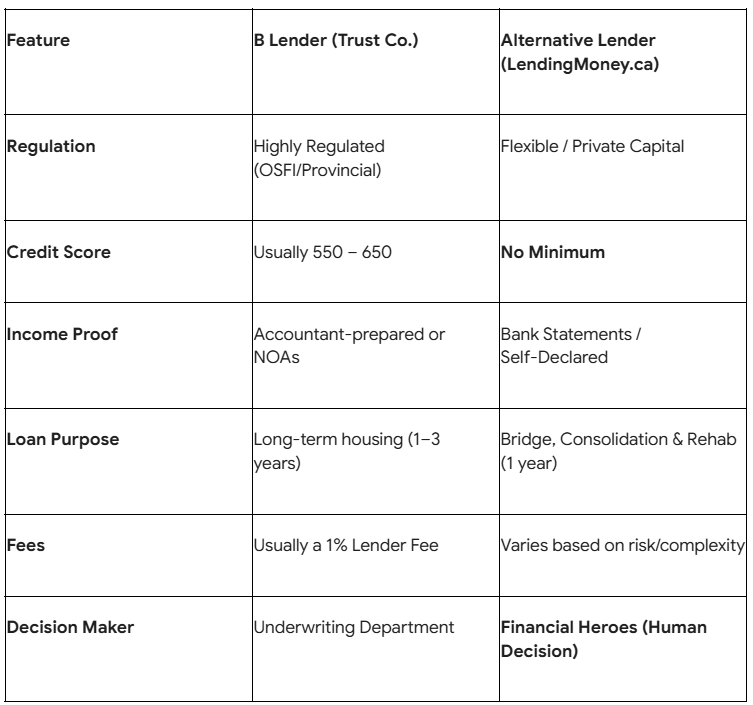

1. What is a B Lender ? (The Trust Company)

B Lenders are essentially “Bank-Lite.” They are federally or provincially regulated financial institutions, often including Trust Companies (like Home Trust or Community Trust) and specialized banks (like Equitable Bank).

- Who they are for: The Near-Prime borrower. You have a decent job and a decent house, but maybe your credit score is 600 instead of 700, or you are self-employed and can’t prove every dollar of income.

- The 2026 Rules: B Lenders are still heavily regulated. While they are more flexible than the Big Six, they still have strict boxes you must fit into regarding your debt-to-income ratios.

- The Rates: They offer a “middle-ground” rate—usually 1% to 2% higher than a standard bank rate.

The Catch: They almost always require a 20% down payment because they do not offer CMHC-insured mortgages.

2. What is an Alternative Lender ? (LendingMoney.ca)

An Alternative Lender is a non-institutional provider of capital. We aren’t bound by the same rigid “stress tests” or federal “Capital Adequacy” rules that govern banks and trust companies.

- Who we are for: The “Big Picture” borrower. You might be in a Consumer Proposal, recovering from a bankruptcy, or dealing with an “unconventional” property that an institution won’t touch.

- The Flexibility: We don’t just look at a credit score. We look at equity, cash flow, and your plan for the future. If you have a solid Exit Strategy (a plan to get back to a bank in 1–2 years), we can provide the funding that institutions won’t

- The Speed: Because we don’t have layers of institutional committees, we can move at lightning speed—often funding a deal in 24 to 48 hours.

Key Differences at a Glance (2026)

3. Why the B Lender Might Still Say No

In 2026, even B Lenders have become more cautious. Because they are “Deposit-Taking” institutions, they have to answer to regulators about the “quality” of their mortgage book.

If you have active collections, an un-discharged bankruptcy, or significant CRA debt, a B Lender Trust Company will likely still decline your application. They want “bruised” credit, not “broken” credit.

4. The LendingMoney.ca Bridge Strategy

This is where we come in. We don’t compete with B Lenders; we prepare you for them.

Most of our clients use our Alternative Lending solutions as a 12-month bridge.

- We provide the funds to pay off the collections, settle the CRA debt, or buy out the Consumer Proposal.

- While you are with us, we implement your Credit Rehabilitation plan.

- After 12 months, your “broken” credit has become “bruised” (or better), and we “graduate” you to a B Lender or even back to an A Lender bank.

Which One Do You Need?

- Choose a B Lender if your credit is “okay” and you just need a bit more flexibility on your income proof than the Big Six allows.

- Choose an Alternative Lender (LendingMoney.ca) if you need speed, have a complex situation, or need a financial “reset” to clear old debts before you can qualify anywhere else.

Still not sure which “box” you fit into? [Talk to a Financial Hero] at LendingMoney.ca. We’ll analyze your situation and tell you exactly which lender is the right stepping stone for your journey.