In Ontario, if you miss a mortgage payment, your lender doesn’t usually go to court to take your house (that’s foreclosure). Instead, they use a legal “shortcut” called Power of Sale.

This process allows the lender to sell your home to recover their money without needing a judge’s permission for the sale itself. Because it is faster and cheaper for the bank, it is the dominant way mortgages are enforced in Ontario. If you’ve received a “Notice of Sale,” the clock is already ticking. Here is the breakdown of the process.

1. The Timeline: How Fast Does It Move?

In 2026, lenders are moving quicker than ever to protect their capital. The transition from a “missed payment” to “losing the house” can happen in as little as 3 to 4 months.

- Day 15 of Default: Once you are 15 days behind, the lender has the legal right to issue a Notice of Sale.

- The 35-Day “Redemption Period”: This is your most critical window. By law, the lender must give you 35 days (40 if mailed) to “redeem” the mortgage.

Day 80+: If the redemption period ends and you haven’t paid, the lender can apply for a Writ of Possession. This is the document that allows the Sheriff to physically evict you and change the locks.

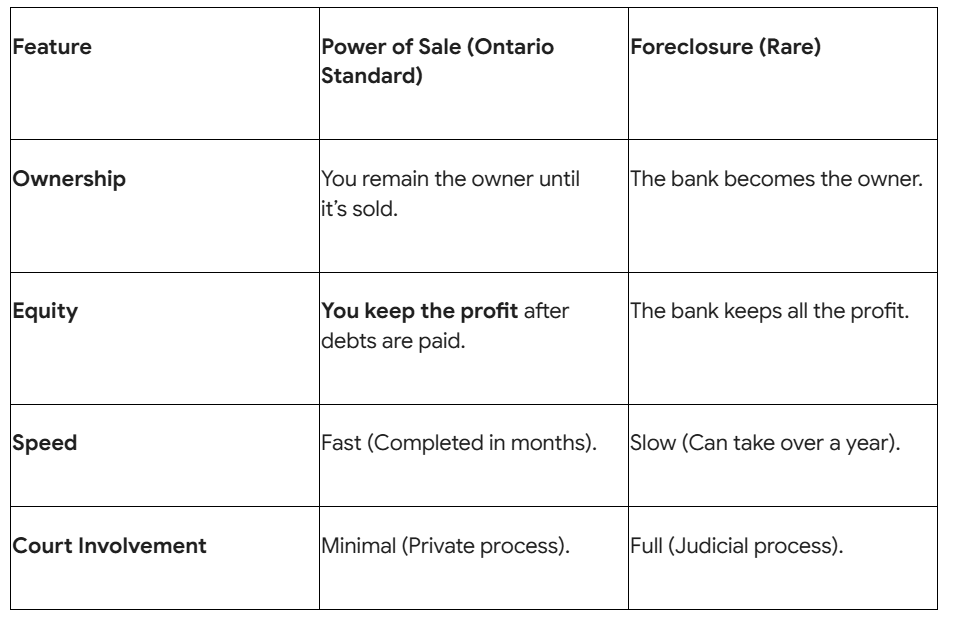

2. Power of Sale vs. Foreclosure: The Key Difference

Many people use these terms interchangeably, but they have a massive impact on your wallet.

The Good News: In a Power of Sale, if your house sells for $800,000 and you only owe $500,000, the remaining $300,000 (minus fees) belongs to you.

3. The “Legal Fee” Snowball

The most dangerous part of a Power of Sale isn’t the interest, it’s the fees. In 2026, once a file is sent to the lender’s lawyer, the costs explode:

- Lender’s Legal Fees: $2,500 – $7,000+

- Appraisal Fees: $500 – $1,000

- Property Inspection/Management: $1,000+

- Realtor Commissions: 5% of the sale price.

If you owe $10,000 in arrears, by the time the house is listed, you might actually need $30,000 to stop the sale. Acting early is the only way to save your equity.

4. Can You Stop a Power of Sale?

Yes. Until the moment the lender signs a “Statement of Purchase and Sale” with a new buyer, you have the right to stop the process.

- The “Cure”: You can pay the arrears and costs to bring the mortgage back into good standing.

- The “Payoff”: You can pay the entire mortgage balance in full.

- The 2026 Strategy: Most homeowners in this situation cannot get a loan from a big bank. At LendingMoney.ca, we provide Emergency Bridge Loans. We pay off the bank’s arrears and legal fees immediately, “voiding” the Power of Sale and giving you 12 months to breathe and refinance properly.

5. The Lender’s Duty of Care

In Ontario, the lender cannot simply “fire sale” your home to their cousin for $1. They have a legal duty to:

- Get an Appraisal: They must determine the fair market value.

- Market the Property: It must be listed on the MLS (Multiple Listing Service) to ensure the public can bid on it.

- Act in Good Faith: If they sell it for significantly less than it’s worth, you can sue them for the difference.

Don’t Wait for the Sheriff

A Power of Sale is a legal process, but it is also a financial negotiation. If you have equity in your home, you have options. You can sell the home yourself (which is always cheaper than letting the bank do it), or you can refinance with an alternative lender like LendingMoney.ca.

Have you received a “Notice of Sale Under Mortgage”? [Upload Your Notice] for a free, confidential review. We’ll help you calculate your equity and find the “Hero Move” to save your home.